Trendfolge-Grid-Strategie

Überblick

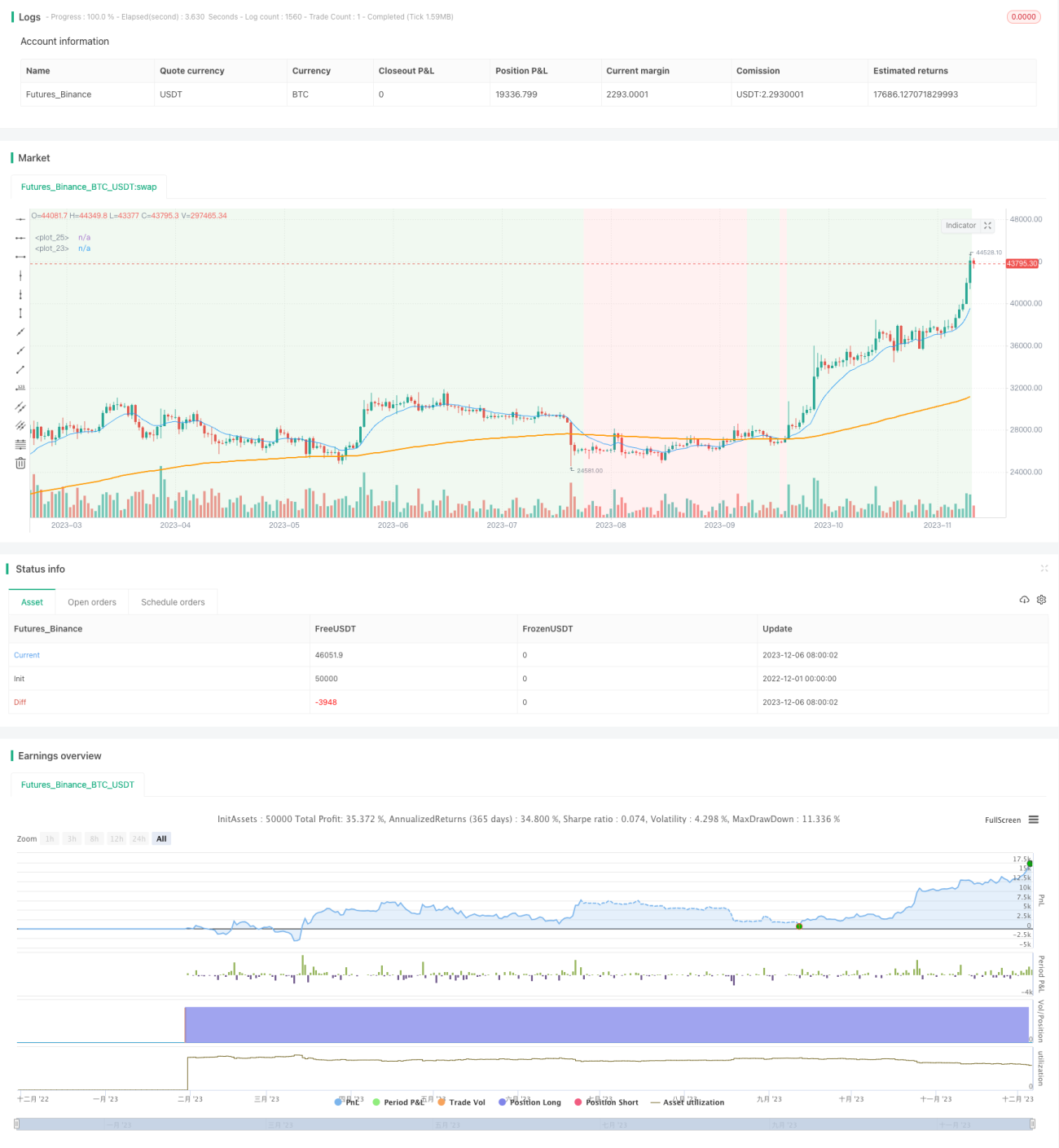

Diese Strategie ist eine reine Long-Strategie (keine Leerverkäufe), die einen Trendfolge-Grid-Ansatz für Phasen mit starkem Aufwärtstrend verwendet. Standardmäßig beträgt die Grid-Größe das 1-fache des ATR (Average True Range). Bei Abwärtsbewegungen werden die Grids der Stufen 1, 2 und 3 zur Nachverfolgung eröffnet, der 5. Grid dient als Stop-Loss. Wenn sich die Position im Leerzustand befindet und der Preis das vorherige Grid durchbricht, verschiebt sich das gesamte Grid nach oben, um dem Preis zu folgen.

Strategieprinzip

- Die Haupttrendrichtung wird mit EMA-Gleitenden Durchschnitten bestimmt: EMA12 > EMA144 zeigt einen Aufwärtstrend an.

- Es werden nur Long-Positionen eröffnet, wenn der Haupttrend aufwärts gerichtet ist.

- Die Standard-Grid-Größe beträgt das 1-fache des ATR, kann aber angepasst werden.

- Bei Abwärtsbewegungen werden die Grids der Stufen 1, 2 und 3 zur Nachverfolgung eröffnet – jeweils Long-Positionen.

- Der 5. Grid dient als Stop-Loss-Punkt.

- Nach der Eröffnung einer Position werden Stop-Loss- und Take-Profit-Punkte gesetzt.

- Wenn der Preis den Take-Profit-Punkt überschreitet, wird die Position geschlossen.

