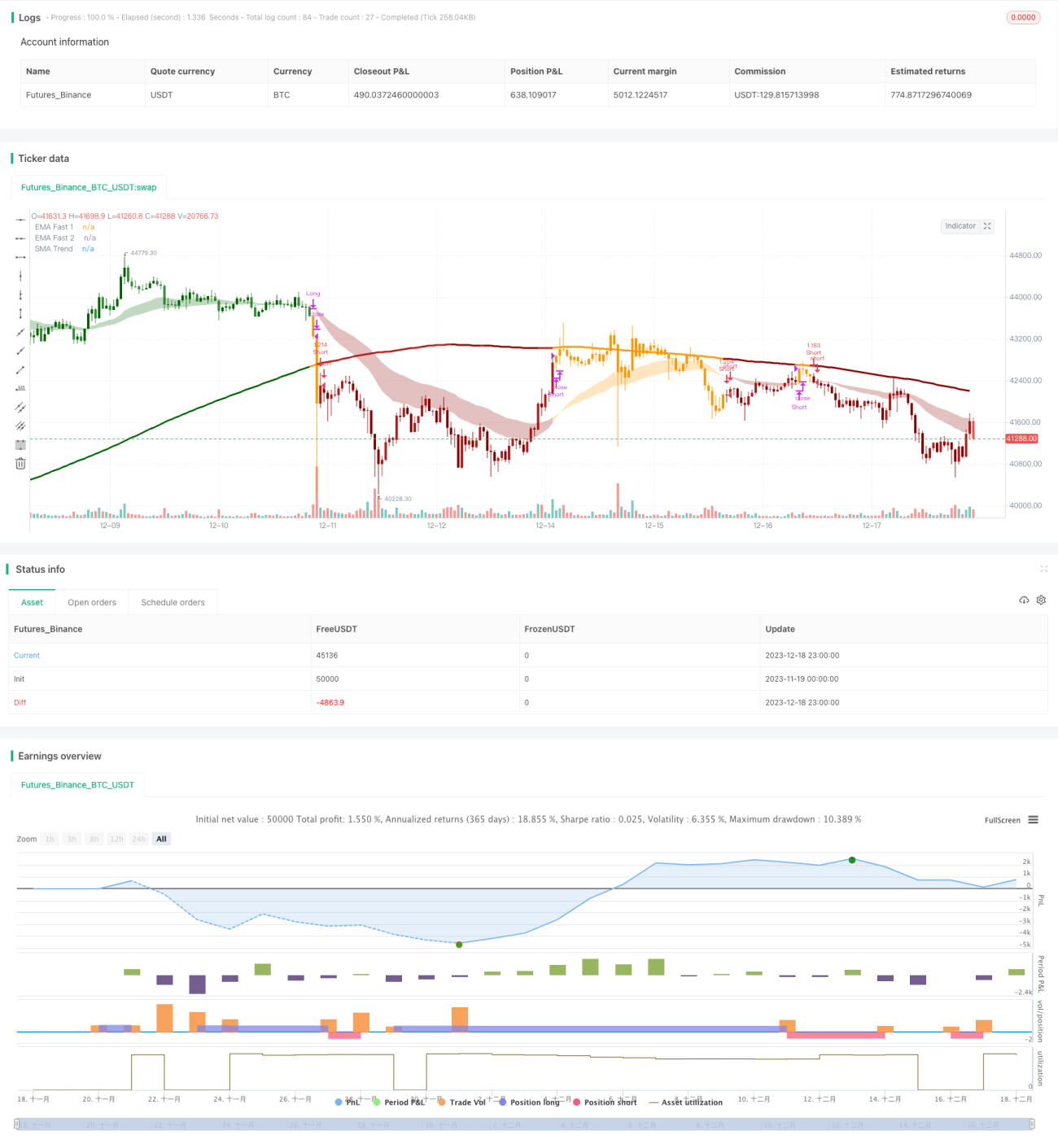

Estrategia de trading cuantitativo híbrida de doble indicador

Resumen

Esta estrategia identifica la dirección de la tendencia y genera operaciones combinando dos indicadores. Primero, utiliza el cruce de dos medias móviles (línea rápida y línea media) para determinar la tendencia a corto plazo; segundo, emplea un rango de canal y una media móvil de largo plazo para determinar la dirección principal de la tendencia. Solo cuando ambas evaluaciones coinciden se genera una señal de trading. Esta combinación de múltiples indicadores filtra eficazmente las señales falsas y mejora la estabilidad.

