Dựa trên chiến lược đột phá động lượng

Tổng quan

Chiến lược đột phá động lượng là một chiến lược xu hướng theo dõi động lượng thị trường. Nó kết hợp nhiều chỉ báo để xác định xem thị trường hiện đang trong xu hướng tăng hay giảm, và mở vị thế mua khi giá phá vỡ các mức kháng cự quan trọng, mở vị thế bán khi giá phá vỡ các mức hỗ trợ quan trọng.

Nguyên lý chiến lược

Chiến lược này chủ yếu xác định xu hướng thị trường và các mức giá quan trọng thông qua việc tính toán các kênh Donchian với nhiều độ dài khác nhau. Cụ thể, khi giá vượt lên trên dải trên của kênh Donchian chu kỳ dài (ví dụ 40 ngày), nó được xác định là xu hướng tăng, và trên cơ sở đó kết hợp với các điều kiện lọc như mức cao nhất trong năm, sự sắp xếp hướng của đường trung bình động để phát tín hiệu mua. Ngược lại, khi giá phá vỡ dải dưới của kênh Donchian chu kỳ dài, nó được xác định là xu hướng giảm, kết hợp với các điều kiện lọc như mức thấp nhất trong năm để phát tín hiệu bán.

Về việc thoát vị thế, chiến lược cung cấp hai lựa chọn: đường cắt lỗ cố định và trailing stop. Đường cắt lỗ cố định được thiết lập dựa trên kênh Donchian chu kỳ ngắn hơn (ví dụ 20 ngày). Trailing stop được tính toán linh hoạt hàng ngày dựa trên giá trị ATR. Cả hai phương pháp dừng lỗ này đều kiểm soát rủi ro tốt.

Phân tích ưu điểm

Chiến lược này kết hợp xác định xu hướng và giao dịch đột phá, có thể nắm bắt hiệu quả các cơ hội hướng trong ngắn và trung hạn. So với các chỉ báo đơn lẻ, nó sử dụng tổng hợp nhiều điều kiện lọc, giúp lọc bỏ một phần các phá vỡ giả, từ đó nâng cao chất lượng tín hiệu vào lệnh. Ngoài ra, việc áp dụng chiến lược dừng lỗ cũng giúp nó có khả năng chịu đựng tốt hơn, ngay cả khi thị trường điều chỉnh ngắn hạn cũng có thể kiểm soát tổn thất hiệu quả.

Phân tích rủi ro

Rủi ro chính của chiến lược này là thị trường có thể biến động mạnh, dẫn đến việc kích hoạt dừng lỗ khiến thoát vị thế. Lúc đó, nếu thị trường đảo chiều nhanh chóng, có thể bỏ lỡ cơ hội. Ngoài ra, việc sử dụng nhiều điều kiện lọc cũng sẽ lọc bỏ một số cơ hội, làm giảm tần suất nắm giữ vị thế của chiến lược.

Để giảm rủi ro, có thể điều chỉnh giá trị ATR hoặc mở rộng khoảng cách dải kênh Donchian, giúp giảm khả năng bị chạm dừng lỗ. Cũng có thể giảm bớt hoặc loại bỏ một số điều kiện lọc để tăng tần suất vào lệnh, nhưng rủi ro cũng sẽ tăng lên.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

- Tối ưu hóa độ dài của kênh Donchian để tìm tổ hợp tham số tốt nhất.

- Thử nghiệm các loại đường trung bình động khác nhau làm chỉ báo lọc.

- Điều chỉnh hệ số nhân ATR hoặc chuyển sang dừng lỗ bằng số điểm cố định.

- Thêm nhiều chỉ báo xác định xu hướng hơn, như MACD, v.v.

- Tối ưu hóa cửa sổ xác định mức cao nhất/thấp nhất trong năm.

Bằng cách kiểm nghiệm các tham số khác nhau, có thể tìm ra tổ hợp tham số tối ưu, đạt được sự cân bằng giữa rủi ro và lợi nhuận.

Tổng kết

Chiến lược này kết hợp nhiều chỉ báo để xác định hướng xu hướng và phát tín hiệu giao dịch khi giá phá vỡ các mức quan trọng. Cơ chế dừng lỗ của nó cũng mang lại khả năng kiểm soát rủi ro mạnh mẽ. Thông qua việc tối ưu hóa thiết lập tham số, chiến lược này có thể đạt được lợi nhuận vượt trội ổn định. Nó phù hợp cho các nhà đầu tư không có nhận định rõ ràng về thị trường nhưng muốn theo dõi xu hướng.

