Adaptive Price Zone Reversal Trading Strategy

1. Strategy Overview

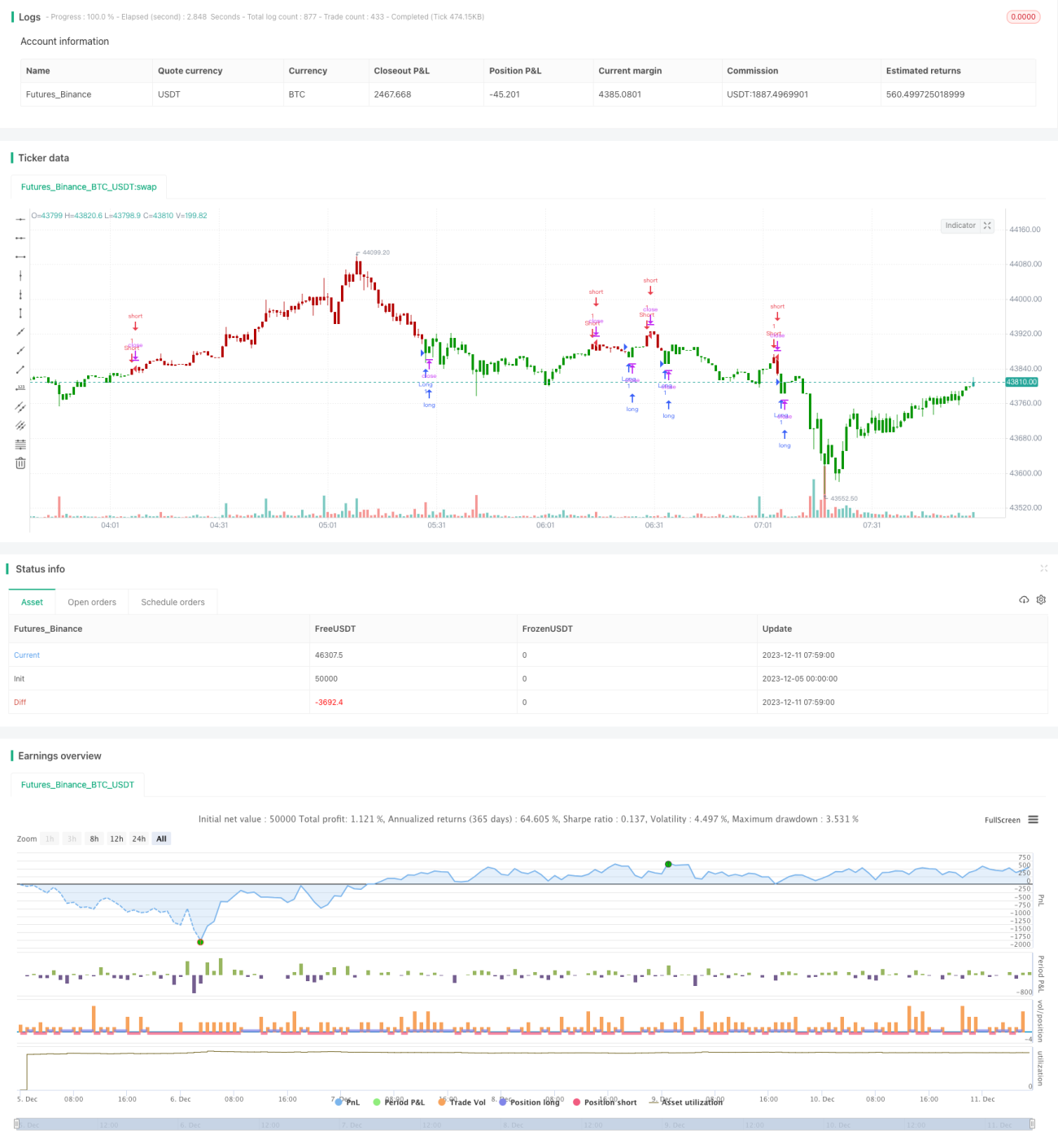

The strategy is named Adaptive Price Zone Reversal Trading Strategy. It uses the Adaptive Price Zone (APZ) indicator to identify price zones and generates trading signals when prices break out of the zones. The APZ indicator calculates upper and lower zone boundaries based on double exponential moving averages and volatility. When prices break through the boundaries, it indicates potential price reversals and trading opportunities.

The strategy is mainly suitable for range-bound markets, especially consolidation markets. It can be used for intraday or short-term trading as part of automated trading systems, and is applicable to all tradable assets. In summary, it utilizes the assistances of APZ indicator and makes reversal trades around price zone boundaries.

2. Strategy Logic

The strategy uses the APZ indicator to determine price zones, with specific calculations as follows:

- Calculate the difference between highest high and lowest low over the past n periods (default 20 periods), called xHL

- Use double exponential moving average to calculate the smoothed close price xVal1 and smoothed xHL called xVal2, with smoothing period being the rounded integer of the square root of n (square root of 20 rounded = 4)

- Calculate Upper Band = xVal1 + nBandPct * xVal2

- Calculate Lower Band = xVal1 - nBandPct * xVal2

The Upper Band and Lower Band make up the adaptive price zone. Trading signals are generated when prices break through this zone. The signal rules are as follows:

- When price drops below the Lower Band, a long signal is generated

- When price rises above the Upper Band, a short signal is generated

In addition, a reverse trading switch parameter called “reverse” is included. When reverse trading is enabled, the long and short signals work in the opposite way of the above rules.

In summary, this strategy uses the APZ indicator to determine adaptive price zones, and generates reversal trading signals when prices break out of the zone boundaries. It belongs to a typical trend reversal tracking strategy.

3. Advantage Analysis

The main advantages of this strategy are:

- The APZ indicator can adaptively determine price zones, avoiding manual setting of support and resistance

- It can make reversal trades when price breaks zone boundaries, capturing short-term price adjustment opportunities

- It allows downside trading through the reverse trading parameter

- It has relatively high trading frequency to capture more short-term opportunities

- It can be flexibly combined with stop loss strategies to control risks

4. Risk Analysis

There are also some risks with this strategy, mainly in the following areas:

- Improper APZ parameter setting may miss price reversal opportunities

- There are possibilities of multiple false breakouts in ranging markets

- Lack of stop loss strategies may lead to huge losses

The suggested mitigations are:

- Adjust APZ parameters to find suitable smoothing periods

- Use other indicators to filter out false breakouts

- Add moving stop loss to control losses for single trades

5. Optimization Directions

The strategy can be optimized in the following aspects:

- Combine with volatility indicators to determine bottom buys and top sells

- Add requirements on breakout strength, such as heavy volume

- Only trade in specific sessions, like US midday

- Incorporate moving average systems to determine overall market trend

- Set up price zones for entry, avoiding unnecessary buys and sells

6. Summary

In summary, this is a short-term reversal strategy which captures price zones using the APZ indicator and makes reversal trades around zone boundaries. The advantages are high trading frequency and ability to adaptively adjust price zones. But there are also risks of false breakouts that need to be addressed through optimizations and additional tools.

- 1