- Wenn der Preis den Stop-Loss-Punkt auslöst, wird die Position geschlossen.

- Nachdem alle Positionen geschlossen wurden, wird, sofern der Preis das letzte Grid erneut durchbricht, die Grid-Position und -Anzahl neu berechnet und nach oben verfolgt.

Die Strategie nutzt EMA zur Bestimmung der Haupttrendrichtung und kombiniert sie mit einer Grid-Strategie zur Nachverfolgung. Sie kann bei starkem Aufwärtstrend höhere Gewinne erzielen. Die Grids werden auf mehreren Preisniveaus gesetzt und die Positionen schrittweise aufgebaut, wodurch das Einzelpositionsrisiko gesenkt wird. Take-Profit und Stop-Loss ermöglichen es, Gewinne zu sichern und den maximalen Verlust zu begrenzen. Nach der vollständigen Schließung aller Positionen kann der höchste Grid-Punkt neu berechnet werden, um erneut zu eröffnen und so die Gewinne zu maximieren.

Vorteile

- Nutzung von EMA zur Bestimmung der Haupttrendrichtung, um Eröffnungen gegen den Trend zu vermeiden.

- Die Grid-Strategie ermöglicht einen schrittweisen Positionsaufbau, der das Einzelpositionsrisiko senkt.

- Take-Profit und Stop-Loss sichern Gewinne und begrenzen den maximalen Verlust.

- Nach Schließung der Positionen kann das Grid neu berechnet werden, um weiter zu kaufen und den Gewinnspielraum zu erweitern.

Der Hauptvorteil der Strategie liegt in der Kombination von Trendhandel und Grid-Handel, die sowohl die Korrektheit der Trendrichtung sicherstellt als auch die Risikostreuung der Grid-Strategie realisiert. Darüber hinaus kann durch die Neuberechnung des Grids nach der Positionsschließung unbegrenzt nachgekauft werden, was bei einem großen Kursanstieg enorme Gewinne ermöglicht.

Risikoanalyse

- Die Bestimmung des Haupttrends kann fehlerhaft sein, was zu einer falschen Richtung führt.

- Starke Seitwärtsbewegungen können zu übermäßigen Grid-Verlusten führen.

- Der Stop-Loss wird zu schnell ausgelöst, sodass alle Positionen geschlossen werden.

- Nach einer Erholung kann der optimale Einstiegspunkt nicht wieder erreicht werden.

Das Hauptrisiko liegt in einer falschen Bestimmung des Haupttrends, was zu Verlusten durch entgegengesetzte Positionen führt. Zudem können heftige Seitwärtsbewegungen mehrere Grids gleichzeitig in die Verlustzone ziehen, was die Verluste verstärkt. Ein schneller Preisrückgang und frühzeitiger Stop-Loss führen ebenfalls zur Schließung aller Positionen, sodass spätere Gewinnchancen verloren gehen. Nach einer Erholung ist es schwierig, wieder exakt in die ursprünglichen optimalen Grid-Positionen zu gelangen.

Durch Optimierung der EMA-Parameter kann die Genauigkeit der Trendbestimmung verbessert werden. Die Anpassung der Grid-Abstände und der ersten Positionsgröße kann die Gesamtverluste kontrollieren. Die Platzierung des Stop-Loss sollte die Schwankungsfrequenz des Marktes berücksichtigen. Zudem könnte man einen Teil der Positionen mit Gewinn schließen, anstatt alle Positionen aufzulösen.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen optimiert werden:

- Optimierung der EMA-Parameter zur Verbesserung der Genauigkeit der Haupttrendbestimmung.

- Anpassung der Grid-Abstände und der Anzahl der Grids zur Optimierung des Risiko-Ertrags-Verhältnisses.

- Verbesserung der Take-Profit/Stop-Loss-Logik (z. B. Teil-Profitsicherung, nachlaufender Stop-Loss usw.).

- Hinzufügen von Bedingungen für den Wiedereinstieg, um einen zu frühen Wiedereinstieg während der Erholung zu vermeiden.

- Einbeziehung weiterer Indikatoren zur Bestimmung des Einstiegszeitpunkts (z. B. Kerzenformationen, Indikatorempfindlichkeit usw.).

- Hinzufügen einer Marktausnahme-Erkennung, um große Verluste bei abnormalen Marktbewegungen zu vermeiden.

Durch diese Optimierungen kann die Strategie in großen Trends höhere Gewinne erzielen und gleichzeitig das Risiko sowie die Verluste in seitwärts gerichteten Phasen reduzieren.

Zusammenfassung

Die Strategie ist eine sinnvolle Kombination aus Trendhandel und Grid-Handel. Sie nutzt EMA zur Bestimmung der Hauptrichtung und setzt dann die Grid-Strategie ein, um schrittweise Long-Positionen aufzubauen. Das Risikomanagement ist solide, mit Take-Profit, Stop-Loss und einem Mechanismus zur Neuberechnung des Grids. Insgesamt kann die Strategie bei starken Aufwärtstrends ordentliche Gewinne erzielen und gleichzeitig das Risiko kontrollieren. Bei weiterer Optimierung der Parameter und Verbesserung der Genauigkeit könnten die Gewinne noch höher ausfallen. Die Strategie ist es wert, im Live-Handel detailliert getestet und optimiert zu werden, bevor sie eingesetzt wird.

- 1