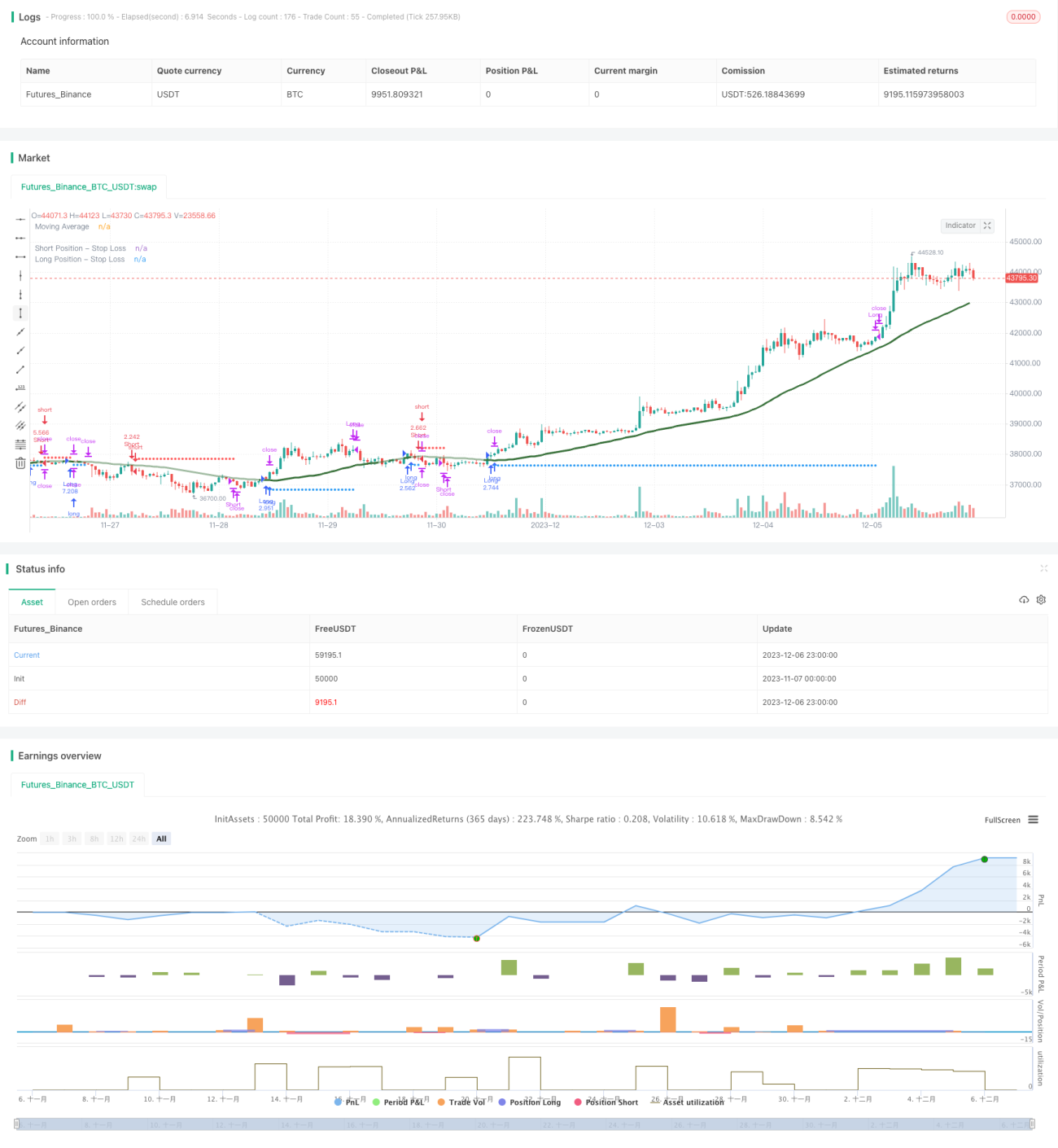

Stratégie de suivi de tendance basée sur le kNN

Aperçu

Cette stratégie utilise l'algorithme d'apprentissage automatique des k plus proches voisins (kNN) pour prédire les tendances du marché et génère des signaux de position longue et courte en fonction des prédictions. Elle prend en compte plusieurs facteurs tels que les données historiques et les indicateurs techniques, et entraîne dynamiquement le modèle kNN pour saisir les caractéristiques du marché, permettant ainsi un trading de suivi de tendance automatisé.

Principe de la stratégie

-

Collecte des données d'apprentissage : collecte de séries temporelles telles que les prix de clôture historiques et les volumes de transactions, ainsi que des indicateurs techniques comme le RSI et le CCI.

-

Prétraitement des données : normalisation des valeurs des indicateurs dans l'intervalle 0-100.

-

Entraînement du modèle kNN : saisie des deux caractéristiques dans le modèle kNN actuel, calcul de la distance euclidienne entre ces vecteurs de caractéristiques et les vecteurs historiques, sélection des k échantillons historiques les plus proches, puis décompte de la distribution des étiquettes (longue ou courte) de ces k échantillons.

-

Obtention des prédictions : prédiction de la tendance actuelle du marché en fonction des étiquettes des k plus proches voisins. Si la prédiction est longue, un signal de position longue est généré ; si elle est courte, un signal de position courte est émis.

-

Combinaison avec des filtres de trading tels que le stop-loss, le contrôle de position et les moyennes mobiles.

Avantages de la stratégie

-

Utilisation de l'algorithme d'apprentissage automatique pour identifier automatiquement les figures techniques, sans intervention humaine.

-

Possibilité de sélectionner librement différents indicateurs techniques comme caractéristiques du modèle pour optimiser la stratégie en temps réel.

-

Intégration de mécanismes stricts de gestion des risques, tels que le stop-loss et la gestion de position.

-

Visualisation claire et intuitive de la ligne de stop-loss.

Risques et solutions

-

Les prédictions de l'apprentissage automatique peuvent être faussement positives. On peut optimiser le modèle en choisissant une valeur k appropriée, des vecteurs de caractéristiques, une plage temporelle d'échantillons, etc.

-

Le trading unidirectionnel comporte des risques potentiels. On peut autoriser le trading bilatéral dans le code pour éliminer les bugs.

-

Un réglage inapproprié des paramètres peut entraîner un sur-transaction. Il convient d'ajuster correctement la taille des positions et la fréquence des transactions.

Directions d'optimisation

-

Tester différents types d'indicateurs techniques comme caractéristiques d'entrée du kNN.

-

Essayer d'autres mesures de distance, comme la distance de Manhattan.

-

Ajuster la taille des positions en fonction de la distance des échantillons ou de la qualité de classification.

-

Ajouter une division entre ensemble d'entraînement et ensemble de test du modèle pour une optimisation glissante.

Résumé

Cette stratégie utilise l'algorithme classique kNN pour prédire les tendances du marché et exécute un trading de suivi de tendance en fonction des signaux de prédiction. Elle se caractérise par des paramètres ajustables et des risques contrôlables, offrant aux utilisateurs une solution de trading automatisée efficace. Les utilisateurs peuvent améliorer les performances de la stratégie en ajustant la combinaison d'indicateurs techniques et en optimisant les hyperparamètres du modèle.

- 1