Automatisierte quantitative Handelsstrategie basierend auf internen Kerzen und gleitenden Durchschnitten

Überblick

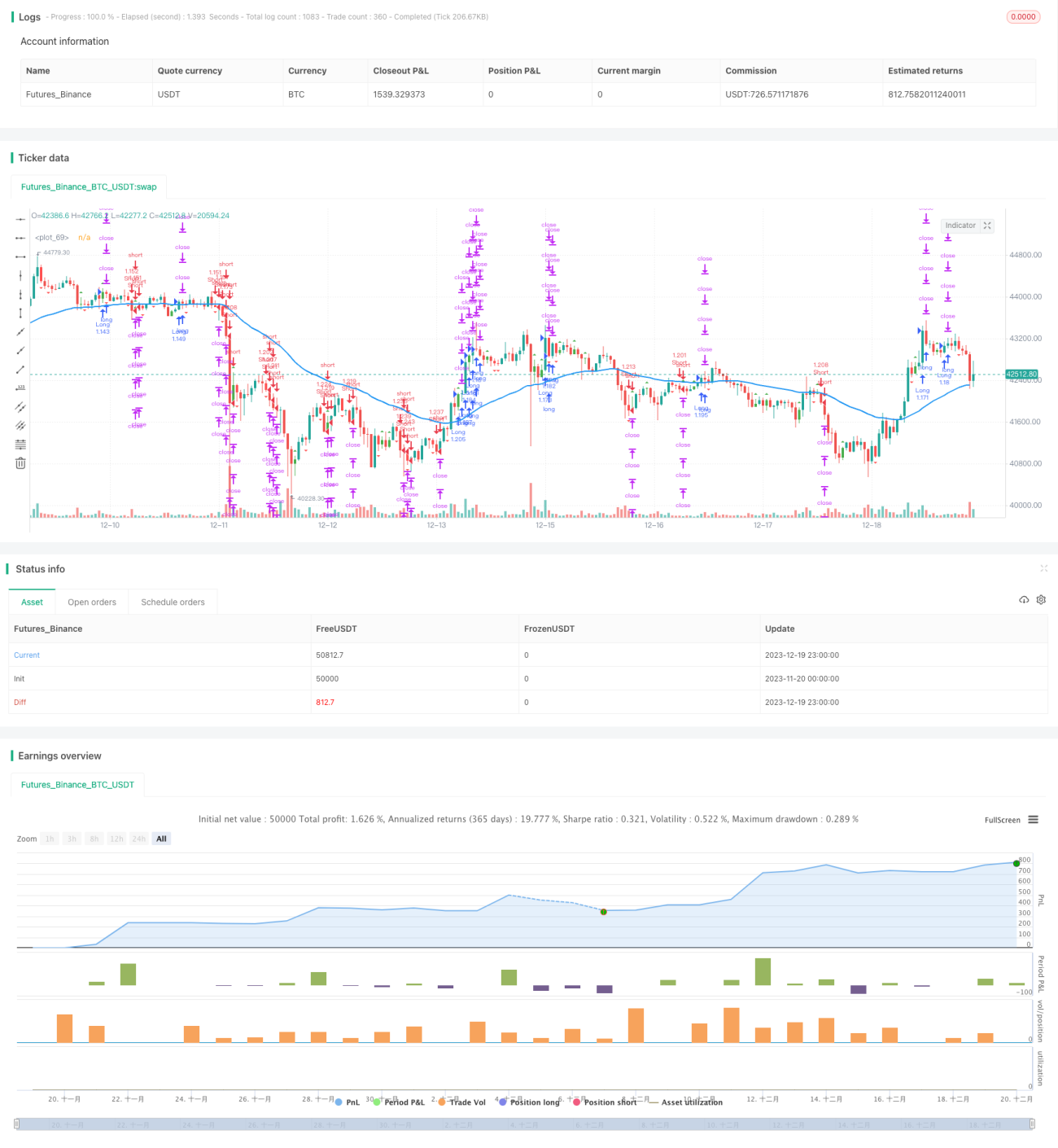

Der Kern dieser Strategie besteht darin, die Formation der Inneren Balken (Internal Bars) mit dem gleitenden Durchschnitt zu kombinieren, um automatisierte Trades zu generieren. Wenn eine Innere-Balken-Formation auftritt, deutet dies auf eine mögliche Trendwende hin. Anschließend nutzen wir die Position des gleitenden Durchschnitts, um die endgültige Handelsrichtung zu bestimmen.

