Mô hình đột phá đảo chiều dựa trên chiến lược của nhà giao dịch rùa

Tổng quan

Chiến lược này dựa trên "Chiến lược giao dịch Rùa" (Turtle Trader Strategy) nổi tiếng, đã được kiểm chứng qua nhiều năm. Nó đưa ra tín hiệu mua và bán, cho phép tối đa 5 lệnh kim tự tháp, nghĩa là chiến lược có thể kích hoạt tới 5 lệnh cùng một hướng. Có quản lý rủi ro và vốn tốt.

Cần lưu ý, chiến lược này kết hợp hai hệ thống hoạt động đồng thời (S1 và S2).

Nguyên lý chiến lược

Quy mô vị thế rất quan trọng đối với nhà giao dịch Rùa để quản lý rủi ro hợp lý. Chiến lược điều chỉnh vị thế này thích ứng với biến động thị trường và tài khoản (lãi và lỗ). Nó dựa trên ATR (Average True Range - Khoảng dao động trung bình thực), còn gọi là "N". Độ dài mặc định là 20.

Số lượng đơn vị mua:

unit = (percentage_to_risk/100)*account/atr*syminfo.pointvalue

Tùy theo khẩu vị rủi ro, bạn có thể tăng tỷ lệ phần trăm tài khoản, nhưng nhà giao dịch Rùa mặc định là 1%. Nếu bạn giao dịch hợp đồng, đơn vị phải được làm tròn xuống theo mặc định.

Có thêm một quy tắc để giảm rủi ro khi giá trị tài khoản thấp hơn vốn ban đầu: trong trường hợp đó, trong công thức đơn vị phải thay thế bằng:

account := (strategy.equity-strategy.openprofit)*(strategy.equity-strategy.openprofit)/strategy.initial_capital

Có hai hệ thống hoạt động đồng thời:

Đột phá là một đỉnh cao mới hoặc đáy thấp mới. Nếu là đỉnh cao mới, chúng ta mở vị thế mua; ngược lại, nếu là đáy thấp mới, chúng ta vào lệnh bán.

Chúng ta thêm một quy tắc bổ sung:

Quy tắc bổ sung này cho phép nhà giao dịch tham gia xu hướng chính nếu bỏ lỡ tín hiệu của hệ thống 1. Nếu bỏ lỡ tín hiệu của hệ thống 1 mà nến tiếp theo cũng là một đột phá 20 ngày mới, thì S1 sẽ không phát tín hiệu. Chúng ta phải chờ tín hiệu S2 hoặc chờ nến không tạo đột phá mới để kích hoạt lại S1.

Phân tích ưu điểm

Chiến lược Rùa cho phép chúng ta thêm các đơn vị bổ sung vào vị thế khi giá biến động có lợi cho chúng ta. Tôi đã cấu hình chiến lược cho phép thêm tối đa 5 lệnh cùng một hướng. Do đó, nếu giá thay đổi từ mức mua, chúng ta sẽ thêm đơn vị.

Chúng ta đặt lệnh đầu tiên (mua hoặc bán) là lệnh tối đa. Các lệnh kim tự tháp tiếp theo sẽ có số đơn vị ít hơn lệnh đầu tiên.

Chúng ta đặt mức dừng lỗ tối đa 10% cho lệnh đầu tiên, nghĩa là bạn sẽ không mất quá 10% giá trị lệnh đầu tiên. Tuy nhiên, vì mức dừng lỗ sẽ tăng/giảm 0.5 * ATR(20), các lệnh kim tự tháp của bạn có thể mất nhiều hơn, lúc này không đảm bảo mức lỗ không vượt quá 10%. Rủi ro vẫn được quản lý tốt vì giá trị các lệnh này thấp hơn giá trị lệnh đầu tiên.

Phân tích rủi ro

Rủi ro lớn nhất của chiến lược này là vị thế quá lớn. Vì lệnh được đặt theo lệnh thị trường, nếu đồng thời đặt nhiều lệnh thị trường lớn, sẽ gây tác động lớn đến báo giá, dẫn đến trượt giá lớn. Điều này có thể gây tổn thất vốn nghiêm trọng.

Một rủi ro khác là cấu hình quản lý vốn không phù hợp. Nếu cấu hình dừng lỗ sai hoặc tỷ lệ quá lớn, đều có thể dẫn đến thua lỗ lớn. Cần cấu hình cẩn thận theo khẩu vị rủi ro của bản thân.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa ở các khía cạnh sau:

-

Có thể kiểm tra tác động của các tham số khác nhau đến tỷ suất sinh lời và tỷ lệ Sharpe, chẳng hạn như chu kỳ ATR, bội số ATR của dừng lỗ, v.v. Tìm ra tổ hợp tham số tối ưu.

-

Có thể kiểm tra các quy tắc vào lệnh và thoát lệnh khác nhau. Ví dụ: sử dụng mô hình nến làm bộ lọc bổ sung.

