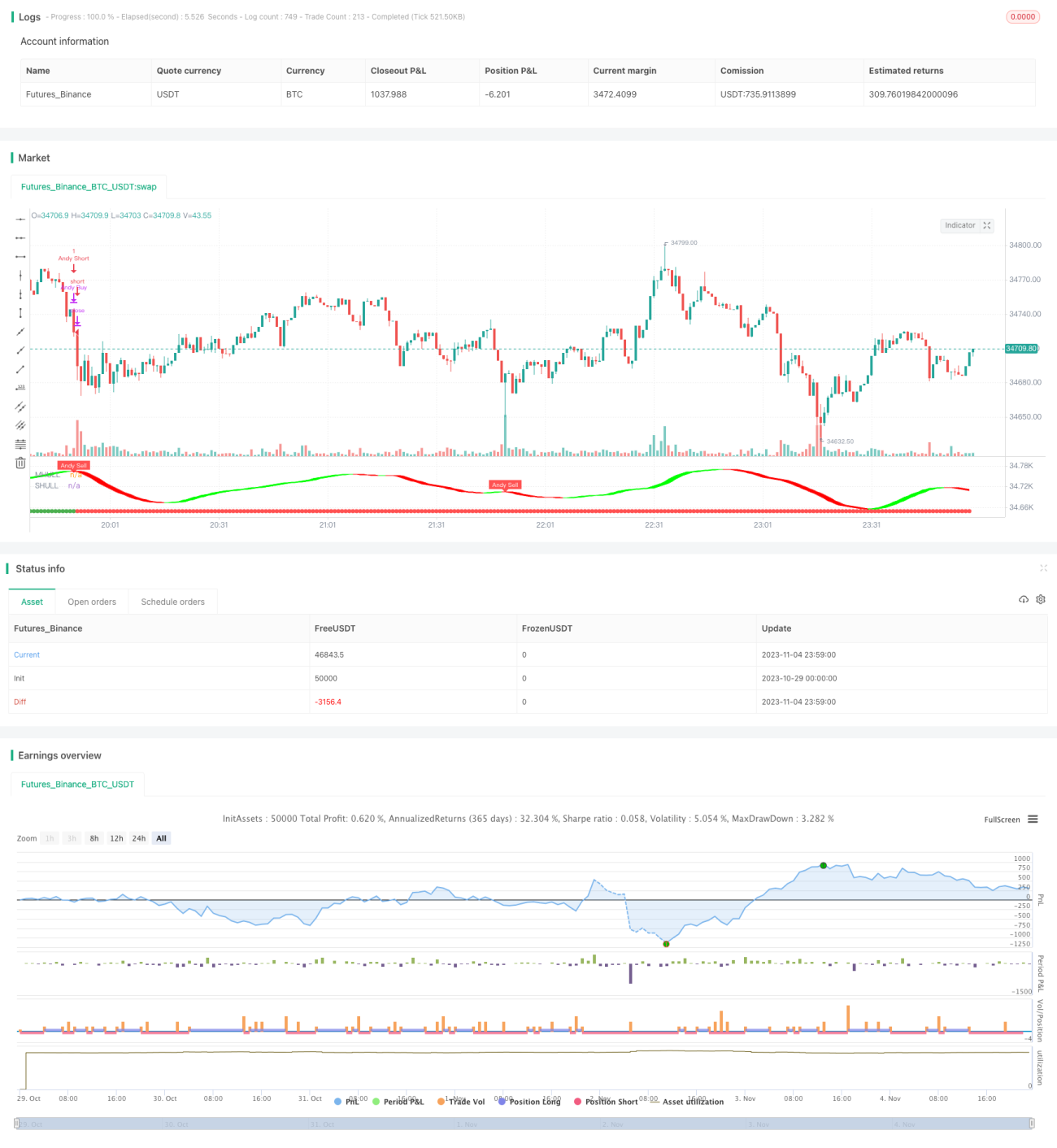

Momentum-Breakout-Trendfolge-Strategie

Übersicht

Diese Strategie kombiniert mehrere technische Indikatoren, um Trendrichtungen zu identifizieren und bei Momentum-Ausbrüchen nachzulaufen, um Überrenditen zu erzielen.

