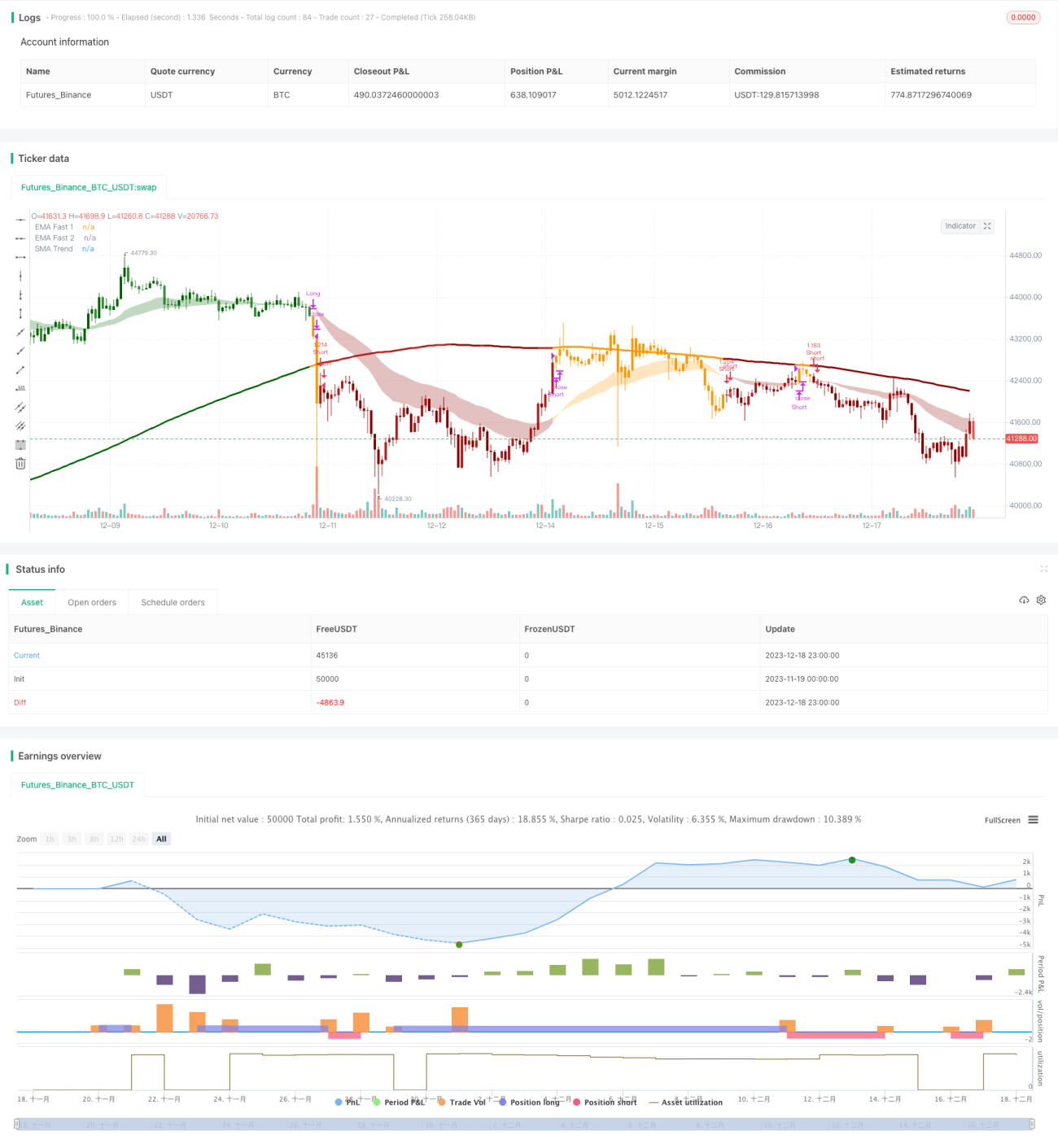

Hybride quantitative Handelsstrategie mit zwei Indikatoren

Überblick

Diese Strategie identifiziert Trendrichtungen und generiert Handelssignale durch die Kombination von Doppelindikatoren. Zunächst wird der kurzfristige Trend anhand des Kreuzzweigs von zwei gleitenden Durchschnitten (schnelle und mittlere Linie) bestimmt; anschließend wird der Haupttrend anhand einer Kanalbreite und eines langfristigen gleitenden Durchschnitts beurteilt. Nur wenn beide Bewertungen übereinstimmen, wird ein Handelssignal ausgelöst. Diese gemischte Verwendung mehrerer Indikatoren kann falsche Signale effektiv filtern und die Stabilität erhöhen.

