Chiến lược đột phá động lượng hai đường MA

Tổng quan

Chiến lược đột phá động lượng hai đường MA là một chiến lược giao dịch định lượng kết hợp hai đường trung bình động (MA) và chỉ báo RSI. Chiến lược này tính toán đường trung bình động nhanh, đường trung bình động chậm và chỉ báo RSI, thiết lập ngưỡng quá mua/quá bán cho chỉ báo động lượng RSI. Khi hai đường MA tạo thành giao cắt vàng (golden cross) thì vào lệnh mua, khi giao cắt tử thần (death cross) thì vào lệnh bán, nhằm nắm bắt các xu hướng thị trường.

Nguyên lý chiến lược

Chiến lược đột phá động lượng hai đường MA chủ yếu dựa trên hai đường trung bình động và chỉ báo RSI. Đầu tiên, tính hai đường trung bình động: một nhanh và một chậm. Đường nhanh là đường trung bình động có trọng số 10 ngày, đường chậm là đường trung bình động thích ứng tuyến tính 100 ngày. Sau đó, tính chỉ báo RSI 14 ngày và thiết lập ngưỡng quá mua/quá bán. Khi đường nhanh cắt lên trên đường chậm, xác định là xu hướng tăng; ngược lại, khi đường nhanh cắt xuống dưới đường chậm, xác định là xu hướng giảm. Khi xác định xu hướng tăng/giảm, cần có chỉ báo RSI vượt trên ngưỡng quá mua hoặc dưới ngưỡng quá bán, điều này giúp lọc hiệu quả các tín hiệu phá vỡ giả.

Cụ thể, khi xác định là xu hướng tăng, nếu chỉ báo RSI hiện tại cao hơn ngưỡng quá mua, thì mở vị thế mua; khi xác định là xu hướng giảm, nếu chỉ báo RSI thấp hơn ngưỡng quá bán, thì mở vị thế bán. Sau khi mở vị thế, nếu tín hiệu giao dịch đảo chiều, sẽ mở vị thế ngược lại.

Lợi thế của chiến lược

Chiến lược đột phá động lượng hai đường MA kết hợp hai đường MA và chỉ báo RSI, có thể nhận diện hiệu quả xu hướng thị trường và sử dụng chỉ báo RSI để lọc các tín hiệu phá vỡ giả, từ đó nâng cao độ tin cậy của tín hiệu giao dịch. So với hệ thống một đường MA đơn thuần, chiến lược này có thể giảm đáng kể các giao dịch không hiệu quả. Ngoài ra, việc tối ưu hóa tham số của chỉ báo RSI cũng mang lại sự linh hoạt cho chiến lược.

Rủi ro của chiến lược

Chiến lược đột phá động lượng hai đường MA cũng tồn tại một số rủi ro nhất định. Hệ thống hai đường MA rất nhạy cảm với tham số, cần kiểm tra cẩn thận các tổ hợp tham số đối với từng thị trường khác nhau. Ngoài ra, nếu ngưỡng của chỉ báo RSI được thiết lập không phù hợp, cũng có thể dẫn đến bỏ lỡ cơ hội giao dịch. Cuối cùng, cơ chế trailing stop dạng mạnh trong một số điều kiện thị trường nhất định có thể bị phá vỡ, do đó cần điều chỉnh điểm dừng dựa trên kết quả backtest.

Tối ưu hóa chiến lược

Chiến lược đột phá động lượng hai đường MA có thể được tối ưu hóa từ các khía cạnh sau:

- Tối ưu hóa tham số của đường MA nhanh và chậm, tìm tổ hợp tham số tốt nhất;

- Tối ưu hóa tham số RSI, điều chỉnh ngưỡng quá mua/quá bán;

- Thêm cơ chế trailing stop thích ứng để kiểm soát rủi ro;

- Thêm mô-đun tối ưu hóa khối lượng vào lệnh, nâng cao hiệu quả sử dụng vốn.

Kết luận

Chiến lược đột phá động lượng hai đường MA sử dụng hệ thống hai đường MA để xác định hướng xu hướng và tận dụng chỉ báo RSI để lọc tín hiệu, có thể cải thiện hiệu quả nhược điểm của hệ thống một đường MA đơn thuần. Chiến lược này có không gian tối ưu hóa tham số lớn và có thể thực hiện điều chỉnh thích ứng, là một chiến lược theo xu hướng xuất sắc.

