Die Zeitreise-Mo-Fei-Indikator-Strategie

Überblick

Dies ist eine einfache quantitative Strategie, die den MoFi-Indikator nutzt, um "große Haie" im Markt zu identifizieren. Sie ist auf das 5-Minuten-Zeitfenster ausgelegt und wird hauptsächlich für den Kryptowährungshandel verwendet.

Strategieprinzip

Die Strategie verwendet den MoFi-Indikator der Länge 3, setzt die Überkauft-Linie auf 100 und die Überverkauft-Linie auf 0. Die Strategie wartet darauf, dass der MoFi-Indikator ein überkauftes Niveau erreicht, was auf die Anwesenheit eines "großen Hais" im Markt hindeutet. Wenn an einem Tag die ersten beiden MoFi-Überkauft-Signale auftreten und die Preise dennoch ihren Aufwärtstrend beibehalten können, ist dies ein Long-Einstiegssignal.

Wenn der MoFi-Indikator = 100 ist und die nächste Kerze eine große bullische Kerze ist, wird eine Long-Position eröffnet. Der Stop-Loss wird auf das Tief des Handelstages gesetzt, und der Take-Profit erfolgt innerhalb von 60 Minuten nach dem Einstieg.

Für Short-Positionen kann die gespiegelte Logik verwendet werden: Wenn der MoFi-Indikator überverkauft ist und die nächste Kerze eine große bärische Kerze ist, wird eine Short-Position eröffnet.

Strategievorteile

-

Der MoFi-Indikator kann effektiv das Verhalten von "großen Haien" identifizieren, die Potenzialwerte akkumulieren. Solche Aktien besitzen ein weiteres Aufwärtspotenzial.

-

Durch die Nutzung der Kerzenkörper (reale Balken) werden starke Ausbruchspunkte erkannt, was viele falsche Ausbrüche herausfiltern kann.

-

In Kombination mit einem SMA-Filter wird vermieden, Aktien in einem fallenden Trend zu kaufen, was das Handelsrisiko effektiv reduziert.

-

Die Verwendung einer intraday-gestützten, sehr kurzfristigen Handelsmethode mit einem 60-Minuten-Take-Profit ermöglicht es, Gewinne schnell zu sichern und die Wahrscheinlichkeit von Drawdowns zu verringern.

Strategierisiken

-

Der MoFi-Indikator kann falsche Signale erzeugen, die zu unnötigen Verlusten führen. Eine Anpassung der Parameter oder die Hinzunahme weiterer Indikatoren zur Filterung wäre sinnvoll.

-

Die 60-Minuten-Handelsmethode (sehr kurzfristig) könnte zu aggressiv sein und ist für Aktien mit hoher Volatilität weniger geeignet. Eine Anpassung der Take-Profit-Zeit oder der Einsatz eines Trailing-Stopps könnten optimieren.

-

Es werden keine schwerwiegenden makroökonomischen Ereignisse berücksichtigt, die Markterschütterungen verursachen können. In solchen Fällen sollte die Strategie pausiert werden, bis sich der Markt wieder stabilisiert hat.

Optimierungsrichtungen

-

Es können verschiedene Parameterkombinationen getestet werden, z. B. die Länge des MoFi-Indikators anpassen oder die SMA-Periodenparameter optimieren.

-

Versuchen Sie, weitere Indikatoren wie Bollinger-Bänder oder den Stochastik-Indikator (KD) hinzuzufügen, um die Signalgenauigkeit zu verbessern.

-

Testen Sie, ob eine etwas großzügigere Stop-Loss-Spanne zu höheren Einzelgewinnen führen kann.

-

Entwickeln Sie auf Basis dieses Strategierahmens Versionen für andere Zeitrahmen, z. B. für 15 oder 30 Minuten.

Zusammenfassung

Die Strategie ist insgesamt sehr einfach und leicht verständlich. Die grundlegende Idee stimmt mit der klassischen Jagd auf den "großen Hai" überein. Durch die Identifizierung der Schlüsselpunkte des MoFi-Indikators (überkauft/überverkauft) in Kombination mit der Filterung durch die Kerzenkörper können viele Störsignale herausgefiltert werden. Die Hinzunahme des SMA-Filters erhöht zudem die Stabilität der Strategie.

