Stratégie de suivi de tendance par breakout de momentum

Aperçu

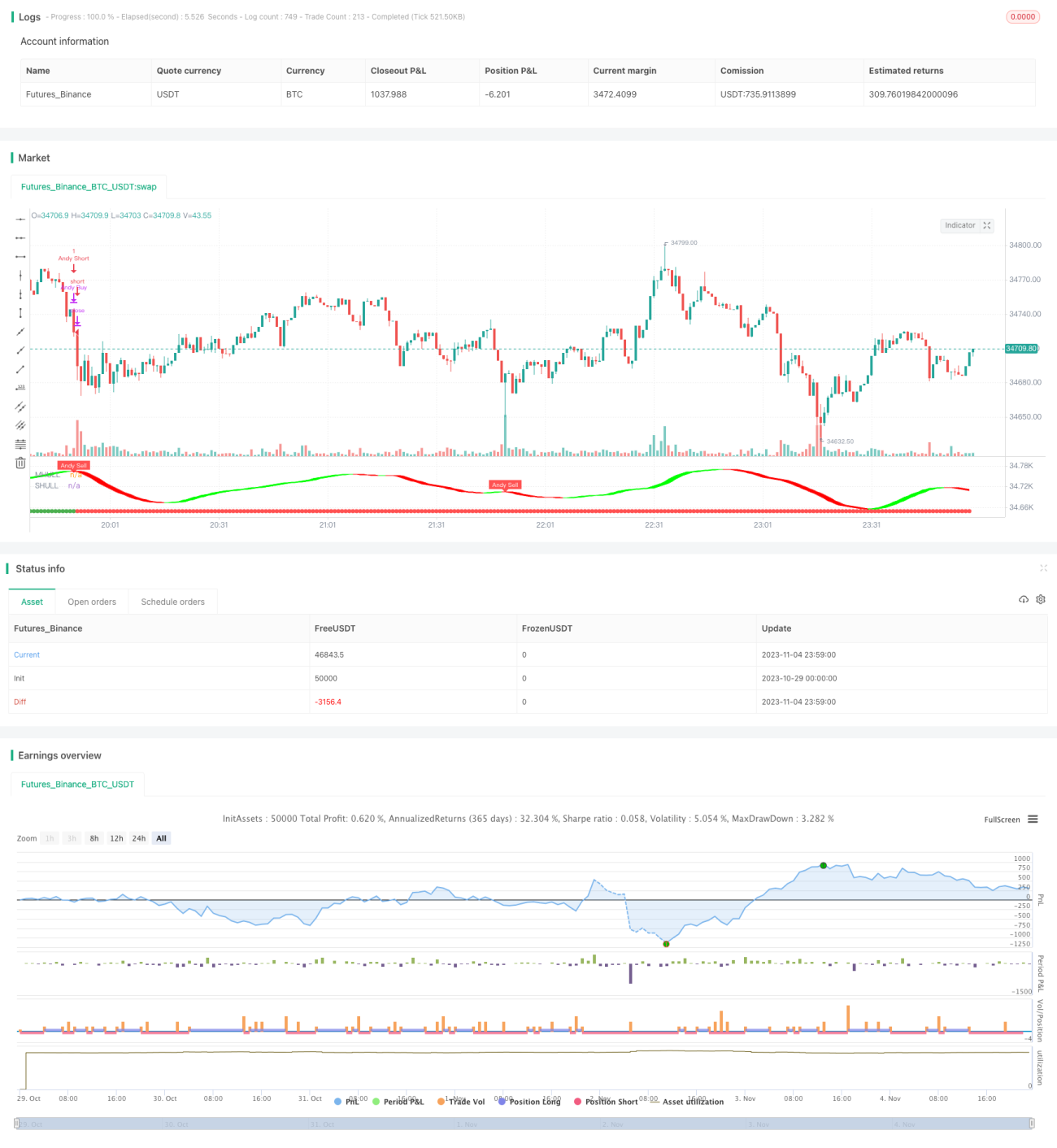

Cette stratégie combine plusieurs indicateurs techniques pour identifier la direction de la tendance et suit les percées de momentum afin de générer des rendements excédentaires.

Principes de la stratégie

-

Utilisation du canal de Donchian pour déterminer la direction générale de la tendance. Lorsque le prix franchit ce canal, un changement de tendance est confirmé.

-

La moyenne mobile de Hull aide à confirmer la direction de la tendance. Cet indicateur est sensible aux variations de prix et peut détecter les retournements de tendance plus tôt.

-

Le système de demi-orbite émet des signaux d'achat et de vente. Basé sur des canaux de prix et l'ATR, il permet d'éviter les fausses percées.

-

Lorsque le canal de Donchian, l'indicateur de Hull et le système de demi-orbite envoient simultanément un signal, une percée de momentum puissante est confirmée et l'entrée en position est effectuée.

-

Condition de sortie : lorsque les indicateurs ci-dessus signalent un renversement, la position est immédiatement fermée avec un stop-loss.

Avantages

-

Combinaison de multiples indicateurs pour une meilleure fiabilité. Le canal de Donchian détermine la tendance générale, tandis que la moyenne mobile de Hull et le système de demi-orbite en précisent les points de retournement.

-

Participation aux percées de momentum pour rechercher des rendements excédentaires. L'entrée n'a lieu que lors d'une forte percée de tendance, évitant d'être piégé dans des phases de consolidation.

-

Stop-loss strict pour protéger le capital. Dès qu'un signal inverse est émis, la position est fermée, limitant les pertes.

-

Paramètres flexibles adaptés à tous les marchés. La longueur du canal, les plages de volatilité, etc., peuvent être ajustés pour différents horizons temporels.

-

Facile à comprendre et à implémenter, même pour les débutants. Les indicateurs et les conditions sont simples et clairs, faciles à coder.

Analyse des risques

-

Opportunités manquées en début de tendance. L'entrée tardive ne capte pas les premiers gains.

-

Pertes en cas d'échec de la percée. Une percée peut échouer et s'inverser, entraînant des pertes.

-

Signaux erronés des indicateurs. Un mauvais réglage des paramètres peut provoquer des erreurs de jugement.

-

Nombre limité de transactions. L'entrée n'a lieu que lors de percées claires, ce qui limite le nombre annuel de trades.

Pistes d'optimisation

-

Optimiser les combinaisons de paramètres. Tester différents paramètres pour trouver la combinaison optimale.

-

Ajouter une condition de retrait progressif pour le stop-loss. Éviter des stop-loss trop précoces qui feraient manquer la tendance.

-

Intégrer d'autres indicateurs de filtrage (MACD, KDJ, etc.) pour réduire les signaux erronés.

-

Optimiser les plages horaires de trading. Ajuster les paramètres selon les différentes périodes.

-

Améliorer l'efficacité de l'utilisation du capital. Utiliser l'effet de levier, l'investissement programmé, etc.

Conclusion

Cette stratégie combine plusieurs indicateurs pour détecter les percées de momentum dans une tendance, et suit la tendance établie afin de réaliser des rendements excédentaires. Un stop-loss strict gère les risques, et des paramètres flexibles s'adaptent à différents environnements de marché. Bien que la fréquence des transactions soit faible, chaque trade vise un rendement élevé. Grâce à l'optimisation des paramètres et à l'ajout d'indicateurs auxiliaires, la stratégie peut être continuellement améliorée.

- 1