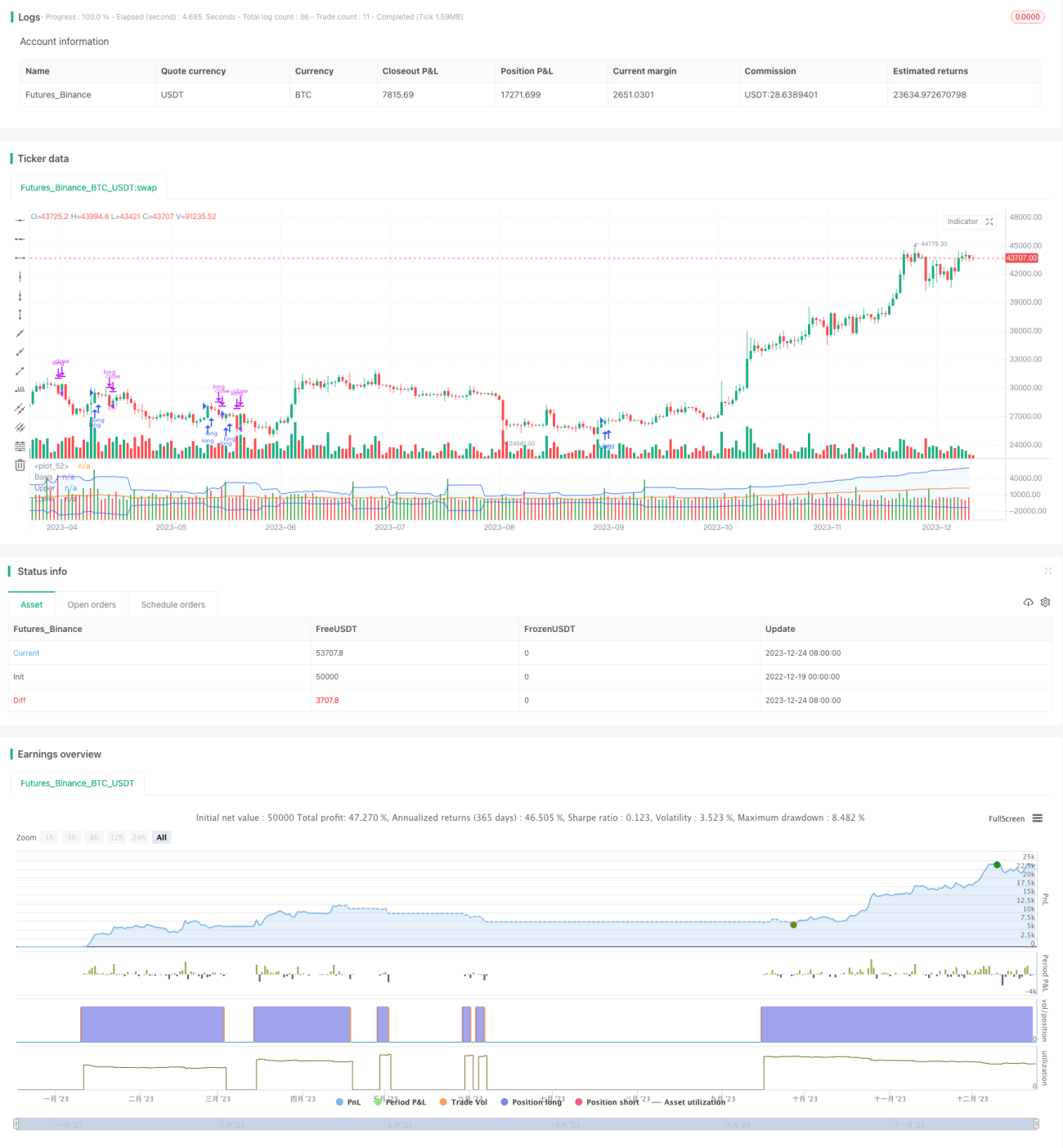

গতিশীল ক্রয়-বিক্রয়ের পরিমাণ অস্থিরতা ব্রেকআউট কৌশল

1

Follow

1802

Followers

সারসংক্ষেপ

এই কৌশলটি কাস্টম টাইম পিরিয়ডের ক্রয়/বিক্রয় ভলিউম ব্যবহার করে লং/শর্ট বিচার করে, সাথে সাপ্তাহিক VWAP ও বলিঞ্জার ব্যান্ডের ফিল্টার ব্যবহার করে উচ্চ সম্ভাবনার ট্রেন্ড অনুসরণ সম্পাদন করে। একই সাথে গতিশীল টেক প্রফিট ও স্টপ লস ব্যবস্থা সংযুক্ত করে একক দিকের ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করে।

