Estrategia del indicador Mofi a través del tiempo

Resumen

Se trata de una estrategia de trading cuantitativo simple que utiliza el indicador MoFi para identificar "grandes tiburones" en el mercado. Está diseñada para un marco temporal de 5 minutos, principalmente para el trading de criptomonedas.

Principio de la Estrategia

La estrategia utiliza el indicador MoFi con una longitud de 3, estableciendo la línea de sobrecompra en 100 y la línea de sobreventa en 0. La estrategia espera a que el indicador MoFi alcance el nivel de sobrecompra, indicando la presencia de un "gran tiburón" en el mercado. Si los dos primeros puntos de sobrecompra del MoFi del día se mantienen y el precio aún puede mantener una tendencia alcista, entonces es una señal de entrada larga.

Cuando el indicador MoFi = 100 y la siguiente vela es una vela larga alcista, se abre una posición larga. El stop loss se establece en el mínimo del día de trading, y el take profit se ejecuta dentro de los 60 minutos posteriores a la entrada.

Para las posiciones cortas, se puede utilizar la lógica espejo. Es decir, cuando el indicador MoFi alcanza la sobreventa y la siguiente vela es una vela larga bajista, se abre una posición corta.

Ventajas de la Estrategia

-

El uso del indicador MoFi puede identificar eficazmente el comportamiento de acumulación de acciones potenciales por parte de los "grandes tiburones" en el mercado, las cuales tienen probabilidad de seguir subiendo.

-

Utilizar el cuerpo real de las velas para identificar puntos de ruptura con fuerza suficiente puede filtrar muchas rupturas falsas.

-

La combinación con un filtro SMA evita comprar acciones en tendencia bajista, reduciendo efectivamente el riesgo de trading.

-

Utilizando un método de trading intradía de corto plazo, el take profit en 60 minutos permite asegurar ganancias rápidamente, reduciendo la probabilidad de retrocesos.

Riesgos de la Estrategia

-

El indicador MoFi puede generar señales falsas, resultando en pérdidas innecesarias. Se pueden ajustar los parámetros adecuadamente o añadir otros indicadores para filtrar.

-

El método de trading de corto plazo de 60 minutos puede ser demasiado agresivo, no adecuado para acciones de alta volatilidad. Se puede ajustar el tiempo de take profit o utilizar un stop loss móvil para optimizar.

-

No se considera el riesgo de impacto del mercado causado por eventos macroeconómicos importantes. En ese caso, se debe pausar la estrategia y reanudar el trading una vez que el mercado se estabilice.

Direcciones de Optimización de la Estrategia

-

Se pueden probar diferentes combinaciones de parámetros, como ajustar la longitud del indicador MoFi u optimizar el período del SMA.

-

Intentar añadir otros indicadores para combinarlos, como las Bandas de Bollinger o el indicador KD, para ver si se puede mejorar la precisión de las señales.

-

Probar si relajar el rango de stop loss permite obtener mayores ganancias por operación individual.

-

Intentar desarrollar versiones para otros marcos temporales basadas en este marco de estrategia, como versiones de 15 o 30 minutos.

Conclusión

En general, esta estrategia es muy simple y fácil de entender. Su idea básica es consistente con el enfoque clásico de seguir a los "grandes tiburones". Al identificar los puntos clave de sobrecompra y sobreventa del indicador MoFi, combinados con el filtrado del cuerpo real de las velas, se puede eliminar mucho ruido. La adición del filtro SMA también mejora la estabilidad de la estrategia.

El método de trading de corto plazo de 60 minutos permite obtener ganancias rápidas, pero también conlleva un mayor riesgo operativo. En general, es una plantilla de estrategia cuantitativa de gran valor práctico, que merece una investigación y optimización más profundas, y nos proporciona valiosas ideas para el desarrollo de estrategias.