Die sehr kurzfristige Handelsmethode mit 60 Minuten ermöglicht schnelle Gewinne, birgt aber auch ein höheres Betriebsrisiko. Insgesamt handelt es sich um eine quantitativ umsetzbare Strategievorlage mit hohem praktischem Wert, die eine gründliche Untersuchung und Optimierung verdient. Sie bietet zudem wertvolle Denkanstöße für die Strategieentwicklung.

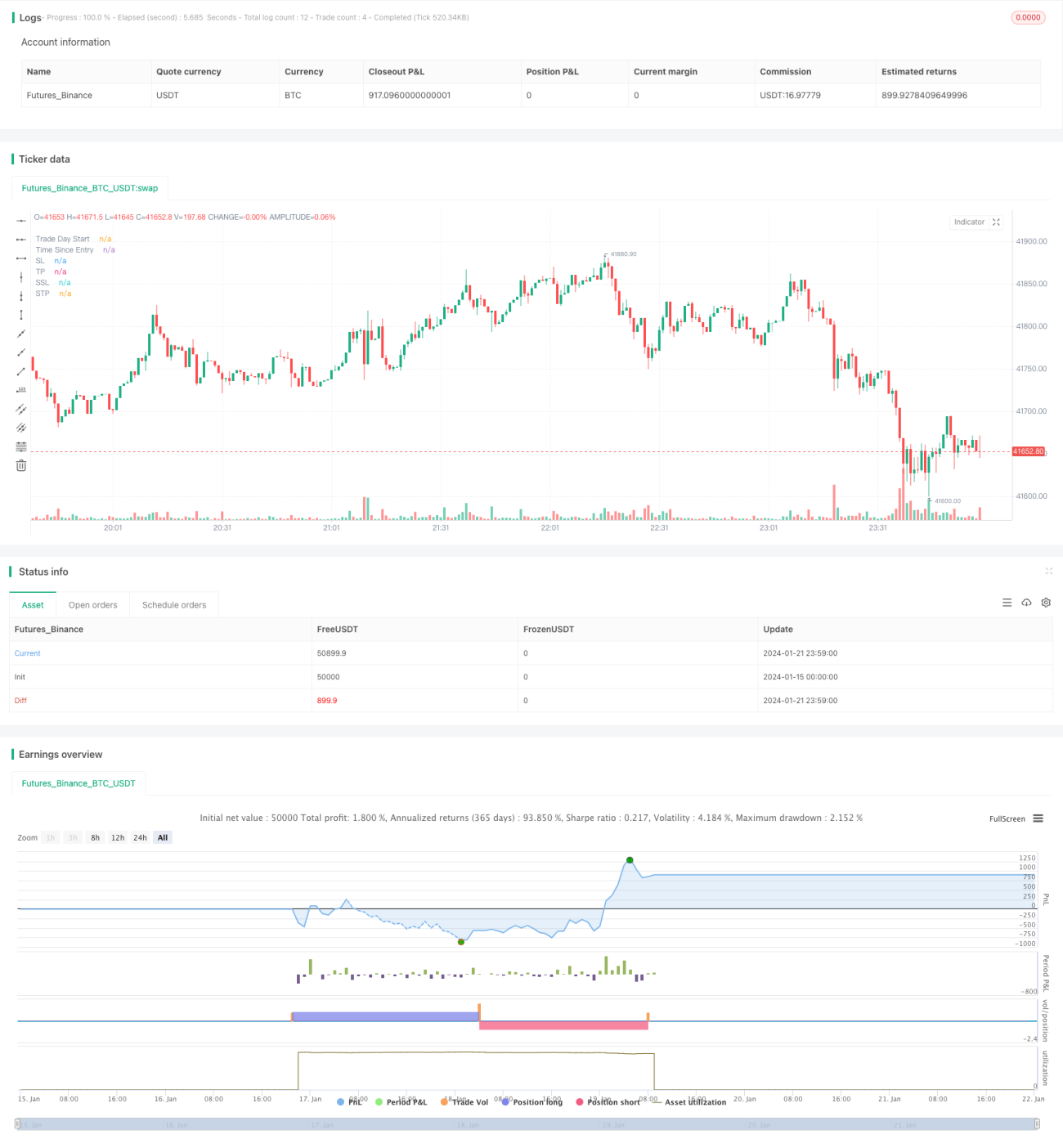

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1