Chiến lược giao dịch định lượng Bitcoin dựa trên xu hướng siêu

Tổng quan

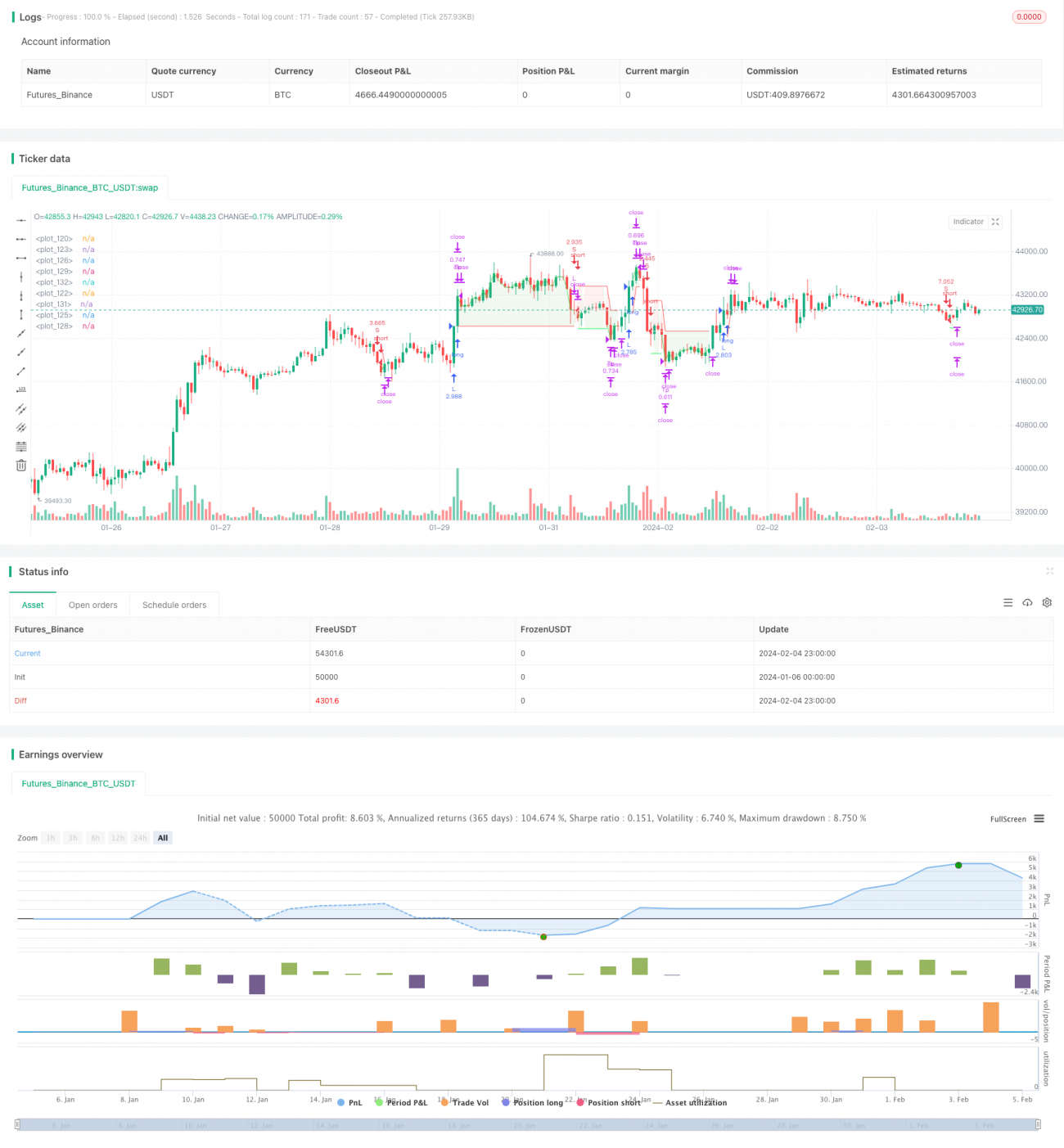

Chiến lược này là một chiến lược giao dịch định lượng tự động cho Bitcoin dựa trên chỉ báo Super Trend. Nó sử dụng chỉ báo Super Trend để đánh giá xu hướng thị trường, kết hợp nguyên tắc cắt lỗ ATR để kiểm soát rủi ro, thực hiện giao dịch hai chiều (long và short). Ưu điểm lớn nhất của chiến lược là tỷ lệ rủi ro/lợi nhuận tốt, chiến lược cắt lỗ đáng tin cậy, phù hợp với đầu tư trung và dài hạn. Chiến lược này có thể áp dụng trên khung 4 giờ tại các sàn giao dịch chính như Coinbase Pro.

Nguyên lý chiến lược

Chiến lược này sử dụng chỉ báo Super Trend để xác định hướng xu hướng thị trường. Khi chỉ báo Super Trend chuyển từ xu hướng giảm sang xu hướng tăng, vào lệnh mua (long); khi chỉ báo Super Trend chuyển từ xu hướng tăng sang xu hướng giảm, vào lệnh bán (short).

