Chiến lược Ichimoku Cloud Nine hướng đến giao dịch

Tổng quan

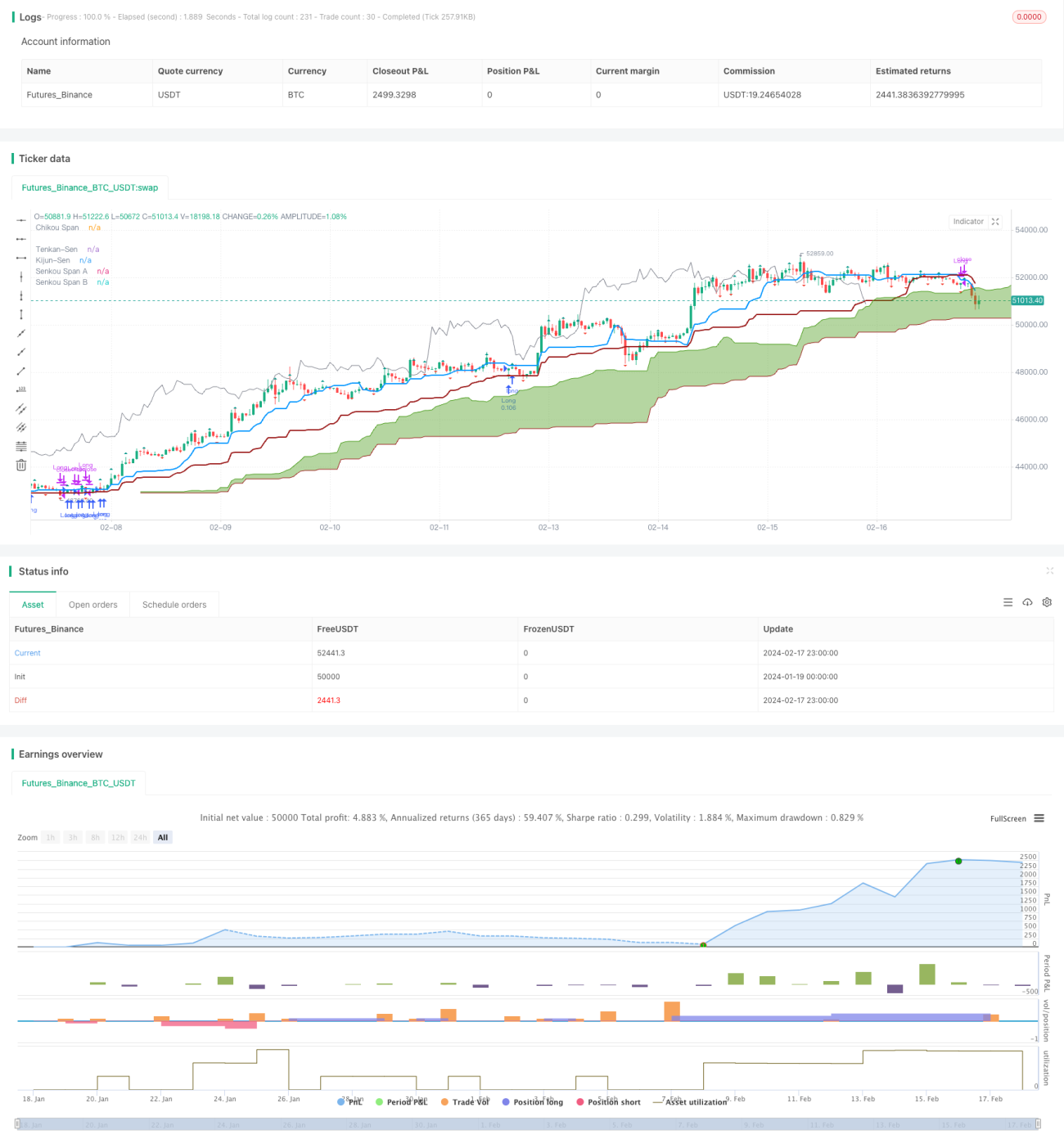

Chiến lược Ichimoku Cloud Nine là một chiến lược giao dịch dựa trên chỉ báo Ichimoku Cloud kết hợp với Fractal Williams. Chiến lược này sử dụng nhiều tín hiệu giao dịch từ chỉ báo Ichimoku Cloud để tạo ra tín hiệu giao dịch. Đây là một chiến lược hướng tới giao dịch thực tế.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa trên các tín hiệu Ichimoku sau để vào lệnh:

- Phá vỡ đám mây: Khi giá đóng cửa phá vỡ cạnh trên hoặc cạnh dưới của đám mây sẽ tạo ra tín hiệu.

