Estrategia de seguimiento de tendencia con ruptura de impulso

Resumen

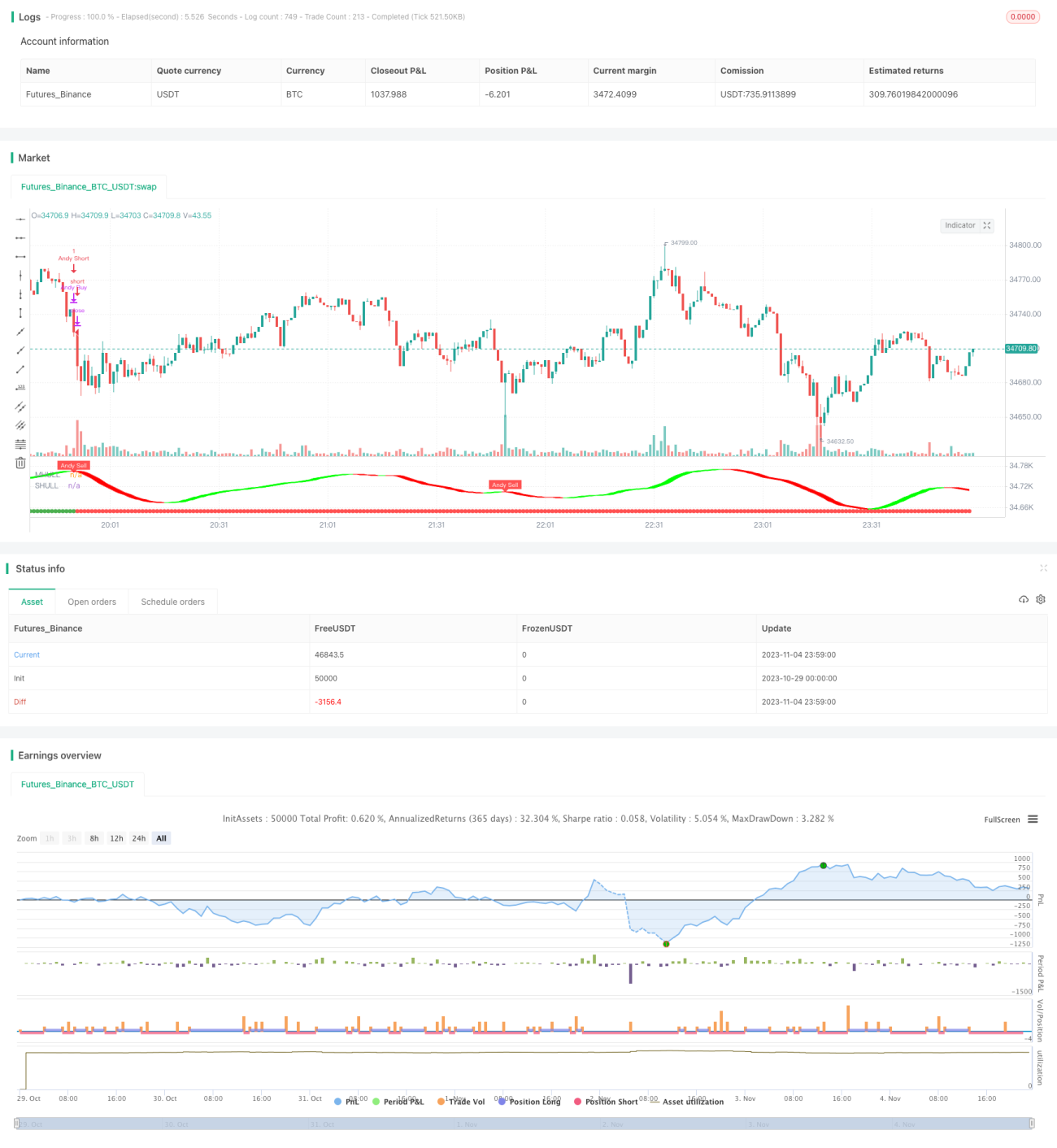

Esta estrategia utiliza múltiples indicadores técnicos para identificar la dirección de la tendencia y realiza un seguimiento cuando se produce una ruptura de impulso en la tendencia, buscando obtener rendimientos excesivos.