Strategieprinzip

-

Der Donchian-Kanal wird verwendet, um die allgemeine Trendrichtung zu bestimmen. Wenn der Preis diesen Kanal durchbricht, wird eine Trendwende bestätigt.

-

Der Hull Moving Average unterstützt die Trendrichtungsbestimmung. Dieser Indikator reagiert empfindlich auf Preisänderungen und kann Trendwenden frühzeitig erkennen.

-

Das Half-Track-System generiert Kauf- und Verkaufssignale. Es basiert auf Preiskorridoren und der durchschnittlichen wahren Schwankungsbreite, um Fehlausbrüche zu vermeiden.

-

Wenn der Donchian-Kanal, der Hull-Indikator und das Half-Track-System gleichzeitig Signale liefern, wird ein starker Momentum-Ausbruch erkannt. Zu diesem Zeitpunkt wird eine Position eröffnet.

-

Ausstiegsbedingung: Wenn die oben genannten Indikatoren ein gegensätzliches Signal geben, wird eine Trendumkehr festgestellt und die Position sofort mit Verlust geschlossen.

Vorteile

-

Mehrere Indikatoren kombiniert, bessere Urteilskraft. Der Donchian-Kanal bestimmt die grundlegende Richtung, Hull-Indikator und Half-Track detaillieren den genauen Wendepunkt.

-

Teilnahme an Momentum-Ausbrüchen, Streben nach Überrenditen. Nur bei starken Ausbrüchen einsteigen, um Seitwärtsbewegungen zu vermeiden.

-

Strenge Stop-Loss-Regelung schützt das Kapital. Sobald Indikatoren gegensätzliche Signale geben, sofort aussteigen, um Verluste zu begrenzen.

-

Flexible Parametereinstellung, anpassbar an verschiedene Märkte. Kanallängen, Volatilitätsbereiche usw. können für unterschiedliche Zeiträume optimiert werden.

-

Einfach zu verstehen und umzusetzen, auch für Anfänger geeignet. Die Indikatoren und Bedingungen sind klar strukturiert und leicht zu programmieren.

Risikoanalyse

-

Verpasste Chancen in der frühen Trendphase. Einstieg erfolgt relativ spät, frühe Kursgewinne werden nicht erfasst.

-

Verluste durch fehlgeschlagene Ausbrüche. Nach dem Einstieg kann ein Ausbruch scheitern und umkehren, was Verluste verursacht.

-

Falsche Signale der Indikatoren. Aufgrund falscher Parametereinstellungen können die Indikatoren falsch urteilen.

-

Begrenzte Anzahl von Trades. Nur bei eindeutigen Trendausbrüchen wird eingestiegen, die jährliche Anzahl der Trades ist begrenzt.

Optimierungsmöglichkeiten

-

Parameterkombinationen optimieren. Verschiedene Parameter testen, um die beste Kombination zu finden.

-

Stop-Loss-Linear-Rücknahmebedingung hinzufügen. Verhindert zu frühe Ausstiege, sodass Trendchancen nicht verpasst werden.

-

Weitere Indikatorfilter hinzufügen. Z. B. MACD, KDJ zur Unterstützung, um Fehlsignale zu reduzieren.

-

Handelszeitfenster optimieren. Parameter können für verschiedene Zeiträume optimiert werden.

-

Kapitalnutzungseffizienz erhöhen. Durch Hebelwirkung, Sparpläne usw. die Nutzung des Kapitals verbessern.

Zusammenfassung

Diese Strategie nutzt mehrere Indikatoren, um den Zeitpunkt eines Momentum-Ausbruchs im Trend zu erkennen, und erzielt durch das Nachlaufen etablierter Trends Überrenditen. Ein strenges Stop-Loss-System kontrolliert das Risiko, und flexible Parametereinstellungen passen sich verschiedenen Marktumgebungen an. Obwohl die Handelsfrequenz niedrig ist, strebt jeder Trade nach hohen Renditen. Durch Parameteroptimierung, Einführung zusätzlicher Indikatoren usw. kann diese Strategie kontinuierlich verbessert werden.

- 1