Funktionsweise der Strategie

-

Suche nach Inneren Balken: Eine Innere-Balken-Formation liegt vor, wenn das Hoch und Tief einer Kerze innerhalb der Körpergrenzen (Spannweite zwischen Eröffnungs- und Schlusskurs) der vorherigen Kerze liegen. Anhand der Körperfarbe können wir zwischen einem bullischen und einem bärischen Inneren Balken unterscheiden.

-

Bestimmung der Position des gleitenden Durchschnitts: Wird ein Innerer Balken identifiziert, gilt:

- Liegt der Preis über dem gleitenden Durchschnitt, ist dies ein bullisches Signal.

- Liegt der Preis unter dem gleitenden Durchschnitt, ist dies ein bärisches Signal.

-

Kombination von Innerem Balken und gleitendem Durchschnitt: Die endgültige Handelsrichtung ergibt sich aus der Kombination:

- Ein bärischer Innerer Balken, der den gleitenden Durchschnitt nach unten durchbricht, wird als Leersignal (Short) interpretiert.

- Ein bullischer Innerer Balken, der den gleitenden Durchschnitt nach oben durchbricht, wird als Kaufsignal (Long) interpretiert.

Vorteile der Strategie

- Kombination von technischen Indikatoren und Preisformationen erhöht die Genauigkeit von Handelsentscheidungen.

- Die Innere-Balken-Formation selbst enthält ein starkes Umkehrsignal, das eine frühzeitige Identifizierung von Trendwendepunkten ermöglicht.

- Der gleitende Durchschnitt filtert Teile des Rauschens heraus und vermeidet, in Seitwärtsbewegungen gefangen zu werden.

- Vollautomatisierung des Handels reduziert den Zeit- und Arbeitsaufwand manuellen Tradings erheblich.

Risiken der Strategie und Lösungsansätze

-

Übermäßige Fehlsignale bei Seitwärtsbewegungen: Wenn sich der Preis um den gleitenden Durchschnitt herum bewegt, kann es zu vielen Fehlsignalen und damit zu übermäßigem Handel kommen.

Lösung: Optimierung der Parameter des gleitenden Durchschnitts oder Hinzufügen zusätzlicher Filterbedingungen, um Fehlsignale zu reduzieren. -

Geringere Wirksamkeit in trendlosen Märkten: Die Strategie eignet sich besser für Märkte mit ausgeprägtem Trend, in Seitwärtsphasen kann die Performance nachlassen.

Lösung: Integration eines Trendindikators wie ADX, um die Aktivierung des Algorithmus zu steuern. -

Zeitverzögerung (Lag): Es besteht eine gewisse Verzögerung bei der Signalerzeugung.

Lösung: Verkürzung der Parameter oder Optimierung der Berechnungsmethode des gleitenden Durchschnitts. -

Erhebliches Drawdown-Risiko: In ungünstigen Marktphasen können größere Verluste auftreten.

Lösung: Setzen von Stop-Losses zur Begrenzung des Verlustrisikos sowie Anpassung des Positionsmanagements zur Reduzierung des Drawdowns.

Optimierungsmöglichkeiten der Strategie

- Optimierung des Zeitrahmens für die Erkennung Innerer Balken, um die beste Parameterkombination zu finden.

- Testen verschiedener Arten gleitender Durchschnitte (z. B. EMA, SMA), um den am besten geeigneten Indikator zu ermitteln.

- Hinzufügen ergänzender Indikatoren wie MACD oder KDJ, um die Entscheidungsbasis zu erweitern und die Signaltreffsicherheit zu erhöhen.

- Integration von Filtern wie ADX oder ATR, um die Umgebungsbedingungen für den Algorithmus zu kontrollieren und einen Einsatz in ungeeigneten Märkten zu vermeiden.

- Optimierung des Positionsmanagements, z. B. durch risikobasierte Positionsgrößen oder Nachholstrategien, um das Risiko zu steuern und die Rendite zu maximieren.

Zusammenfassung

Diese Strategie realisiert ein vollautomatisches quantitatives Handelssystem, indem sie dynamisch Signale von Inneren Balken und dem gleitenden Durchschnitt verfolgt. Die Signalerzeugung ist klar und einfach zu verstehen und nachzuvollziehen. In Märkten mit deutlichem Trend zeigt die Strategie eine überdurchschnittliche Performance. Durch weitere Optimierung der Parameter und Regeln lassen sich Stabilität und Ertragskraft der Strategie noch weiter steigern.

- 1