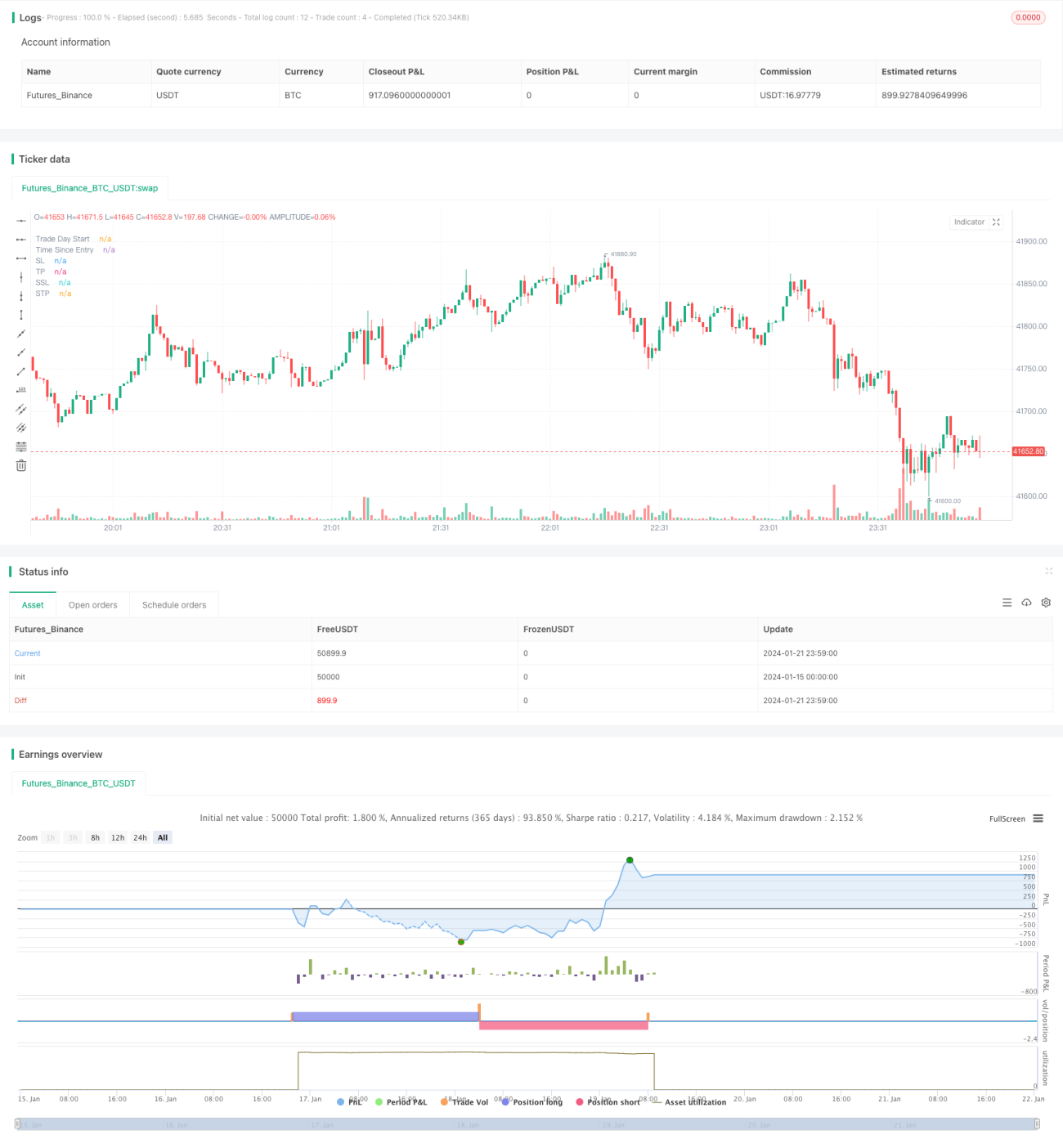

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1