Schnelle Handelsstrategie mit drei gleitenden Durchschnitten und niedriger Latenz

Strategieprinzip

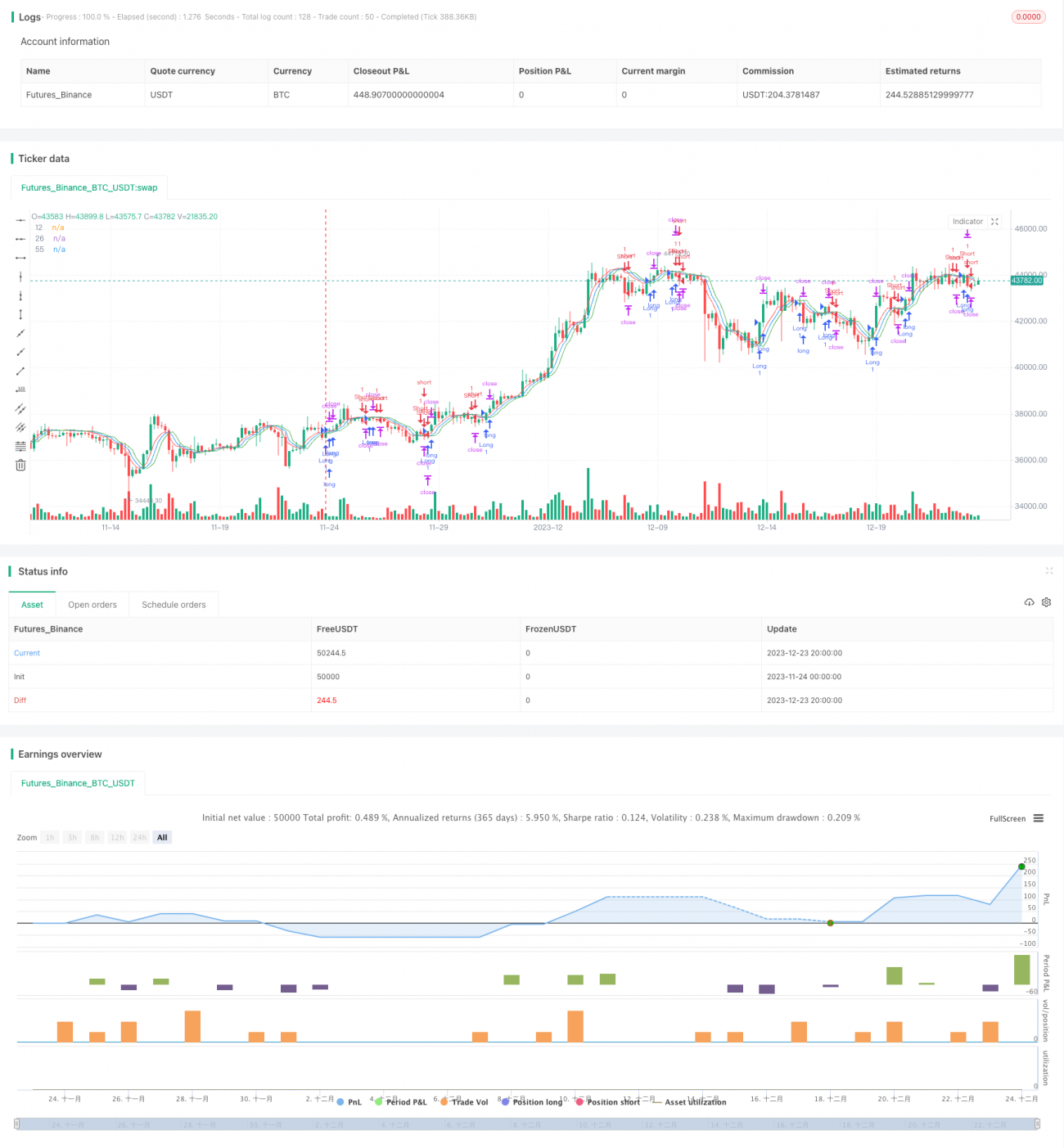

Die Strategie verwendet drei gleitende Durchschnitte mit geringer Verzögerung, darunter 12-, 26- und 55-Perioden-TEMA mit geringer Latenz. Diese drei gleitenden Durchschnitte repräsentieren den schnellen, mittleren und langsamen gleitenden Durchschnitt. Wenn der schnelle gleitende Durchschnitt den mittleren von unten nach oben kreuzt, wird ein Kaufsignal generiert; wenn der schnelle gleitende Durchschnitt den mittleren von oben nach unten kreuzt, wird ein Verkaufssignal generiert. So werden durch die Kreuze der drei gleitenden Durchschnitte die Marktein- und -ausstiegspunkte bestimmt, um einen Hochfrequenzhandel zu ermöglichen.