Funktionsweise der Strategie

Die Strategie verwendet drei Gruppen von Indikatoren zur Beurteilung. Zunächst wird der kurzfristige Trend durch den Goldenen/Dead Cross der schnellen EMA (26 Perioden) und der mittleren EMA (50 Perioden) bestimmt. Zweitens wird eine Kanalbreite berechnet, um zu beurteilen, ob der Preis diese durchbricht, und so den mittelfristigen Trend (bullish/bearish) zu ermitteln. Schließlich wird der langfristige gleitende Durchschnitt SMA (200 Perioden) berechnet und mit dem Preis verglichen, um die Hauptrangrichtung zu bestimmen. Nur wenn alle drei Bewertungen übereinstimmen, wird ein Handelssignal ausgegeben.

Im Einzelnen lautet die Bewertungslogik:

- Der Kreuzung der schnellen und mittleren Linie (Goldenes Kreuz = bullisch, Todeskreuz = bärisch) bestimmt die kurzfristige Trendrichtung.

- Der Durchbruch des Preises durch die Kanalbreite bestimmt die mittelfristige Trendrichtung. Die Kanalbreite basiert auf dem langfristigen gleitenden Durchschnitt plus/minus dem ATR multipliziert mit einem Koeffizienten. Wenn der Preis die obere Grenze durchbricht, gilt dies als bullisch; wenn er die untere Grenze durchbricht, als bärisch.

- Der Vergleich des Preises mit dem langfristigen gleitenden Durchschnitt bestimmt die Hauptrangrichtung.

Schließlich wird ein Handelssignal nur dann ausgegeben, wenn alle drei Bewertungen (kurz-, mittel- und langfristig) übereinstimmen. Diese gemischte Bewertung kann falsche Signale effektiv filtern und die Stabilität erhöhen.

Vorteile der Strategie

Diese Doppelindikator-Mischstrategie bietet mehrere Vorteile:

- Effektive Filterung falscher Signale und erhöhte Stabilität, da Handelssignale von mehreren Indikatoren bestätigt werden müssen, wodurch falsche Signale einzelner Indikatoren vermieden werden.

- Hohe Flexibilität: Die Parameter der gleitenden Durchschnitte und der Kanalbreite können an verschiedene Marktumgebungen angepasst werden.

- Kombination von Trendhandel und Range-Handel: Kurz- und mittelfristige Indikatoren erfassen Trends, der langfristige Indikator definiert die Range, insgesamt werden die Vorteile von Trend- und Reversalstrategien vereint.

- Effiziente Kapitalnutzung: Aufträge werden nur ausgeführt, wenn mehrere Indikatoren übereinstimmen – dies vermeidet unnötige Trades und nutzt das Kapital effizient.

Risiken der Strategie

Die Strategie birgt auch einige Risiken:

- Risiko der Parametereinstellung: Die Perioden der gleitenden Durchschnitte und die Kanalbreite müssen angemessen gewählt werden; falsche Einstellungen können Trends nicht effektiv erkennen oder zu vielen falschen Signalen führen.

- Doppelindikator erhöht Opportunitätskosten: Im Vergleich zu Einzelindikator-Strategien können Handelsmöglichkeiten verpasst werden, sodass nicht zum optimalen Zeitpunkt ein- und ausgestiegen wird.

- Stop-Loss-Strategie muss sorgfältig abgewogen werden: Der integrierte Ausbruchs-Stop-Loss kann unnötige Verluste verursachen; der Stop-Loss-Prozentsatz sollte sorgfältig gewählt werden.

- Wirksamkeit in stark schwankenden Märkten möglicherweise geringer: Die Strategie eignet sich besser für Märkte mit klarem Trend.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen optimiert werden:

- Testen verschiedener Parameterkombinationen, um optimale Einstellungen durch umfangreiche historische Daten zu finden.

- Integration eines adaptiven Stop-Loss-Mechanismus, z. B. unter Verwendung eines Volatilitätsindikators zur dynamischen Anpassung des Stop-Loss.

- Hinzufügen eines Volumenindikators zur Unterstützung der Entscheidungen an Schlüsselpunkten, um die Kapitalnutzung zu verbessern.

- Optimierung der Einstiegslogik, z. B. durch Cost-Average-Strategie mit mehreren Teilpositionen, um das Risiko einzelner Einstiege zu reduzieren.

- Integration von maschinellen Lernmodellen (z. B. neuronale Netze) zur Beurteilung der Robustheit und Anpassungsgüte des Modells.

Zusammenfassung

Diese Strategie unterdrückt durch die dreifache Indikatorbewertung (kurz-, mittel-, langfristig) und das doppelte Bestätigungsverfahren effektiv falsche Signale und erhöht die Stabilität. Gleichzeitig vereint sie die Vorteile von Trend- und Range-Handel und nutzt das Kapital effizient. Sie kann durch Parameteroptimierung, Stop-Loss-Optimierung, Einbindung von Volumenindikatoren usw. verbessert werden und stellt eine empfehlenswerte hybride quantitative Strategie dar.

- 1