Principio de la estrategia

-

Utiliza el canal de Donchian para determinar la dirección general de la tendencia. Cuando el precio rompe este canal, se confirma un cambio de tendencia.

-

La media móvil Hull ayuda a juzgar la dirección de la tendencia. Este indicador es sensible a los cambios de precio y puede detectar giros de tendencia con anticipación.

-

El sistema de media órbita genera señales de compra y venta. Este sistema se basa en canales de precio y el rango verdadero promedio, evitando falsas rupturas.

-

Cuando el canal de Donchian, el indicador Hull y el sistema de media órbita emiten señales simultáneamente, se determina una ruptura de impulso fuerte de la tendencia, momento en el que se ingresa al mercado.

-

Condición de cierre: cuando los indicadores anteriores emiten una señal opuesta, se determina una reversión de la tendencia y se sale inmediatamente con stop loss.

Análisis de ventajas

-

Combinación de múltiples indicadores para un juicio más sólido. El canal de Donchian determina el panorama general, mientras que Hull y la media órbita analizan los detalles, capturando puntos de giro precisos de la tendencia.

-

Participación en rupturas de impulso para buscar rendimientos excesivos. Solo se ingresa cuando la tendencia tiene una ruptura fuerte, evitando quedar atrapado en movimientos laterales.

-

Stop loss estricto para proteger el capital. Tan pronto como los indicadores emiten una señal contraria, se aplica el stop loss para evitar pérdidas mayores.

-

Parámetros ajustables para adaptarse a varios mercados. Se pueden modificar la longitud del canal, el rango de volatilidad, etc., para optimizar según diferentes períodos.

-

Fácil de entender e implementar, incluso para principiantes. La combinación de indicadores y condiciones es simple y clara, fácil de programar.

Análisis de riesgos

-

Se pierden oportunidades al inicio de la tendencia. El momento de entrada es tardío, no se capturan las ganancias iniciales.

-

Pérdidas por fallo de ruptura y reversión. Después de la entrada, puede ocurrir una ruptura fallida y un giro, causando pérdidas.

-

Señales erróneas de los indicadores. Debido a una configuración inadecuada de los parámetros, los indicadores pueden dar juicios incorrectos.

-

Número limitado de operaciones. Solo se ingresa en rupturas claras de tendencia, lo que limita las operaciones anuales.

Direcciones de optimización

-

Optimizar la combinación de parámetros. Probar diferentes parámetros para encontrar la mejor combinación.

-

Agregar condiciones de retroceso lineal para el stop loss. Evitar salidas demasiado tempranas que pierdan oportunidades de tendencia.

-

Incorporar filtros de otros indicadores. Como MACD, KDJ, etc., para ayudar a reducir señales falsas.

-

Optimizar los períodos de negociación. Los parámetros pueden optimizarse para diferentes franjas horarias.

-

Mejorar la eficiencia del uso del capital. Mediante apalancamiento, inversión periódica, etc., aumentar la eficiencia del uso de fondos.

Conclusión

Esta estrategia combina múltiples indicadores para identificar el momento de ruptura de impulso en la tendencia, y busca rendimientos excesivos siguiendo la tendencia establecida. Un riguroso mecanismo de stop loss controla el riesgo, y los parámetros flexibles se adaptan a diferentes entornos de mercado. Aunque la frecuencia de negociación es baja, cada operación busca obtener altos rendimientos. Mediante la optimización de parámetros, la incorporación de indicadores auxiliares, etc., esta estrategia puede mejorarse continuamente.

- 1