কৌশলের নীতি

- কাস্টম টাইম পিরিয়ডের মধ্যে ক্রয়/বিক্রয় ভলিউম সূচক গণনা

- BV: ক্রয় ভলিউম, নিম্ন স্তরে কেনার মাধ্যমে সৃষ্ট ভলিউম

- SV: বিক্রয় ভলিউম, উচ্চ স্তরে বিক্রয়ের মাধ্যমে সৃষ্ট ভলিউম

- ক্রয়/বিক্রয় ভলিউম প্রক্রিয়াকরণ

- ২০-পিরিয়ড EMA দিয়ে মসৃণ করা

- প্রক্রিয়াকৃত ক্রয়/বিক্রয় ভলিউমকে ধনাত্মক ও ঋণাত্মকে পৃথক করা

- সূচকের দিক নির্ণয়

- সূচক > ০ হলে ঊর্ধ্বমুখী, < ০ হলে নিম্নমুখী

- সাপ্তাহিক VWAP ও বলিঞ্জার ব্যান্ডের সাহায্যে ডাইভারজেন্স নির্ণয়

- মূল্য VWAP-এর উপরে ও সূচক ঊর্ধ্বমুখী = লং সিগন্যাল

- মূল্য VWAP-এর নিচে ও সূচক নিম্নমুখী = শর্ট সিগন্যাল

- গতিশীল টেক প্রফিট ও স্টপ লস

- দৈনিক ATR-এর ভিত্তিতে টেক প্রফিট ও স্টপ লস শতাংশ নির্ধারণ

কৌশলের সুবিধা

- ক্রয়/বিক্রয় ভলিউম বাজারের প্রকৃত শক্তি প্রতিফলিত করে, ট্রেন্ডের সম্ভাব্য শক্তি ধারণ করে

- সাপ্তাহিক VWAP বড় সময়চক্রের ট্রেন্ড দিক নির্ণয় করে, বলিঞ্জার ব্যান্ড ব্রেকআউট সিগন্যাল নির্ধারণ করে

- গতিশীল ATR-ভিত্তিক টেক প্রফিট ও স্টপ লস সর্বোচ্চ মুনাফা লক করতে ও অতিরিক্ত সংশোধন এড়াতে সহায়তা করে

কৌশলের ঝুঁকি

- ক্রয়/বিক্রয় ভলিউম ডেটায় কিছুটা ত্রুটি থাকতে পারে, যা ভুল সিদ্ধান্তের কারণ হতে পারে

- একক সূচকের সাথে যুক্ত বিচারের কারণে ভুল সিগন্যাল উৎপন্ন হতে পারে

- বলিঞ্জার ব্যান্ডের প্যারামিটার সঠিকভাবে নির্ধারণ না করলে কার্যকর ব্রেকআউট সীমিত হয়ে যায়

কৌশল উন্নয়নের দিকনির্দেশনা

- বিভিন্ন সময়চক্রের ক্রয়/বিক্রয় ভলিউম সূচক অপ্টিমাইজ করা

- লেনদেন ভলিউমের মতো সহায়ক সূচক যুক্ত করে ফিল্টারিং করা

- বলিঞ্জার ব্যান্ডের প্যারামিটার গতিশীলভাবে সমন্বয় করে ব্রেকআউট দক্ষতা বাড়ানো

উপসংহার

এই কৌশলটি ক্রয়/বিক্রয় ভলিউমের ভবিষ্যদ্বাণী ক্ষমতার পূর্ণ ব্যবহার করে, VWAP ও বলিঞ্জার ব্যান্ডের সাহায্যে উচ্চ সম্ভাবনার সিগন্যাল তৈরি করে এবং গতিশীল টেক প্রফিট ও স্টপ লসের মাধ্যমে ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করে। এটি একটি দক্ষ ও স্থিতিশীল পরিমাণগত ট্রেডিং কৌশল। প্যারামিটার ও নিয়মের ক্রমাগত উন্নতির সাথে এর কার্যকারিতা আরও স্পষ্ট হবে বলে আশা করা যায়।

Source

Pine

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1