Doppelte CCI-Quantitativstrategie

Überblick

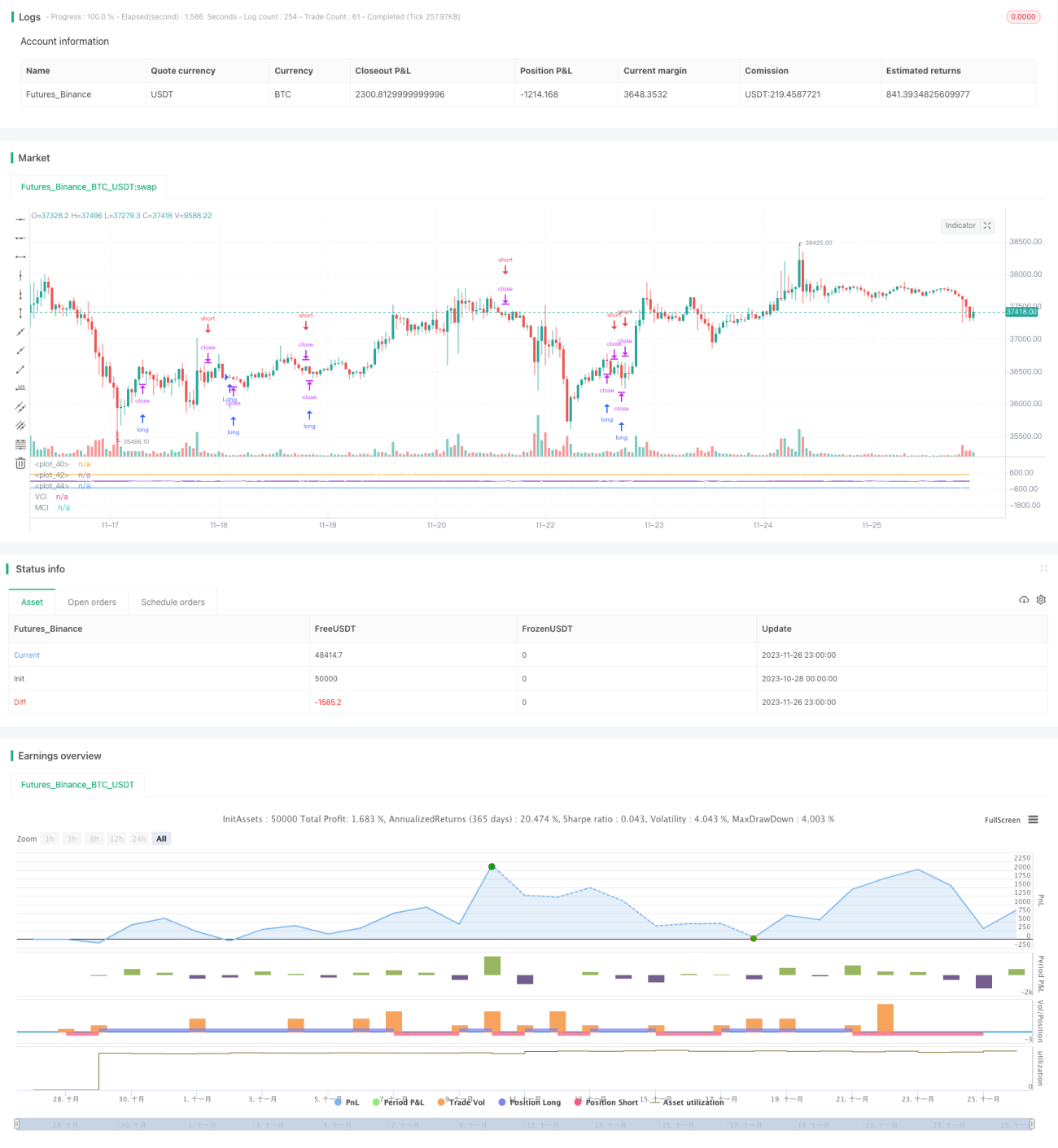

Diese Strategie generiert Handelssignale durch die Kombination des klassischen technischen Indikators CCI mit den selbst entwickelten Indizes VCI und MCI. Sie gehört zu den typischen quantitativen Handelsstrategien. Durch die Identifizierung von Trendänderungen in Volumen und Preis wird die aktuelle Hauptrichtung und -stärke des Marktes bestimmt, um Handelssignale zu erzeugen. Sie kann auf Finanzinstrumente wie Kryptowährungen, Devisen und Aktien breit angewendet werden.

Strategieprinzip

- Berechnung des gleitenden Durchschnitts von ohlc4 und Beurteilung des Kursniveaus mit dem CCI-Indikator.

- Berechnung des obv-Indikators zur Messung der Geldflüsse.

- Berechnung des VCI-Index, der die Verteilung der Geldflüsse über die Varianz des obv-Indikators misst.

- Berechnung des MCI-Index, der die Preisverteilung über die Varianz des Preises misst.

- Vergleich von VCI und MCI zur Beurteilung der Kauf-/Verkaufsstimmung:

- VCI > MCI: starke Kaufneigung

- VCI < MCI: starke Verkaufsneigung

- Generierung von Long- und Short-Signalen basierend auf dem Vergleich von VCI und MCI.

Vorteile

- Die Strategie berücksichtigt mehrere Dimensionen wie Preis, Handelsvolumen und Geldflüsse, um die Marktstimmung zu beurteilen. Die Signale sind relativ präzise.

- VCI und MCI werden mittels dynamischer Standardabweichung berechnet und passen sich an Echtzeitveränderungen des Marktes an.

- Die Parameter der Strategie wurden durch umfangreiche Backtests optimiert und weisen eine hohe Stabilität auf.

Risikoanalyse

- Die Berechnung von Preis- und Volumenindikatoren erfolgt verzögert, sodass plötzliche Ereignisse nicht vorzeitig erfasst werden können.

- Eine einzelne Strategie kann die komplexen und sich ständig ändernden Marktbedingungen nicht vollständig abdecken.

- Sie muss mit anderen ergänzenden Indikatoren kombiniert werden und kann den Markt nicht allein beurteilen.

Optimierungsmöglichkeiten

- Integration von Vorhersagemodellen wie Deep Learning zur Verbesserung der Signalgenauigkeit.

- Hinzufügen von Risikomanagementmodulen wie Stop-Loss zur Erhöhung der Stabilität.

- Testen verschiedener Parameterkombinationen, um die Anwendbarkeit in spezifischen Märkten zu prüfen.

Zusammenfassung

Diese Strategie generiert Handelssignale durch den Vergleich der beiden CCI-Indizes, berücksichtigt mehrere Faktoren wie Preis und Volumen und bewertet die Marktkraft. Sie ist eine typische und praktische quantitative Handelsstrategie. Dennoch muss sie mit anderen Hilfsinstrumenten kombiniert werden, um ihre volle Wirkung zu entfalten. Eine weitere Optimierung zur Verbesserung der Anwendungsszenarien und Risikominimierung ist empfehlenswert.

- 1