Chiến lược cắt lỗ theo xu hướng RSI

Tổng quan

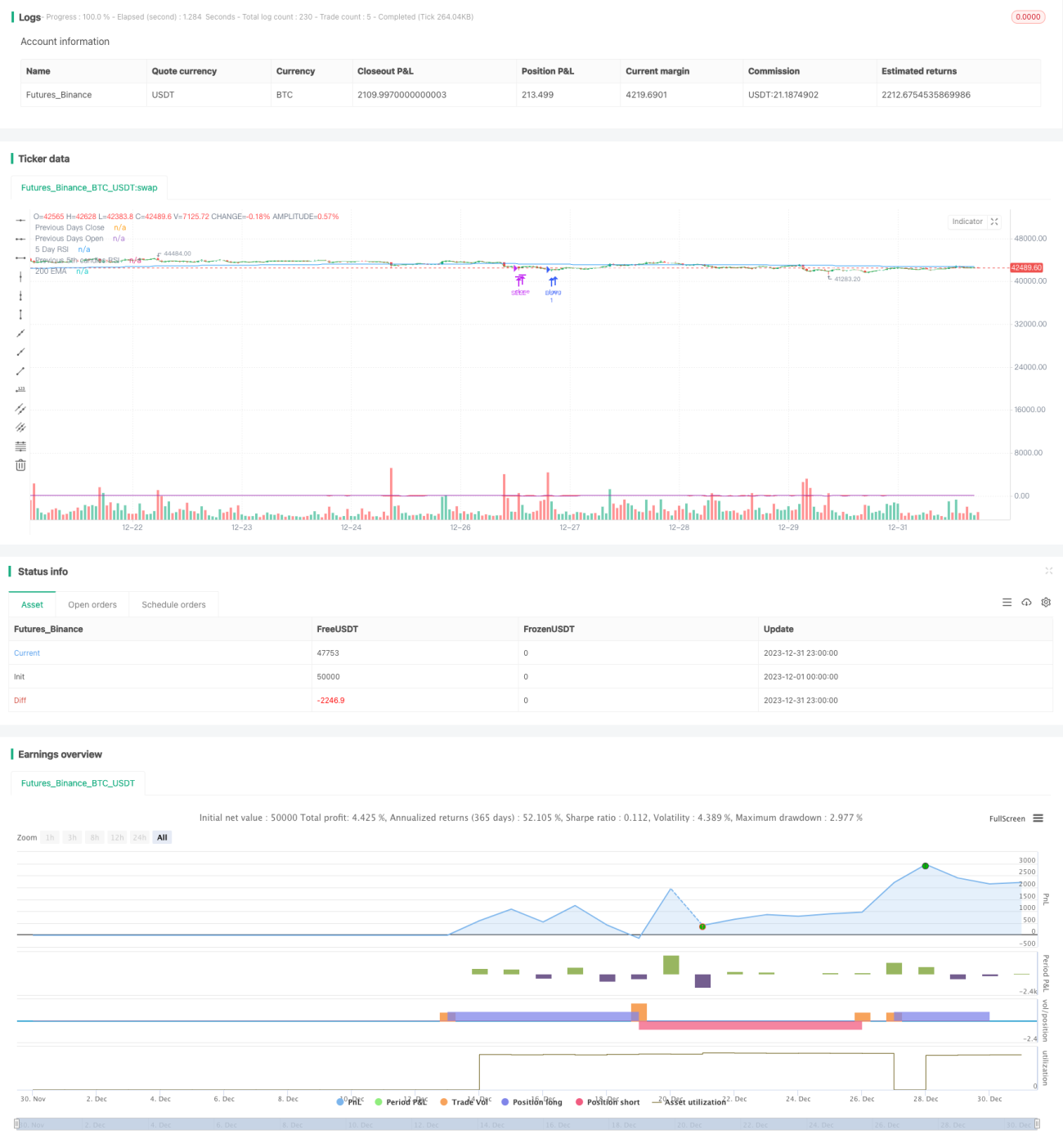

Đây là một chiến lược giao dịch định lượng sử dụng chỉ báo RSI để xác định xu hướng và thiết lập cắt lỗ/chốt lời. Chiến lược này kết hợp chỉ báo RSI để đánh giá hướng của xu hướng thị trường, đồng thời thiết lập cắt lỗ/chốt lời động nhằm khóa lợi nhuận và giảm thiểu rủi ro tối đa.

Nguyên lý chiến lược

Chiến lược chủ yếu sử dụng chỉ báo RSI để xác định hướng xu hướng thị trường, từ đó quyết định mua lên hay bán xuống. Khi chỉ báo RSI cắt lên trên đường thấp, thị trường được đánh giá là đang trong xu hướng tăng, thực hiện lệnh mua lên; khi chỉ báo RSI cắt xuống dưới đường cao, thị trường được đánh giá là đang trong xu hướng giảm, thực hiện lệnh bán xuống.

Đồng thời, chiến lược theo dõi giá mở lệnh của từng lệnh để thiết lập cắt lỗ/chốt lời động. Đối với lệnh mua lên, đặt một tỷ lệ phần trăm nhất định so với giá mở lệnh làm đường cắt lỗ; đối với lệnh bán xuống, đặt một tỷ lệ phần trăm nhất định so với giá mở lệnh làm đường chốt lời. Khi giá chạm các đường cắt lỗ/chốt lời, chiến lược sẽ tự động đóng lệnh để cắt lỗ hoặc chốt lời.

Lợi thế của chiến lược

- Sử dụng chỉ báo RSI để xác định hướng xu hướng thị trường, tránh giao dịch trong vùng đi ngang;

- Thiết lập cắt lỗ/chốt lời động, có thể linh hoạt khóa lợi nhuận, kiểm soát rủi ro hiệu quả;

- Các tham số RSI và tỷ lệ cắt lỗ/chốt lời đều có thể điều chỉnh và tối ưu thông qua đầu vào bên ngoài.

Rủi ro của chiến lược

- Chỉ báo RSI có độ trễ nhất định, có thể bỏ lỡ các điểm chuyển đổi xu hướng ngắn hạn;

- Đường cắt lỗ/chốt lời quá gần có thể bị phá vỡ và dẫn đến thanh lý vị thế.

Hướng tối ưu hóa

- Có thể kiểm tra hiệu quả của chỉ báo RSI với các chu kỳ khác nhau;

- Có thể kiểm tra các tổ hợp tham số khác nhau để tìm tỷ lệ cắt lỗ/chốt lời tối ưu;

- Có thể thêm các chỉ báo phụ trợ để lọc tín hiệu.

Kết luận

Nhìn chung, chiến lược này là một chiến lược giao dịch định lượng sử dụng chỉ báo RSI để theo dõi xu hướng, kết hợp với cắt lỗ/chốt lời động. So với các chiến lược giao dịch chỉ dựa trên một chỉ báo duy nhất, chiến lược này kiểm soát rủi ro tốt hơn và có thể khóa lợi nhuận hiệu quả. Thông qua tối ưu hóa tham số và bổ sung các chỉ báo phụ trợ, hiệu suất của chiến lược có thể được cải thiện hơn nữa.

- 1