Trendfolgestrategie mit doppeltem gleitendem Durchschnitt und Preiskanal

Überblick

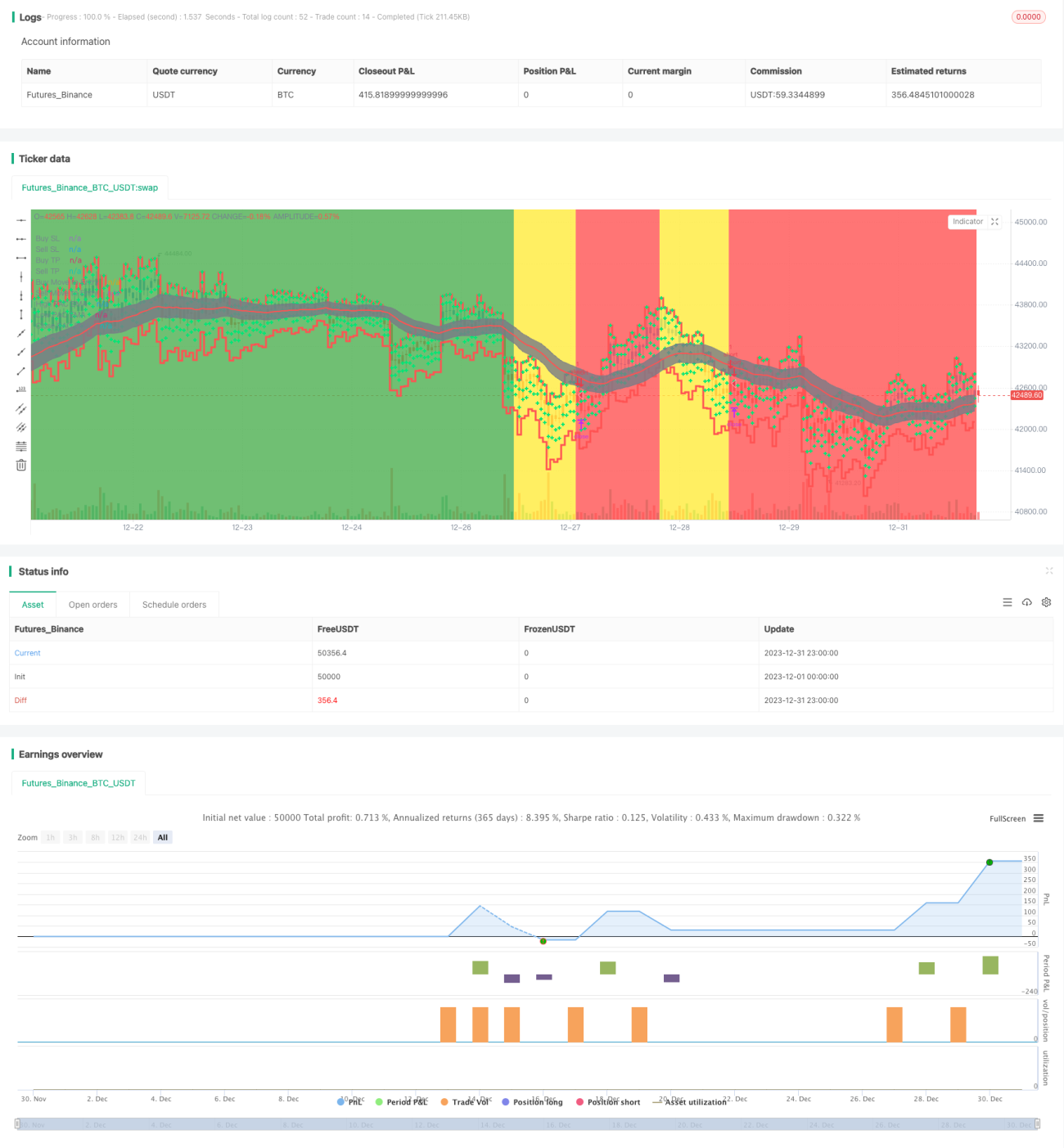

Diese Strategie basiert auf der Konstruktion eines Preiskanals mit doppelten gleitenden Durchschnitten, nutzt die Kanalbereiche, um die Richtung des Preistrends zu bestimmen, und setzt einen Trailing-Stop zur Sicherung von Gewinnen ein. Es handelt sich um eine Trendfolgestrategie.

