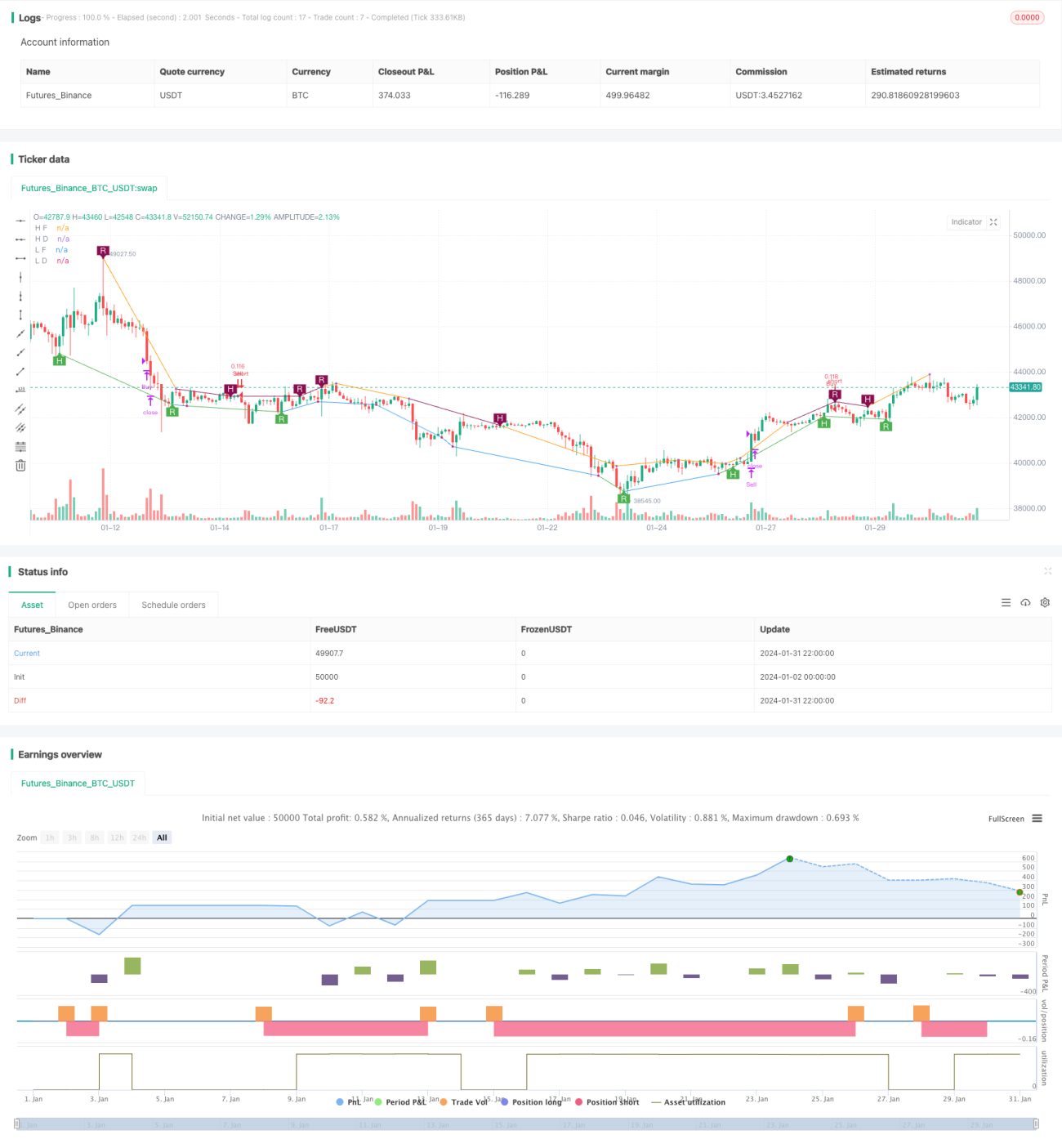

Estrategia de trading de tendencia basada en divergencia de precios

Resumen

Esta estrategia es una estrategia de trading de tendencia basada en señales de divergencia de precios. Utiliza múltiples indicadores para detectar señales de divergencia de precios, como RSI, MACD, Stochastics, etc., y las confirma mediante el oscilador Murrey Math. Cuando aparece una señal de divergencia de precios y el oscilador también confirma la dirección de la tendencia actual, se realiza la entrada.

Principio de la estrategia

El núcleo de la estrategia es la teoría de la divergencia de precios. Cuando el precio alcanza un nuevo máximo pero el indicador no lo hace, se denomina divergencia bajista; cuando el precio alcanza un nuevo mínimo pero el indicador no lo hace, se denomina divergencia alcista. Esto indica una posible reversión de la tendencia. La estrategia combina patrones de picos y valles con el oscilador para confirmar las señales de trading.

Específicamente, las condiciones de entrada de la estrategia son:

- Se detecta una señal de divergencia de precios, incluida divergencia regular y divergencia oculta.

- El oscilador Murrey Math se encuentra en la zona de tendencia correspondiente.

La condición de salida es cerrar la posición cuando el oscilador cruza de nuevo la línea media.

Análisis de ventajas

Esta estrategia combina la teoría de la divergencia de precios y la confirmación de tendencia, ofreciendo las siguientes ventajas:

- Utiliza señales de divergencia de precios para detectar posibles puntos de reversión de tendencia.

- Aplica un oscilador para confirmar la tendencia actual, evitando falsas rupturas.

- Múltiples indicadores y combinaciones de parámetros que se pueden ajustar de forma flexible.

- Equilibra el seguimiento de tendencia y la prevención de pérdidas.

- Reglas lógicas claras y amplio margen de optimización del código.

Análisis de riesgos

Los principales riesgos provienen de los siguientes aspectos:

- Las señales de divergencia de precios pueden ser falsas y no confirmar completamente la reversión de la tendencia.

- Una configuración inadecuada de los parámetros del oscilador puede provocar la omisión de oportunidades de trading.

- Una sobreexposición en posiciones largas o cortas puede generar un alto riesgo de pérdidas.

- Durante períodos de alta volatilidad, puede aumentar el número de operaciones y los costos de deslizamiento.

Se recomienda establecer stop loss, ajustar el tamaño de las posiciones y optimizar las combinaciones de parámetros para reducir el riesgo.

Direcciones de optimización

Esta estrategia aún tiene margen para una mayor optimización:

- Agregar algoritmos de aprendizaje automático para optimizar las combinaciones de parámetros en tiempo real.

- Incorporar técnicas de stop loss adaptativas, como stop loss dinámico o stop loss promedio.

- Combinar más indicadores y filtros para mejorar la relación señal/ruido.

- Ajustar dinámicamente los parámetros del oscilador para optimizar la identificación de tendencias.

- Optimizar la gestión de riesgos estableciendo límites como la reducción máxima.

Resumen

Esta estrategia integra la teoría de la divergencia de precios y los indicadores de análisis de tendencia, lo que permite detectar de manera efectiva posibles puntos de cambio de tendencia. Combinada con medidas optimizadas de gestión de riesgos, puede lograr un buen rendimiento estratégico. En el futuro, se puede optimizar mediante métodos avanzados como el aprendizaje automático para obtener un alfa más estable.

- 1