Estrategia de seguimiento de tendencia basada en el Rango Verdadero Promedio

Resumen

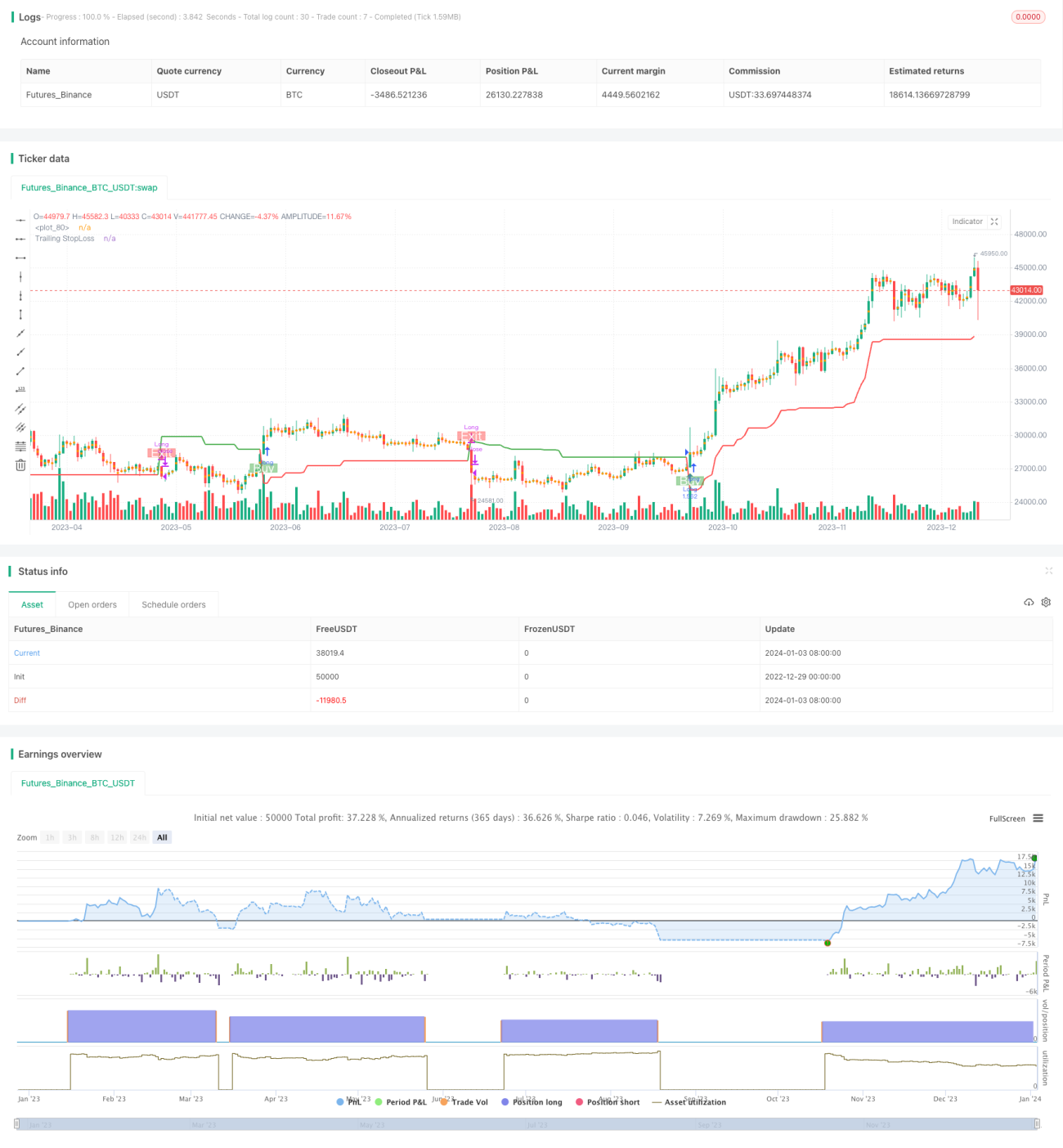

Esta estrategia es una estrategia de seguimiento de tendencia basada en el Average True Range (ATR). Utiliza el ATR para calcular valores indicadores y así determinar la dirección de la tendencia del precio. La estrategia también proporciona un mecanismo de stop loss para controlar el riesgo.

Principio de la estrategia

La estrategia utiliza tres parámetros principales: Período, Multiplicador y Punto de Entrada/Salida. Los parámetros predeterminados son un período de ATR de 14 y un multiplicador de 4.

La estrategia primero calcula el precio promedio de compra (buyavg) y el precio promedio de venta (sellavg), luego compara el precio con estos dos promedios para determinar la dirección actual de la tendencia. Si el precio está por encima del promedio de venta, se considera alcista; si el precio está por debajo del promedio de compra, se considera bajista.

Además, la estrategia combina el ATR para establecer un trailing stop loss. El método específico es: utiliza la media móvil ponderada de 14 períodos del ATR multiplicada por un multiplicador (por defecto 4) como distancia del stop loss. De esta manera, la distancia del stop loss se ajusta según la volatilidad del mercado.

Cuando se activa el stop loss, la estrategia cierra la posición para obtener ganancias.

Ventajas de la estrategia

- Basada en la determinación de tendencias, permite seguir la tendencia y obtener ganancias continuas.

- El uso del ATR para ajustar dinámicamente la distancia del stop loss controla efectivamente el riesgo.

- El cálculo de los puntos de compra y venta es simple y directo, fácil de entender e implementar.

Riesgos y contramedidas

- Cuando la tendencia cambia, pueden ocurrir pérdidas significativas.

- Ajustar adecuadamente el período del ATR y el multiplicador para optimizar la distancia del stop loss.

- En mercados laterales, se generarán múltiples pérdidas pequeñas.

- Agregar condiciones de filtro para evitar mercados laterales.

- Una configuración inadecuada de parámetros puede empeorar el rendimiento de la estrategia.

- Realizar pruebas de optimización con múltiples combinaciones de parámetros para encontrar los mejores.

Direcciones de optimización de la estrategia

- Incorporar otros indicadores para filtrar señales y evitar entradas y salidas en mercados laterales.

- Optimizar los parámetros de período y multiplicador del ATR para que la distancia del stop loss sea más razonable.

- Agregar control del tamaño de la posición de apertura, ajustando el tamaño según las condiciones del mercado.

Resumen

En general, esta estrategia es una estrategia de seguimiento de tendencia simple y práctica. Solo requiere unos pocos parámetros para implementarse. Al ajustar dinámicamente el stop loss mediante el ATR, puede controlar efectivamente el riesgo. Si se combina con otros indicadores auxiliares de juicio, se puede optimizar aún más filtrando algunas señales de ruido. En resumen, esta estrategia es adecuada para quienes desean aprender estrategias de seguimiento de tendencia, y también puede usarse como componente básico para estrategias más avanzadas.

/*backtest

start: 2022-12-29 00:00:00

end: 2024-01-04 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Trend Strategy by zdmre', shorttitle='Trend Strategy', overlay=true, pyramiding=0, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=10000, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.005)

show_STOPLOSSprice = input(true, title='Show TrailingSTOP Prices')

src = input(close, title='Source')- 1