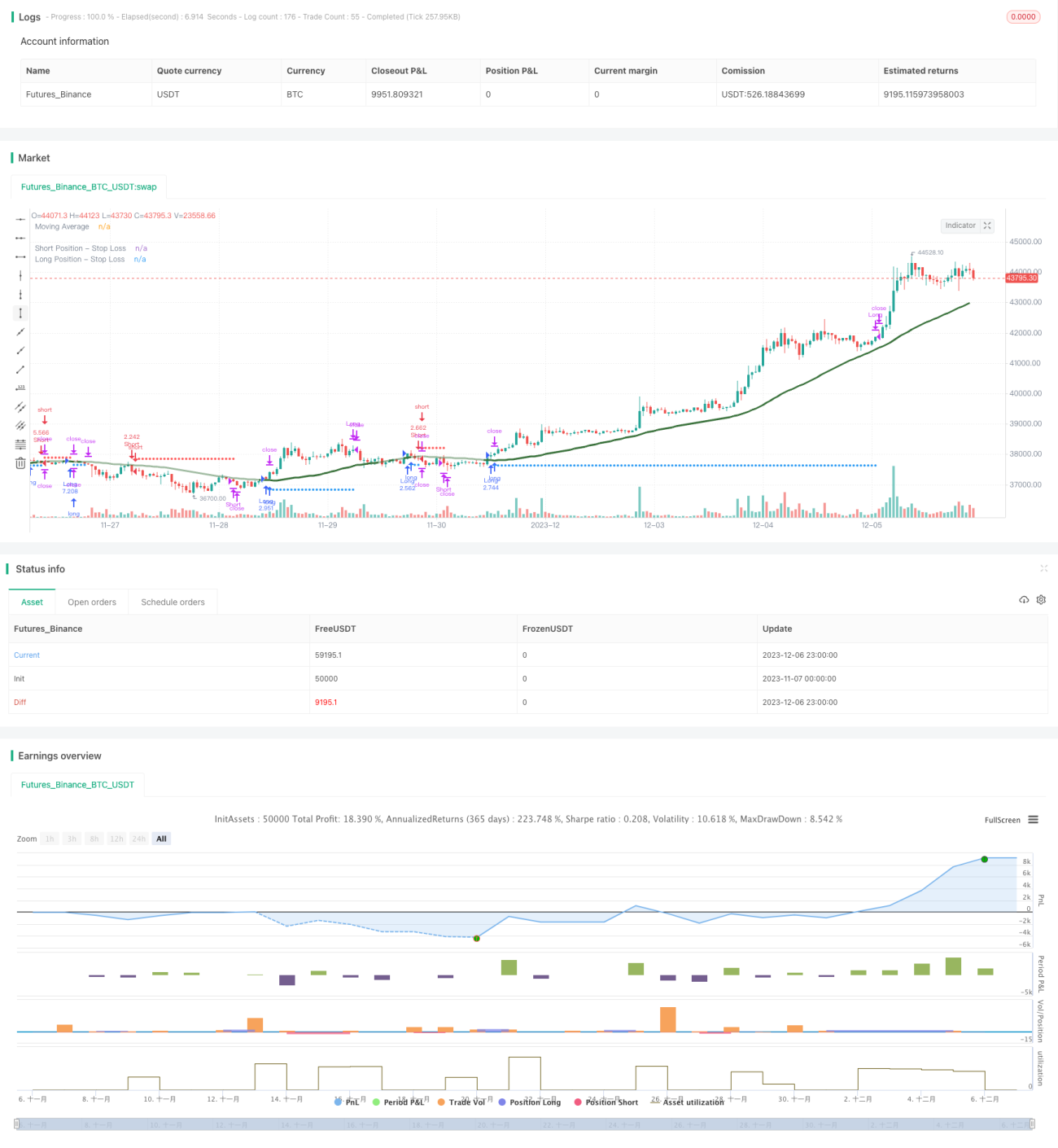

Estrategia de seguimiento de tendencia basada en kNN

Resumen

Esta estrategia utiliza el algoritmo de aprendizaje automático de k vecinos más cercanos (kNN) para predecir la tendencia del mercado y generar señales de posiciones largas y cortas según los resultados de la predicción. La estrategia considera múltiples factores como datos históricos e indicadores técnicos, entrenando dinámicamente el modelo kNN para capturar las características del mercado, logrando un trading de seguimiento de tendencia automatizado.

Principio de la estrategia

-

Recopilación de datos de entrenamiento: se recopilan series temporales como precios de cierre históricos, volúmenes de negociación, así como indicadores técnicos como RSI y CCI.

-

Preprocesamiento de datos: se normalizan los valores de los indicadores al rango 0-100.

-

Entrenamiento del modelo kNN: se ingresan las dos características actuales en el modelo kNN, se calcula la distancia euclidiana entre estos vectores de características y los vectores de características históricos, se seleccionan las k muestras históricas más cercanas y se analiza la distribución de las etiquetas (alcista o bajista) de esas k muestras.

-

Obtención de la predicción: se predice la tendencia actual del mercado según las etiquetas de las k muestras vecinas más cercanas. Si se predice una tendencia alcista, se genera una señal larga; si se predice una tendencia bajista, se genera una señal corta.

-

Combinación con filtros como stop loss, control de posición, media móvil, etc., para realizar las operaciones.

Ventajas de la estrategia

-

Utiliza un algoritmo de aprendizaje automático para identificar patrones técnicos automáticamente, sin intervención manual.

-

Permite seleccionar de manera flexible diferentes indicadores técnicos como características del modelo, optimizando la estrategia en tiempo real.

-

Integra mecanismos estrictos de control de riesgos como stop loss y gestión de posición.

-

Visualiza la línea de stop loss de forma clara e intuitiva.

Riesgos y soluciones

-

Las predicciones del aprendizaje automático pueden generar falsas alarmas. Se puede optimizar el modelo seleccionando un valor k adecuado, vectores de características y rango temporal de las muestras.

-

Existe un riesgo potencial en operaciones unidireccionales. Se puede agregar permiso para operaciones bidireccionales en el código para eliminar errores.

-

Una configuración inadecuada de parámetros puede provocar un exceso de operaciones. Se deben ajustar adecuadamente el tamaño de la posición, la frecuencia de las operaciones y otros parámetros.

Direcciones de optimización

-

Probar diferentes tipos de indicadores técnicos como características de entrada del kNN.

-

Probar otros métodos de medición de distancia, como la distancia de Manhattan.

-

Ajustar el tamaño de la posición según la distancia de las muestras o la calidad de la clasificación.

-

Agregar división del conjunto de entrenamiento y prueba del modelo para lograr una optimización continua.

Resumen

Esta estrategia utiliza el clásico algoritmo kNN para predecir la tendencia del mercado y realiza un trading de seguimiento de tendencia según las señales de predicción. La estrategia tiene las características de parámetros ajustables y riesgo controlable, proporcionando a los usuarios una solución de trading automatizada efectiva. Los usuarios pueden mejorar continuamente el rendimiento de la estrategia ajustando la combinación de indicadores técnicos, optimizando los hiperparámetros del modelo, etc.

- 1