Principio de la estrategia

La estrategia utiliza tres grupos de indicadores para el análisis. Primero, el cruce dorado (alcista) o cruce de la muerte (bajista) entre la EMA rápida (período 26) y la EMA media (período 50) determina la tendencia a corto plazo. Segundo, se calcula un rango de canal; si el precio supera dicho rango, se determina la dirección alcista o bajista a medio plazo. Por último, se compara la SMA de largo plazo (período 200) con el precio para determinar la tendencia principal. Solo cuando los tres juicios coinciden completamente se emite una señal de trading.

En concreto, la lógica de juicio es:

-

El cruce de la línea rápida y la línea media (cruce dorado = alcista, cruce de la muerte = bajista) indica la tendencia a corto plazo.

-

La ruptura del precio por encima o por debajo del rango del canal indica la tendencia a medio plazo. El rango del canal se basa en la media móvil de largo plazo más/menos el ATR multiplicado por un coeficiente. Si el precio supera el límite superior, es alcista; si cae por debajo del límite inferior, es bajista.

-

La comparación entre el precio y la media móvil de largo plazo determina la tendencia principal.

Finalmente, solo cuando los tres juicios (corto, medio y largo plazo) son consistentes se genera una señal de trading. Este enfoque combinado filtra eficazmente las señales falsas y mejora la estabilidad.

Ventajas de la estrategia

Esta estrategia híbrida de doble indicador ofrece varias ventajas:

-

Filtra eficazmente las señales falsas y mejora la estabilidad, ya que las señales requieren la validación de múltiples indicadores a corto, medio y largo plazo, evitando así errores derivados de un solo indicador.

-

Alta flexibilidad: los parámetros de las medias móviles rápidas/lentas y del rango del canal se pueden ajustar para adaptarse a diferentes entornos de mercado.

-

Combina trading de tendencia y trading de rango. Los indicadores a corto y medio plazo capturan la tendencia, mientras que el indicador a largo plazo define el rango, logrando un equilibrio entre estrategias de tendencia y de reversión.

-

Alta eficiencia en el uso del capital: solo se operan cuando múltiples indicadores coinciden, lo que evita operaciones innecesarias.

Riesgos de la estrategia

La estrategia también presenta algunos riesgos:

-

Riesgo de configuración de parámetros: los períodos de las medias móviles y los parámetros del rango del canal deben ajustarse adecuadamente; de lo contrario, podrían no detectar tendencias o generar demasiadas señales falsas.

-

El doble indicador aumenta el coste de oportunidad: en comparación con estrategias de un solo indicador, podría perder algunas oportunidades de trading y no lograr entrar o salir en los puntos óptimos.

-

La estrategia de stop loss requiere precaución: el mecanismo de stop loss por ruptura en esta estrategia podría generar pérdidas innecesarias; el porcentaje de stop loss debe configurarse con cuidado.

-

Puede tener un rendimiento deficiente en mercados muy laterales o de alta volatilidad. Esta estrategia funciona mejor en mercados con tendencia clara.

Direcciones de optimización

La estrategia se puede optimizar en los siguientes aspectos:

-

Probar diferentes combinaciones de parámetros para encontrar los valores óptimos, mediante backtesting con más datos históricos.

-

Añadir un mecanismo de stop loss adaptativo, ajustando dinámicamente el tamaño del stop loss en función de indicadores de volatilidad.

-

Incorporar indicadores de volumen como apoyo para evaluar el tamaño de la posición en puntos clave y mejorar la eficiencia del uso del capital.

-

Optimizar la lógica de entrada, considerando estrategias de coste promedio (DCA) para reducir el riesgo de una sola entrada.

-

Combinar modelos de machine learning, como redes neuronales, para evaluar la robustez y el ajuste del modelo.

Resumen

Esta estrategia, mediante la triple evaluación (corto, medio y largo plazo) y el mecanismo de doble verificación, suprime eficazmente las señales falsas y mejora la estabilidad. Al mismo tiempo, combina las ventajas del trading de tendencia y del trading de rango, con un uso eficiente del capital. Puede mejorarse mediante optimización de parámetros, ajuste de stop loss, incorporación de indicadores de volumen y otras técnicas, lo que la convierte en una estrategia cuantitativa híbrida recomendable.

- 1