Im Code ist die Vorlagefunktion tema() definiert, um den TEMA mit geringer Verzögerung zu berechnen. Die Berechnungsformel lautet: TEMA = 2*EMA - EMA(EMA). Sie verwendet den exponentiell gewichteten gleitenden Durchschnitt (EWMA) zur Berechnung, im Wesentlichen einen doppelt geglätteten EMA, dessen Hauptvorteil die stark reduzierte Verzögerung ist. Dadurch kann schneller auf Preisänderungen reagiert werden, was die Aktualität der Handelssignale verbessert.

Im Einzelnen lautet die Einstiegsbedingung der Strategie: Wenn der schnelle gleitende Durchschnitt den mittleren von unten nach oben kreuzt und der schnelle gleitende Durchschnitt über dem langsamen liegt, wird ein Kaufsignal generiert; wenn der schnelle gleitende Durchschnitt den mittleren von oben nach unten kreuzt und der schnelle gleitende Durchschnitt unter dem langsamen liegt, wird ein Verkaufssignal generiert.

Vorteilsanalyse

Der größte Vorteil dieser Strategie liegt in der schnellen und genauen Bestimmung von Ein- und Ausstiegen. Das Design der drei gleitenden Durchschnitte mit geringer Verzögerung verringert die Latenz erheblich, sodass sie schnell auf Preisänderungen reagieren können. Gleichzeitig wird durch die Kreuzbestimmung mit drei gleitenden Durchschnitten Fehlinterpretationen vorgebeugt.

Darüber hinaus eignet sich die Strategie für den Hochfrequenzhandel, um Gewinne aus kurzfristigen Preisschwankungen zu erzielen. Durch das schnelle Ein- und Aussteigen kann in volatilen Märkten Gewinn erzielt werden.

Risikoanalyse

Das größte Risiko der Strategie besteht in möglichen kurzfristigen Seitwärtsbewegungen (Whipsaws). Das Design mit geringer Verzögerung macht sie äußerst empfindlich gegenüber Preisänderungen, was in bestimmten Märkten zu hochfrequenten Oszillationen führen kann. Dann besteht eine hohe Wahrscheinlichkeit, in die Falle zu tappen.

Zudem fallen beim Hochfrequenzhandel relativ hohe Gebühren und Slippage-Kosten an. Wenn die Ertragskraft nicht ausreicht, kann der Handel schnell durch die Transaktionskosten gegenteilig ausgenutzt werden.

Außerdem erfordert die Strategie vom Händler eine hohe Echtzeit-Überwachungsfähigkeit, um Stop-Loss- und Take-Profit-Punkte rechtzeitig anzupassen.

Optimierungsrichtungen

Die Strategie kann in den folgenden Bereichen optimiert werden:

-

Optimierung der Periodenparameter der drei gleitenden Durchschnitte, um sie besser an die Eigenschaften verschiedener Märkte anzupassen.

-

Hinzufügen von Volatilitätsindikatoren oder Volumenindikatoren zur Bestätigung von Signalen, um in seitwärts tendierenden Märkten nicht in die Falle zu tappen.

-

Einbeziehung weiterer Faktoren zur Einrichtung eines dynamischen Nachführ-Stopp-Mechanismus.

-

Optimierung des Positionsmanagements durch Geldmanagement-Techniken zur Kontrolle des Einzelrisikos.

-

Integration von Algorithmen des maschinellen Lernens zur dynamischen Optimierung der Strategieparameter.

Zusammenfassung

Bei dieser Strategie handelt es sich um eine schnelle Handelsstrategie mit drei gleitenden Durchschnitten und geringer Verzögerung. Durch das Design mit geringer Latenz werden schnelle Ein- und Ausstiege ermöglicht, was sie für den Hochfrequenzhandel zur Erfassung kurzfristiger Chancen geeignet macht. Der größte Vorteil dieser Strategie ist die schnelle und genaue Signalbestimmung; der größte Nachteil ist die Anfälligkeit für Seitwärtsbewegungen (Whipsaws). Dieser Artikel bietet eine umfassende Übersicht über die Handelsstrategie durch detaillierte Prinzipienanalyse, Vorteilsanalyse, Risikoanalyse und Optimierungsdiskussion.

Conclusion

Dies ist eine schnelle Handelsstrategie mit geringer Verzögerung und dreifachem gleitendem Durchschnitt. Durch ihr Design mit geringer Verzögerung können schnelle Ein- und Ausstiege erreicht werden, was sie für Hochfrequenzhandel zur Erfassung kurzfristiger Chancen geeignet macht. Der größte Vorteil dieser Strategie ist, dass ihre Signalbestimmung schnell und genau ist. Der größte Nachteil ist, dass sie in Seitwärtsmärkten anfällig für Fehlsignale (Whipsaws) ist. Dieser Artikel fasst diese Handelsstrategie umfassend durch detaillierte Analyse ihrer Grundlagen, Vorteile, Risiken und Optimierungsrichtungen zusammen.

[/trans]

/*backtest

start: 2023-11-24 00:00:00

end: 2023-12-24 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("scalping low lag tema etal", shorttitle="Scalping tema",initial_capital=10000, overlay=true)

mav = input(title="Moving Average Type", defval="temadelay", options=["nkclose", "ema", "emadelay", "fastema", "tema", "temadelay"])

lenb = 3- 1