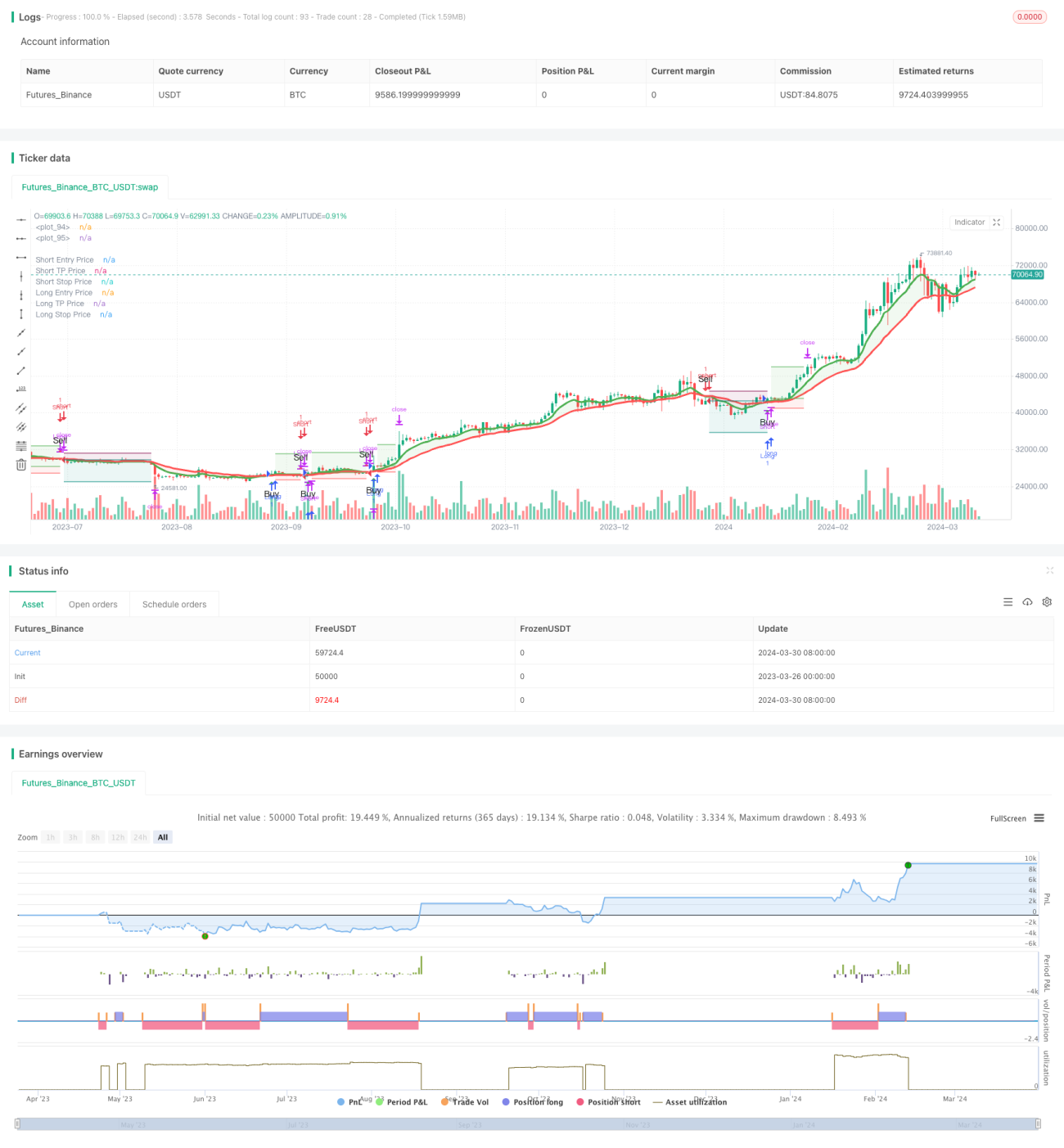

Chiến lược giao dịch động lượng với hai đường trung bình động cắt nhau

Tổng quan

Chiến lược này sử dụng đường trung bình động hàm mũ (EMA) chu kỳ 8 và 21 để xác định sự thay đổi xu hướng thị trường. Khi EMA chu kỳ ngắn hơn cắt lên trên EMA chu kỳ dài hơn, tín hiệu mua được tạo ra; ngược lại, khi EMA chu kỳ ngắn hơn cắt xuống dưới EMA chu kỳ dài hơn, tín hiệu bán được tạo ra. Chiến lược này cũng kết hợp ba đáy cao hơn liên tiếp (HLL) và ba đỉnh thấp hơn liên tiếp (LLH) làm tín hiệu xác nhận thêm cho sự đảo chiều xu hướng. Ngoài ra, chiến lược còn thiết lập các mức cắt lỗ và chốt lời để kiểm soát rủi ro và khóa lợi nhuận.