Cụ thể, chiến lược trước tiên tính toán chỉ báo ATR với độ dài 14 chu kỳ, nhân với bội số cắt lỗ ATR (ví dụ 1.5 lần) để xác định khoảng cách cắt lỗ cho mỗi lệnh. Sau đó tính chỉ báo Super Trend với các tham số mặc định (chu kỳ ATR 9, hệ số Super Trend 2.5). Khi chỉ báo Super Trend đổi hướng, tín hiệu giao dịch được phát ra.

Sau khi vào lệnh, điểm cắt lỗ được cố định ở trên hoặc dưới mức cắt lỗ ATR. Điểm chốt lời đầu tiên được tính dựa trên tỷ lệ rủi ro/phần thưởng, mặc định là 0,75, tức là khoảng cách chốt lời bằng 0,75 lần khoảng cách cắt lỗ. Khi giá đạt đến điểm chốt lời đầu tiên, đóng 50% vị thế và di chuyển điểm cắt lỗ về mức giá mở cửa (sau khi có lợi nhuận để tăng thêm vị thế), nhằm khóa lợi nhuận cho vị thế đó. Khoảng cách chốt lời thứ hai tiếp tục được tính theo tỷ lệ rủi ro/phần thưởng 0,75. Nếu giá chạm cắt lỗ, toàn bộ vị thế còn lại sẽ bị cắt lỗ và thoát lệnh.

Do đó, chiến lược này có thể đảm bảo rủi ro cắt lỗ được kiểm soát, đồng thời thông qua việc chốt lời một phần để đảm bảo lợi nhuận, phù hợp với chiến lược đầu tư trung và dài hạn.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược là tỷ lệ rủi ro/lợi nhuận tốt, có thể nắm giữ trung và dài hạn. Cụ thể:

-

Sử dụng Super Trend để đánh giá xu hướng thị trường, lọc nhiễu thị trường, tránh bỏ lỡ xu hướng chính.

-

Cắt lỗ động theo ATR, kiểm soát đáng tin cậy tổn thất mỗi lệnh.

-

Phương pháp chốt lời một phần để khóa lợi nhuận, tỷ lệ rủi ro/lợi nhuận cao.

-

Khi giá đạt đến điểm chốt lời 1, điều chỉnh cắt lỗ về giá mở cửa, đảm bảo lợi nhuận, tăng cường độ ổn định của chiến lược.

-

Logic giao dịch cực kỳ đơn giản, dễ hiểu và triển khai, có nhiều không gian tối ưu tham số.

-

Có thể áp dụng trên dữ liệu trong ngày hoặc tần suất cao của các sàn giao dịch chính, tính linh hoạt cao.

Phân tích rủi ro

Chiến lược này cũng có một số rủi ro, tập trung ở các khía cạnh sau:

-

Các sự kiện bất ngờ trên thị trường gây ra gap hoặc nhảy giá, không thể cắt lỗ, có thể chịu tổn thất lớn. Có thể giảm rủi ro bằng cách điều chỉnh hợp lý bội số cắt lỗ ATR.

-

Chỉ báo Super Trend phán đoán sai, gây ra tín hiệu giao dịch sai. Có thể tối ưu bằng cách điều chỉnh tổ hợp tham số ATR và Super Trend.

-

Tỷ lệ đóng một phần vị thế quá cao, không thu được đủ lợi nhuận từ xu hướng. Cần điều chỉnh tỷ lệ đóng một phần phù hợp với từng thị trường.

-

Tần suất giao dịch có thể quá cao hoặc quá thấp. Nên điều chỉnh tham số Super Trend để tìm cân bằng tối ưu.

Hướng tối ưu

Chiến lược này còn nhiều không gian tối ưu, tập trung ở các khía cạnh sau:

-

Thử nghiệm các phương pháp cắt lỗ ATR khác nhau, như ATR tiêu chuẩn, cắt lỗ động lượng, cắt lỗ Bollinger Band, v.v. để tối ưu chiến lược cắt lỗ.

-

Kiểm tra chỉ báo Super Trend với các tham số khác nhau, tìm tổ hợp tham số tối ưu. Có thể sử dụng tối ưu hóa bước hoặc thuật toán di truyền để tối ưu đa chiều.

-

Thử nghiệm chồng thêm chỉ báo cắt lỗ thứ hai lên trên mức cắt lỗ, như kênh Donchian, để cắt lỗ đáng tin cậy hơn.

-

Kiểm tra các tỷ lệ đóng một phần khác nhau, tìm điểm cân bằng tối ưu giữa hiện thực lợi nhuận và rủi ro. Tỷ lệ đóng một phần cũng có thể điều chỉnh động.

-

Khám phá các chiến lược cắt lỗ động, điều chỉnh vị thế động dựa trên học máy, v.v.

Tổng kết

Chiến lược này là một chiến lược định lượng dựa trên Super Trend để xác định xu hướng, cắt lỗ động ATR và chốt lời một phần để thu lợi nhuận. Nó có sự cân bằng tốt giữa rủi ro và lợi nhuận, phù hợp với giao dịch tự động. Chiến lược này có thể tối ưu đáng kể về siêu tham số, phương pháp cắt lỗ, phương pháp chốt lời, v.v., là một chiến lược định lượng đáng được tối ưu và áp dụng lâu dài.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Developed by © StrategiesForEveryone

//@version=5

- 1