多时标自适应震荡轮廓跟踪策略

Tổng quan

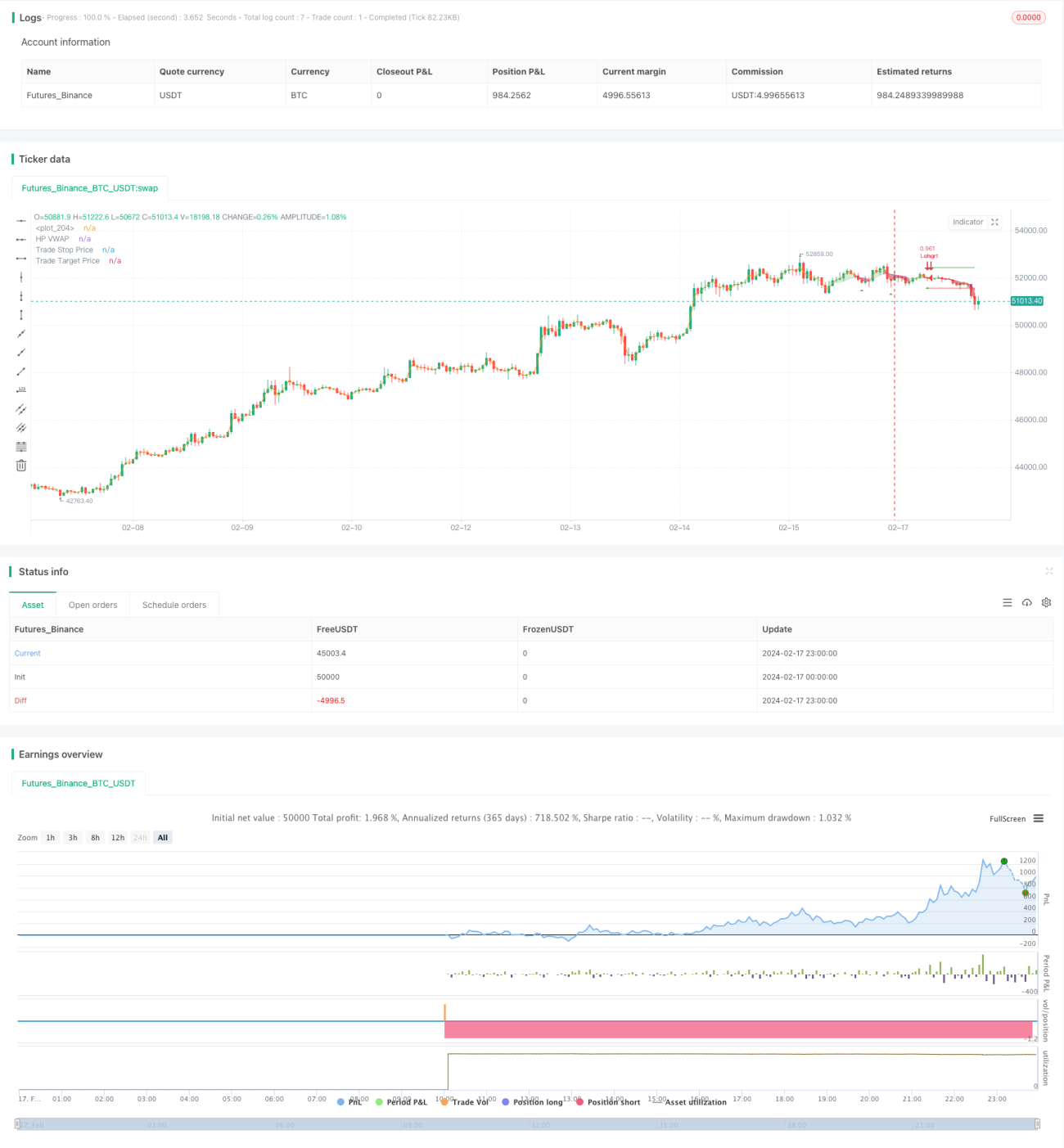

Chiến lược này sử dụng bộ lọc Hodrick-Prescott (HP) để làm mịn giá, trích xuất đường xu hướng giá. Sau đó, dựa trên khung thời gian do người dùng xác định, tính toán giá trung bình gia quyền tùy chỉnh (VWAP). Khi giá cao hơn đường xu hướng thì mua lên, thấp hơn thì bán xuống. Đồng thời kết hợp cắt lỗ ATR để đảm bảo rủi ro giao dịch có thể kiểm soát được.