- Giao cắt TK: Khi đường Tenkan (đường chuyển hướng) và đường Kijun (đường cơ sở) giao nhau sẽ tạo ra tín hiệu.

- Xoay chuyển đám mây: Khi đường Senkou Span A và đường Senkou Span B giao nhau sẽ tạo ra tín hiệu.

- Giao cắt biên: Khi giá đi từ một phía của đám mây sang phía bên kia sẽ tạo ra tín hiệu.

Ngoài ra, chiến lược này cũng sẽ đóng lệnh trong các trường hợp sau:

- Đóng lệnh khi giá đóng cửa đi vào vùng đám mây.

- Đóng lệnh khi có giao cắt ngược của TK.

- Đóng lệnh một phần khi Fractal Williams bị phá vỡ.

Chiến lược này kết hợp nhiều tín hiệu giao dịch từ biểu đồ Ichimoku Cloud, nhằm nâng cao độ tin cậy của tín hiệu giao dịch, đồng thời sử dụng Fractal để thiết lập cắt lỗ, kiểm soát rủi ro.

Lợi thế của chiến lược

So với các chiến lược chỉ sử dụng một tín hiệu, chiến lược này tận dụng tổng hợp nhiều tín hiệu từ biểu đồ Ichimoku Cloud, có thể lọc bỏ một số tín hiệu sai lệch, nâng cao độ chính xác của tín hiệu. Đồng thời, các tham số của chiến lược có thể được cấu hình linh hoạt, phù hợp với nhiều loại sản phẩm và tối ưu hóa tham số.

Ngoài ra, chiến lược này đưa vào việc phá vỡ Fractal Williams để thiết lập cắt lỗ, có thể kiểm soát rủi ro chủ động hơn, khóa lợi nhuận, tránh thua lỗ lớn.

Rủi ro của chiến lược

Chiến lược này chủ yếu đối mặt với các rủi ro sau:

- Chỉ báo biểu đồ đám mây có độ trễ, không phản ánh kịp thời sự biến động giá.

- Nhiều tín hiệu có thể quá thận trọng, bỏ lỡ một số cơ hội.

- Cắt lỗ theo Fractal có thể bị phá vỡ gây thua lỗ.

Đối với vấn đề độ trễ, có thể điều chỉnh tham số thích hợp hoặc tắt một phần tín hiệu lọc. Đối với rủi ro cắt lỗ theo Fractal, có thể điều chỉnh chu kỳ thời gian của Fractal hoặc chỉ cắt lỗ một phần.

Hướng tối ưu hóa chiến lược

Chiến lược này chủ yếu có thể được tối ưu hóa từ các khía cạnh sau:

- Điều chỉnh tham số Ichimoku để phù hợp với các chu kỳ và sản phẩm khác nhau.

- Điều chỉnh hoặc tắt một phần tín hiệu lọc, giữ lại tín hiệu cốt lõi.

- Điều chỉnh tham số của Fractal, sử dụng Fractal có chu kỳ thời gian lớn hơn, hoặc chỉ áp dụng cắt lỗ một phần.

- Thêm các chỉ báo lọc khác, chẳng hạn như chỉ báo khối lượng, v.v.

Kết luận

Chiến lược Ichimoku Cloud Nine tích hợp nhiều tín hiệu giao dịch từ biểu đồ Ichimoku Cloud, phát huy lợi thế của chỉ báo đám mây đồng thời nâng cao độ chính xác và tỷ lệ thắng của tín hiệu. Chiến lược cũng sử dụng Fractal làm phương pháp cắt lỗ để kiểm soát rủi ro. Chiến lược này có thể được tối ưu hóa thông qua tham số và tín hiệu, phù hợp cho giao dịch thuật toán đa sản phẩm.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1