-

Có thể thử các loại dừng lỗ khác, chẳng hạn như dừng lỗ trượt, dừng lỗ động. Điều này có thể làm giảm xác suất bị chạm dừng lỗ.

-

Có thể kiểm tra số lượng lệnh kim tự tháp khác nhau. Càng nhiều lệnh, đòn bẩy và rủi ro càng cao. Tìm điểm cân bằng tốt nhất.

-

Có thể thử dừng giao dịch trong các khoảng thời gian cụ thể (ví dụ: trước khi công bố dữ liệu việc làm phi nông nghiệp Hoa Kỳ) để tránh tác động của các sự kiện lớn.

Tổng kết

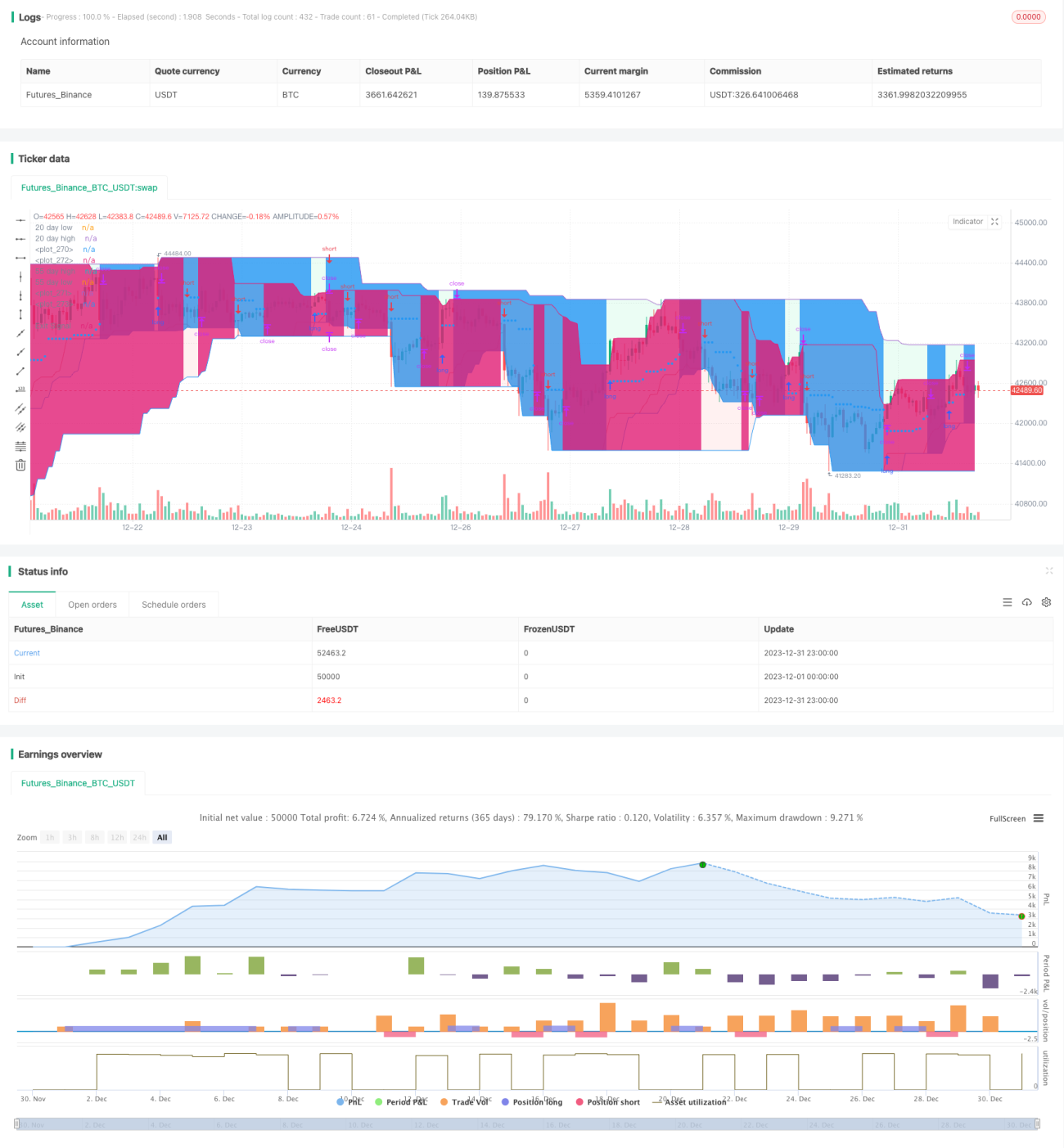

Nhìn chung, chiến lược này có sự cân bằng tốt giữa rủi ro và lợi nhuận, phù hợp với giao dịch xu hướng trung và dài hạn. Nó có ưu điểm như giao dịch hệ thống hóa, rủi ro có thể kiểm soát. Thông qua tối ưu hóa, có thể cải thiện hơn nữa tính ổn định và tỷ suất sinh lời của chiến lược.

- 1