Chiến lược giao dịch đảo chiều phá vỡ kênh

Tổng quan

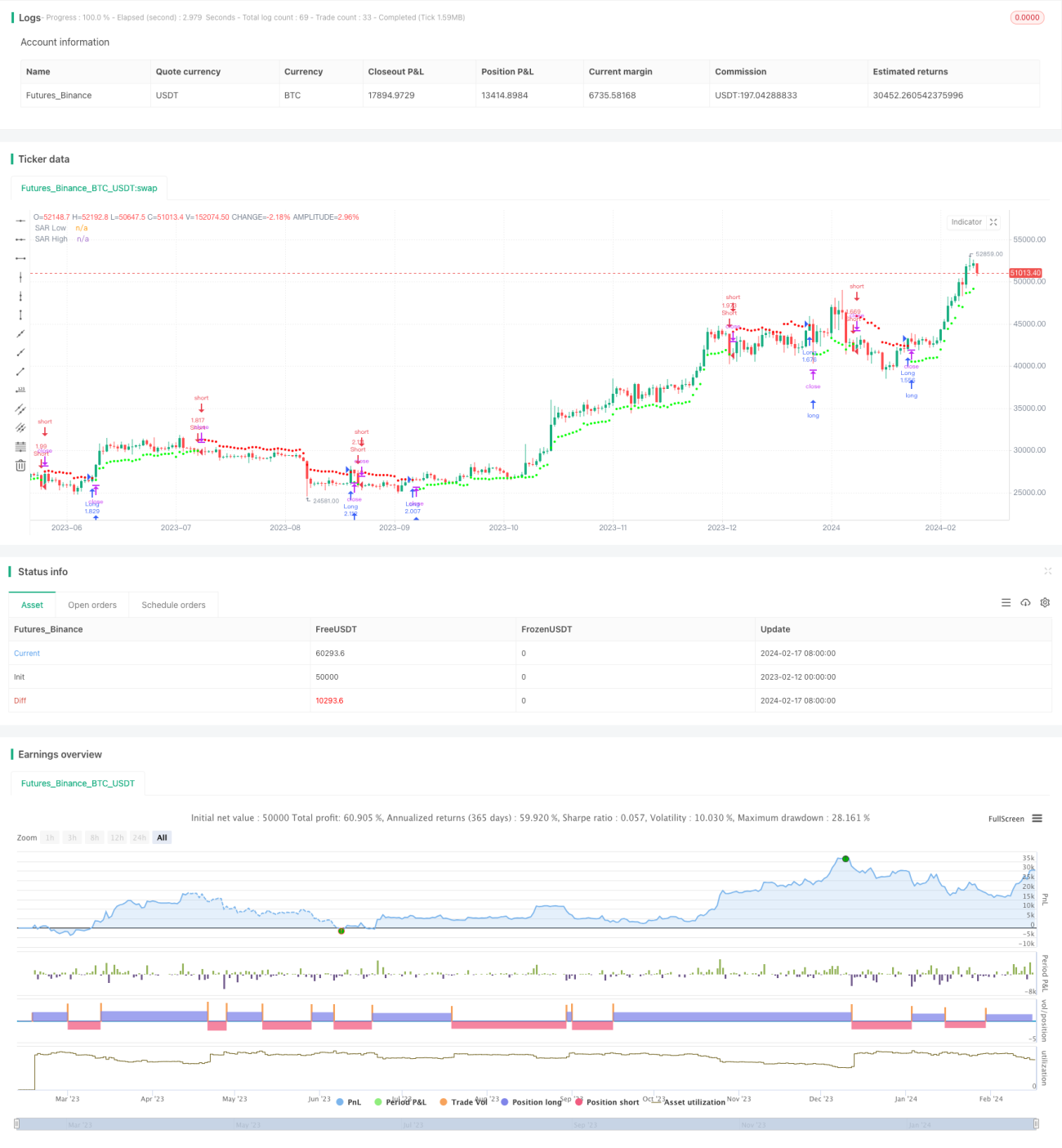

Chiến lược giao dịch đảo chiều phá vỡ kênh giá là một chiến lược giao dịch đảo chiều, sử dụng điểm chốt lời và cắt lỗ di động bám theo kênh giá. Nó tính toán kênh giá dựa trên phương pháp trung bình động có trọng số, và thiết lập vị thế mua hoặc bán khi giá phá vỡ kênh.

Nguyên lý chiến lược

Chiến lược này trước tiên tính toán biến động giá bằng chỉ báo Dải trung bình thực Wilder (ATR). Sau đó, dựa trên giá trị ATR, nó tính toán Hằng số dải trung bình (ARC). ARC chính là một nửa độ rộng của kênh giá. Tiếp theo, nó tính toán dải trên và dải dưới của kênh, tức là điểm chốt lời và cắt lỗ, gọi là điểm SAR. Khi giá phá vỡ dải trên, vào lệnh bán; khi phá vỡ dải dưới, vào lệnh mua.

Cụ thể, trước hết tính ATR của N nến gần nhất. Sau đó nhân ATR với một hệ số để có ARC. Hệ số nhân với ARC có thể kiểm soát độ rộng của kênh. Cộng ARC vào điểm cao nhất của giá đóng cửa trong N nến để có dải trên (SAR trên). Trừ ARC khỏi điểm thấp nhất của giá đóng cửa để có dải dưới (SAR dưới). Nếu giá đóng cửa phá vỡ dải trên, vào lệnh bán; nếu giá đóng cửa phá vỡ dải dưới, vào lệnh mua.

Ưu điểm chiến lược

- Sử dụng biến động giá để tính kênh thích ứng, có thể theo dõi sự thay đổi của thị trường.

- Giao dịch đảo chiều, phù hợp với thị trường có xu hướng đảo chiều.

- Chốt lời và cắt lỗ di động, có thể khóa lợi nhuận và kiểm soát rủi ro.

Rủi ro chiến lược

- Giao dịch đảo chiều dễ bị kẹt lệnh, cần điều chỉnh tham số phù hợp.

- Trong thị trường biến động mạnh, dễ bị đóng vị thế sớm.

- Tham số không phù hợp có thể gây ra giao dịch quá thường xuyên.

Giải pháp:

- Tối ưu chu kỳ ATR và hệ số ARC để độ rộng kênh hợp lý.

- Kết hợp chỉ báo xu hướng để lọc thời điểm vào lệnh.

- Tăng chu kỳ ATR, giảm tần suất giao dịch.

Hướng tối ưu hóa chiến lược

- Tối ưu chu kỳ ATR và hệ số ARC.

- Thêm điều kiện mở lệnh, ví dụ kết hợp chỉ báo MACD.

- Thêm chiến lược cắt lỗ.

Tổng kết

Chiến lược giao dịch đảo chiều phá vỡ kênh giá sử dụng kênh giá để theo dõi biến động giá, đảo chiều vào lệnh khi biến động gia tăng, và thiết lập điểm chốt lời và cắt lỗ di động thích ứng. Chiến lược này phù hợp với thị trường đi ngang chủ yếu đảo chiều, nếu xác định chính xác điểm đảo chiều, có thể đạt được lợi nhuận đầu tư khả quan. Tuy nhiên cần chú ý tránh điểm cắt lỗ quá rộng và vấn đề tối ưu tham số.

- 1