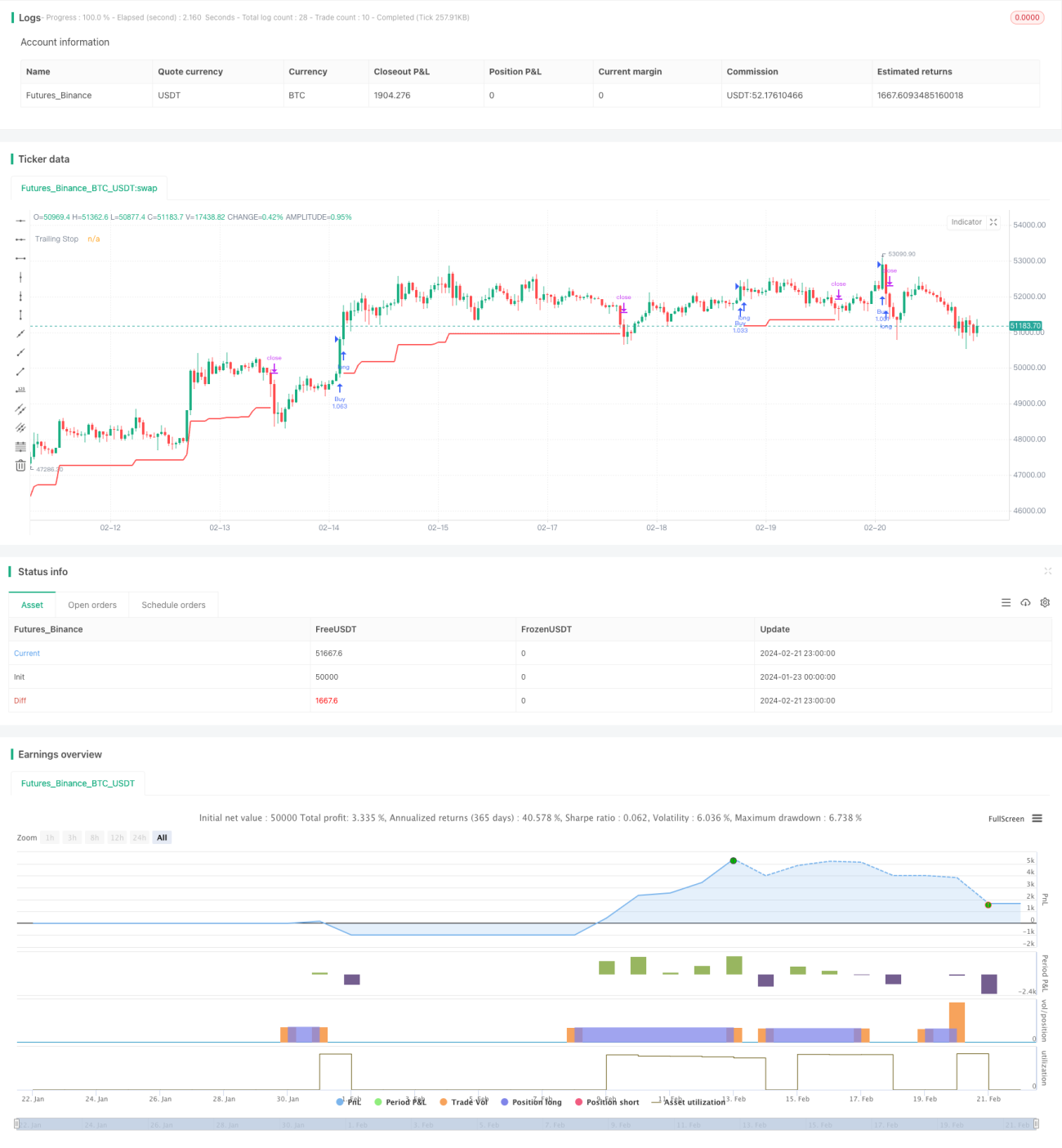

/*backtest

start: 2024-01-23 00:00:00

end: 2024-02-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1