Nguyên lý chiến lược

- Tính EMA chu kỳ 8 và 21 để xác định hướng xu hướng chính.

- Xác định ba đáy cao hơn liên tiếp (HLL) và ba đỉnh thấp hơn liên tiếp (LLH) làm tín hiệu sớm cho sự đảo chiều xu hướng.

- Khi EMA 8 chu kỳ cắt lên trên EMA 21 chu kỳ và có sự phá vỡ HLL, tín hiệu mua được tạo ra; khi EMA 8 chu kỳ cắt xuống dưới EMA 21 chu kỳ và có sự phá vỡ LLH, tín hiệu bán được tạo ra.

- Đặt mức cắt lỗ ở mức 5% giá vào lệnh và mức chốt lời ở mức 16% giá vào lệnh để kiểm soát rủi ro và khóa lợi nhuận.

- Khi xuất hiện tín hiệu ngược lại, đóng vị thế hiện tại và mở vị thế ngược chiều.

Ưu điểm của chiến lược

- Kết hợp EMA và các mô hình giá (HLL và LLH) để xác nhận xu hướng, tăng độ tin cậy của tín hiệu.

- Thiết lập các mức cắt lỗ và chốt lời rõ ràng, giúp kiểm soát rủi ro và khóa lợi nhuận.

- Phù hợp với nhiều khung thời gian và thị trường khác nhau, có tính phổ quát nhất định.

- Logic rõ ràng, dễ hiểu và dễ triển khai.

Rủi ro của chiến lược

- Trong thị trường dao động (sideways), việc cắt lỗ thường xuyên có thể dẫn đến nhiều tín hiệu giả, gây thua lỗ.

- Các mức cắt lỗ và chốt lời cố định có thể không thích ứng được với các môi trường thị trường khác nhau, dẫn đến chi phí cơ hội tiềm ẩn hoặc thua lỗ lớn hơn.

- Chiến lược phụ thuộc vào dữ liệu lịch sử, khả năng thích ứng với các sự kiện bất ngờ hoặc thay đổi cơ bản có thể kém.

Hướng tối ưu hóa chiến lược

- Giới thiệu cơ chế cắt lỗ và chốt lời thích ứng, chẳng hạn như điều chỉnh mức cắt lỗ và chốt lời dựa trên biến động (ví dụ ATR) để thích ứng tốt hơn với các điều kiện thị trường khác nhau.

- Kết hợp các chỉ báo hoặc yếu tố khác như khối lượng giao dịch, chỉ số sức mạnh tương đối (RSI) để lọc thêm tín hiệu và tăng độ tin cậy.

- Tối ưu hóa các tham số (như chu kỳ EMA, tỷ lệ cắt lỗ/chốt lời) để tìm ra bộ tham số hoạt động tốt nhất trên thị trường hoặc mã cụ thể.

- Cân nhắc đưa vào các biện pháp quản lý rủi ro như định cỡ vị thế để kiểm soát mức độ rủi ro của mỗi giao dịch.

Tổng kết

Chiến lược này sử dụng sự giao nhau của EMA chu kỳ 8 và 21, kết hợp với các mô hình giá HLL và LLH, để xác định sự đảo chiều xu hướng và tạo ra tín hiệu giao dịch. Các quy tắc cắt lỗ và chốt lời rõ ràng giúp kiểm soát rủi ro và khóa lợi nhuận. Tuy nhiên, chiến lược có thể tạo ra tín hiệu giả trong thị trường dao động, và các mức cắt lỗ/chốt lời cố định cũng có thể không thích ứng với các môi trường thị trường khác nhau. Để cải thiện thêm, có thể xem xét đưa vào cơ chế cắt lỗ/chốt lời thích ứng, kết hợp các chỉ báo khác, tối ưu hóa tham số và áp dụng các biện pháp quản lý rủi ro. Nhìn chung, chiến lược này cung cấp một khung giao dịch dựa trên động lượng và theo xu hướng, nhưng vẫn cần được điều chỉnh và tối ưu hóa dựa trên thị trường cụ thể và sở thích cá nhân.

/*backtest

start: 2023-03-26 00:00:00

end: 2024-03-31 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Trend Following 8&21EMA with strategy tester [ukiuro7]', overlay=true, process_orders_on_close=true, calc_on_every_tick=true, initial_capital = 10000)

//INPUTS- 1