Nguyên lý chiến lược

-

Sử dụng bộ lọc HP để trích xuất đường xu hướng giá. Bộ lọc HP trích xuất thành phần xu hướng dài hạn của giá thông qua phương pháp tối ưu hóa, loại bỏ nhiễu biến động ngắn hạn.

-

Tính VWAP dựa trên khung thời gian do người dùng tự xác định. VWAP phản ánh chính xác hơn giá trung bình trong các chu kỳ khác nhau.

-

Khi giá cao hơn đường xu hướng HP, điều kiện mua lên được thỏa mãn; khi giá thấp hơn đường xu hướng HP, điều kiện bán xuống được thỏa mãn. Nhờ đó có thể bắt được các đột phá từ dưới lên hoặc từ trên xuống.

-

Cắt lỗ ATR kết hợp với mức rủi ro hợp lý, tránh thua lỗ quá lớn.

Phân tích ưu điểm

-

Sử dụng bộ lọc HP để trích xuất xu hướng giá, so với các chỉ báo như MA thì mượt hơn, tránh bị đánh lừa bởi biến động giá ngắn hạn.

-

VWAP chu kỳ tùy chỉnh, linh hoạt hơn, thích ứng với sự thay đổi chu kỳ thị trường.

-

Giao dịch theo hướng xu hướng, phù hợp với triết lý giao dịch xu hướng, tỷ lệ thắng cao.

-

Cắt lỗ ATR kiểm soát thua lỗ từng lệnh, tránh thua lỗ quá lớn.

-

Nhiều tham số có thể điều chỉnh, có thể tối ưu hóa cho các thị trường khác nhau.

Rủi ro và biện pháp đối phó

-

Trong giai đoạn dao động đi ngang, có thể thường xuyên bị chạm stop loss. Có thể nới rộng phạm vi cắt lỗ phù hợp.

-

Vào giai đoạn cuối xu hướng, thường xuất hiện các đột phá thăm dò kiểu hồi lại khiến chiến lược bị mắc kẹt. Nên kết hợp các chỉ báo khác để nhận biết giai đoạn cuối xu hướng, đóng lệnh kịp thời.

-

Cài đặt chu kỳ VWAP không phù hợp có thể bỏ lỡ các cơ hội giao dịch hiệu quả hơn. Nên kết hợp với chỉ báo xu hướng để điều chỉnh chu kỳ VWAP một cách linh hoạt.

Hướng tối ưu hóa

-

Tham số λ của bộ lọc HP có thể điều chỉnh độ mượt. Khi λ lớn, đường xu hướng mượt hơn, có lợi cho việc bắt xu hướng dài hạn; khi λ nhỏ, phản ứng nhạy hơn với biến động giá, phù hợp để bắt cơ hội trung ngắn hạn.

-

Bội số ATR có thể điều chỉnh phạm vi cắt lỗ. Có thể tối ưu cùng tham số λ: λ lớn thì nới rộng phạm vi cắt lỗ; λ nhỏ thì thu hẹp phạm vi cắt lỗ để khóa lợi nhuận nhiều hơn.

-

Tỷ lệ rủi ro/lợi nhuận (R:R) ảnh hưởng trực tiếp đến tỷ lệ lãi/lỗ. Có thể kiểm tra khả năng kiểm soát sụt giảm và lợi nhuận dưới các bội số khác nhau.

Tổng kết

Chiến lược này được thiết kế theo tư duy giao dịch theo xu hướng. Thông qua nhiều thiết lập tham số, có thể tối ưu hóa cho các khung thời gian dài, trung và ngắn khác nhau, tỷ lệ thắng và khả năng sinh lời đều mạnh. Về kiểm soát rủi ro cũng đã có những cân nhắc nhất định, đảm bảo hiệu quả rằng thua lỗ từng lệnh không quá lớn. Nhìn chung, chiến lược này sử dụng phương pháp khoa học để trích xuất đặc điểm xu hướng giá, kết hợp với đặc điểm không gian tối ưu hóa tham số lớn, triển vọng ứng dụng khá tốt.

/*backtest

start: 2024-02-17 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tathal animouse hajixde

//@version=4- 1