Chiến lược trailing stop loss dựa trên Heikin Ashi Super Trend

Tổng quan chiến lược

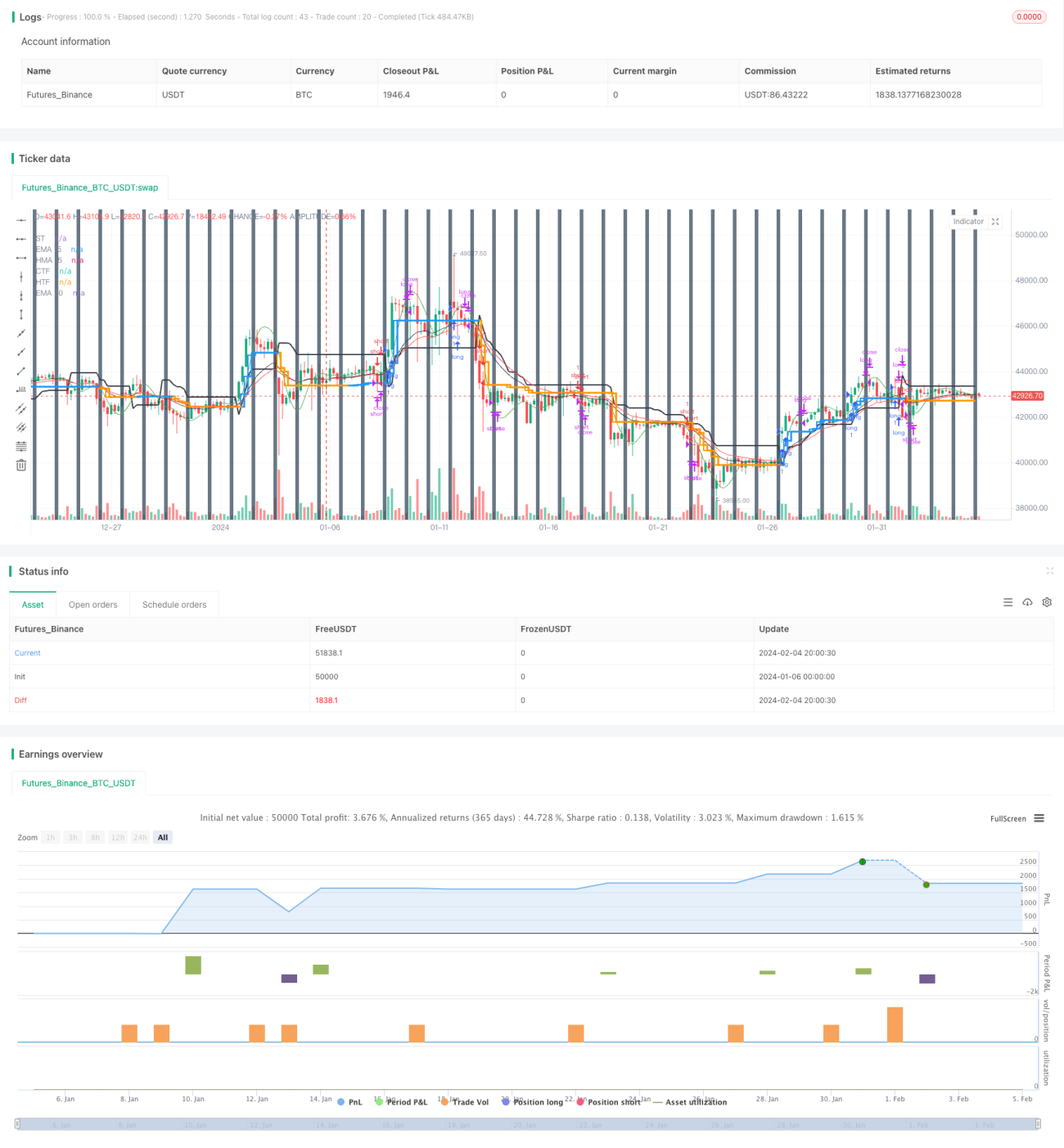

Chiến lược này là một chiến lược trailing stop kết hợp giữa nến Heikin Ashi và chỉ báo SuperTrend. Nó sử dụng nến Heikin Ashi để lọc nhiễu thị trường, chỉ báo SuperTrend để xác định hướng xu hướng, và dùng SuperTrend làm đường stop động, giúp theo dõi xu hướng và kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

- Tính nến Heikin Ashi: bao gồm giá mở cửa, giá đóng cửa, giá cao nhất, giá thấp nhất.

- Tính chỉ báo SuperTrend: dựa trên ATR và giá để tính dải trên và dải dưới.

- Kết hợp nến Heikin Ashi và SuperTrend để xác định hướng xu hướng.

- Khi giá đóng cửa Heikin Ashi gần dải trên của SuperTrend hơn so với giá đóng cửa của nến trước đó, đó là xu hướng tăng; khi giá đóng cửa Heikin Ashi gần dải dưới của SuperTrend hơn so với giá đóng cửa của nến trước đó, đó là xu hướng giảm.

- Trong xu hướng tăng, sử dụng dải trên của SuperTrend làm đường trailing stop; trong xu hướng giảm, sử dụng dải dưới của SuperTrend làm đường trailing stop.

Lợi thế của chiến lược

- Sử dụng Heikin Ashi để lọc các phá vỡ giả, giúp nhận diện tín hiệu xu hướng đáng tin cậy hơn.

- SuperTrend làm stop động, tối đa hóa lợi nhuận từ xu hướng, tránh drawdown quá lớn.

- Kết hợp nhiều khung thời gian để xác định xu hướng tăng/giảm, giúp xác nhận tín hiệu đỉnh/đáy chính xác hơn.

- Chức năng đóng lệnh theo thời gian giúp tránh ảnh hưởng của các diễn biến thị trường bất hợp lý vào những thời điểm cụ thể.

Rủi ro của chiến lược

- Dễ bị stop loss khi xu hướng đảo chiều. Có thể nới lỏng mức stop một chút để giảm rủi ro này.

- Cài đặt tham số SuperTrend không phù hợp có thể khiến stop quá rộng hoặc quá hẹp. Có thể thử nghiệm các bộ tham số khác nhau.

- Chưa xem xét vấn đề quản lý vốn. Cần thiết lập kiểm soát vị thế.

- Chưa tính chi phí giao dịch. Cần đánh giá tác động của chi phí.

Hướng tối ưu hóa chiến lược

- Tối ưu hóa bộ tham số SuperTrend để tìm tham số tối ưu.

- Thêm chức năng kiểm soát vị thế.

- Đưa yếu tố chi phí vào, như phí giao dịch, trượt giá, v.v.

- Có thể linh hoạt điều chỉnh mức stop dựa trên cường độ xu hướng.

- Xem xét kết hợp các chỉ báo khác để lọc tín hiệu vào lệnh.

Tổng kết

Chiến lược này tích hợp ưu điểm của hai chỉ báo Heikin Ashi và SuperTrend, có thể bắt được hướng xu hướng, đồng thời sử dụng SuperTrend để tự động hóa trailing stop động, từ đó khóa lợi nhuận từ xu hướng. Rủi ro chính của chiến lược đến từ sự đảo chiều xu hướng và tối ưu hóa tham số, cả hai khía cạnh này đều có thể được cải thiện thông qua tối ưu hóa thêm. Nhìn chung, chiến lược này sử dụng sự kết hợp chỉ báo để nâng cao tính ổn định và không gian lợi nhuận của hệ thống giao dịch.

- 1