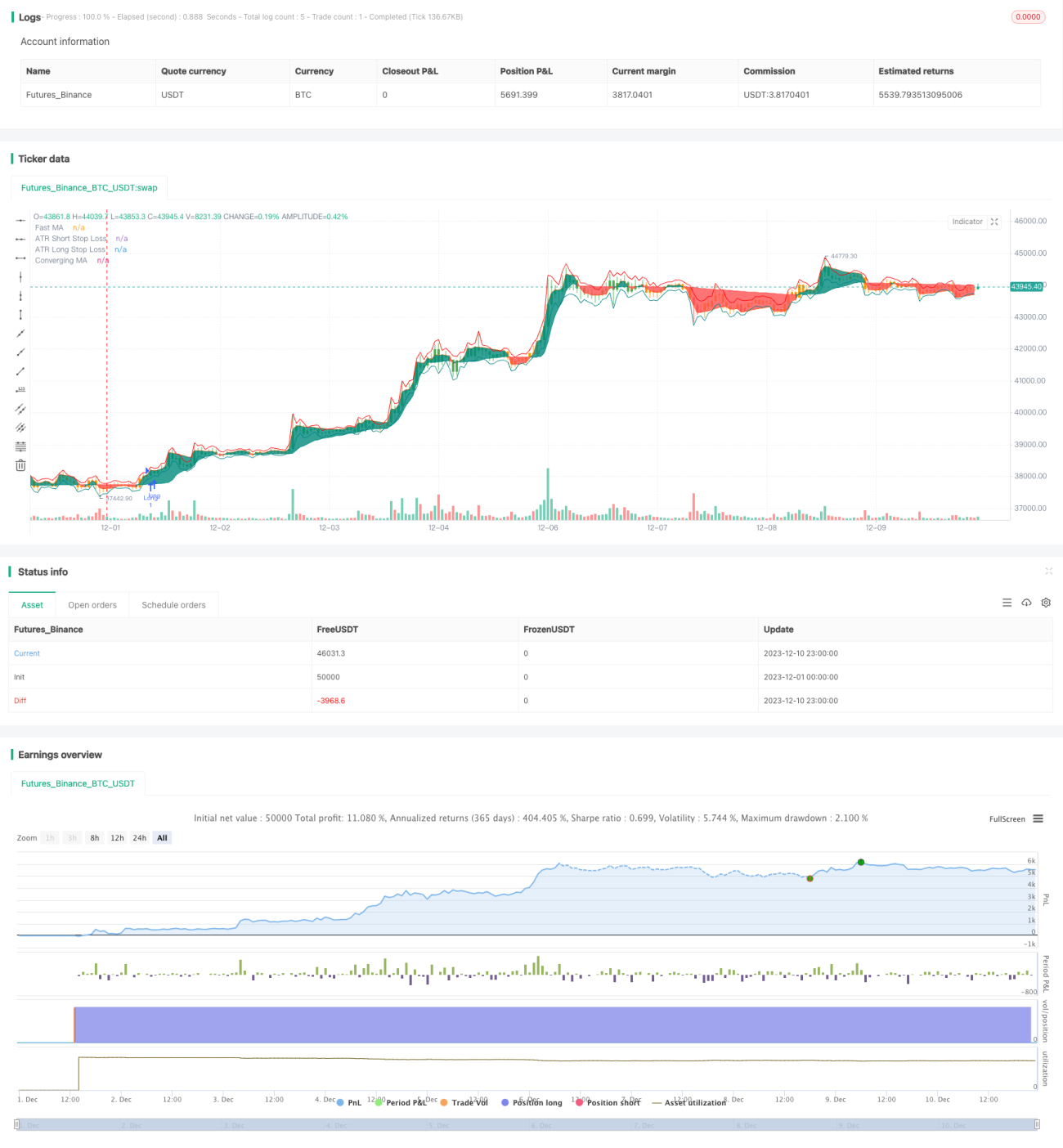

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1