Funktionsweise der Strategie

Die Strategie des doppelten gleitenden Durchschnitts-Preiskanals verwendet einen schnellen EMA und einen langsamen EMA, um den Preiskanal zu bilden. Der schnelle EMA hat einen Parameter von 89 Perioden, der langsame EMA von 200 Perioden. Gleichzeitig werden drei gleitende Durchschnitte basierend auf Hoch-, Tief- und Schlusskursen verwendet, um den Bereich des Preiskanals zu definieren. Die obere und untere Kanalgrenze sind der 34-Perioden-EMA des Hoch- bzw. Tiefkurses.

Wenn der schnelle EMA über dem langsamen EMA liegt und der Preis unter der unteren Grenze liegt, wird ein Aufwärtstrend angenommen; wenn der schnelle EMA unter dem langsamen EMA liegt und der Preis über der oberen Grenze liegt, wird ein Abwärtstrend angenommen.

Im Aufwärtstrend geht die Strategie eine Leerverkaufsposition ein, sobald eine Trendumkehr bestätigt wird; im Abwärtstrend geht sie eine Long-Position ein, sobald eine Trendumkehr bestätigt wird.

Darüber hinaus verfügt die Strategie über eine Trailing-Stop-Funktion. Nach dem Eingehen einer Position wird der Trailing-Stop-Preis kontinuierlich aktualisiert, um Gewinne zu sichern.

Vorteile

Der größte Vorteil dieser Strategie liegt in der Nutzung des doppelten gleitenden Durchschnitts-Preiskanals zur Bestimmung des Preistrends, kombiniert mit dem Eingehen von Positionen bei Trendumkehr, um Kaufen zu Höchst- und Verkaufen zu Tiefstkursen zu vermeiden. Gleichzeitig ermöglicht die integrierte Trailing-Stop-Funktion die Sicherung von Gewinnen und die Reduzierung von Verlustrisiken.

Weitere Vorteile sind: Großer Spielraum für Parameteroptimierung, der an verschiedene Instrumente und Zeiträume angepasst werden kann; ständige Aktualisierung des Stop-Preises, was das Betriebsrisiko senkt.

Risikoanalyse

Das Hauptrisiko dieser Strategie liegt in der möglicherweise unzureichenden Effektivität der Umkehrsignale, was zu Fehleinschätzungen führen kann. In diesem Fall müssen die Parameter optimiert werden, um eine zuverlässige Erkennung von Trendumkehrungen zu gewährleisten.

Darüber hinaus ist die Einstellung des Stop-Loss-Kurses entscheidend. Ein zu großer Stop-Loss kann zu nicht rechtzeitigem Stoppen führen; ein zu kleiner Stop-Loss kann zu übermäßigen Stopps führen. Dies muss je nach spezifischem Instrument angepasst werden.

Schließlich können auch Datenprobleme zum Versagen der Strategie führen. Es muss sichergestellt werden, dass zuverlässige, kontinuierliche und ausreichende historische Daten für Backtesting und Live-Validierung verwendet werden.

Optimierungsmöglichkeiten

Die Optimierung dieser Strategie konzentriert sich hauptsächlich auf die folgenden Aspekte:

-

Die Perioden des schnellen und langsamen EMA können optimiert werden, indem verschiedene Parameterkombinationen getestet werden.

-

Die Parameter der oberen und unteren Kanalgrenzen können ebenfalls angepasst werden, um geeignetere Perioden zu finden.

-

Die Einstellung des Stop-Loss-Kurses ist entscheidend. Verschiedene Parameter können getestet werden, um die Stop-Strategie zu optimieren.

-

Es kann getestet werden, ob andere Indikatoren zur Bestimmung von Trendumkehrungen einbezogen werden, um die Handelseffektivität zu verbessern.

Zusammenfassung

Diese Strategie hat einen insgesamt logischen und reibungslosen Ablauf, nutzt den doppelten gleitenden Durchschnitts-Preiskanal zur Bestimmung der Trendrichtung und sichert Gewinne durch einen Trailing-Stop. Sie ist eine relativ stabile Trendfolgestrategie. Durch Parameteroptimierung und Verbesserung der Risikokontrolle kann diese Strategie zu einer effizienten quantitativen Handelsstrategie werden.

- 1