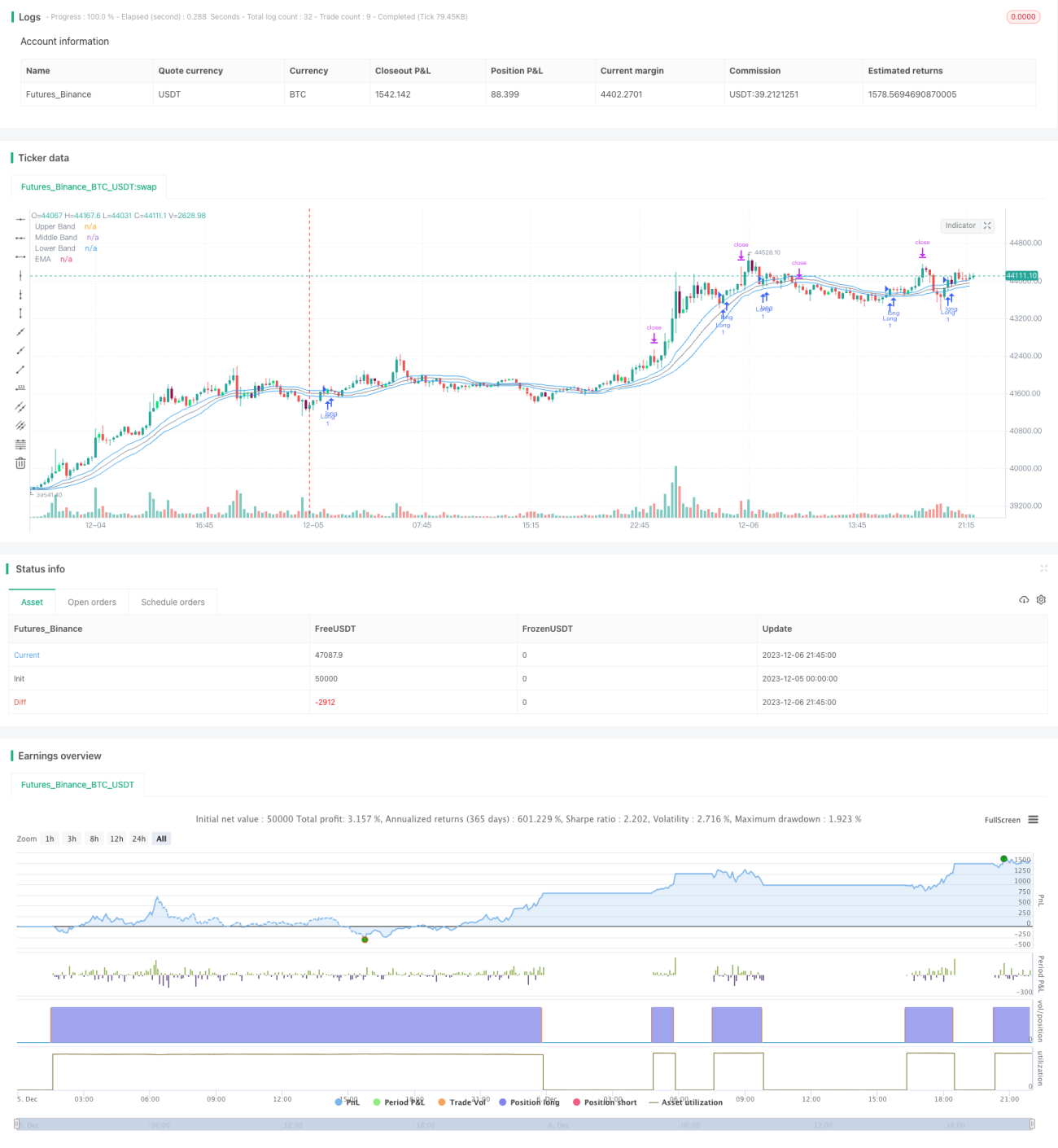

Stratégie de capture à double moyenne exponentielle

Aperçu

Cette stratégie utilise une double moyenne exponentielle pour déterminer la tendance du marché, combinée à l'indicateur des bandes de Bollinger pour identifier les conditions de surachat et de survente, afin d'acheter bas et de vendre haut, puis de prendre ses bénéfices.

Principe de la stratégie

La stratégie utilise la double moyenne exponentielle pour juger la tendance générale du marché et les bandes de Bollinger pour déterminer les points d'entrée précis.

Le fonctionnement de la double moyenne exponentielle est le suivant : on calcule respectivement une moyenne exponentielle courte et une moyenne exponentielle longue. Lorsque la ligne courte franchit la ligne longue par le bas, c'est un signal haussier ; lorsqu'elle la traverse par le haut, c'est un signal baissier.

Les bandes de Bollinger indiquent si le prix est en surachat ou en survente. La bande médiane est la moyenne mobile du cours de clôture sur n jours, et la largeur de bande est l'écart type de la moyenne mobile sur les n jours précédents. Un prix proche de la bande supérieure indique un surachat, proche de la bande inférieure une survente.

Les règles de cette stratégie sont les suivantes :

- Lorsque la moyenne courte franchit la moyenne longue par le bas et que le cours de clôture dépasse la bande supérieure de Bollinger, prendre une position longue.

- Lorsque la moyenne courte traverse la moyenne longue par le haut et que le cours de clôture passe sous la bande inférieure de Bollinger, prendre une position courte.

Le stop-loss pour une position longue est le plus bas des n jours précédents, et le take-profit est 1,6 fois le prix d'ouverture. Pour une position courte, le stop-loss est le plus haut des n jours précédents, et le take-profit est 1,6 fois le prix d'ouverture.

De plus, cette stratégie prend en compte l'indicateur EMA pour évaluer la tendance générale et éviter d'ouvrir des positions à contre-tendance.

Analyse des avantages

- L'utilisation de la double moyenne exponentielle pour la tendance générale et des bandes de Bollinger pour les points d'entrée/sortie est une combinaison judicieuse d'indicateurs.

- Le stop-loss pour les positions longues utilise le plus bas des n jours précédents, et pour les positions courtes, le plus haut des n jours précédents, ce qui réduit le risque de se faire stopper par une poursuite de mouvement.

- Le take-profit fixé à 1,6 fois le prix d'ouverture permet de réaliser un gain suffisant.

- La prise en compte de l'indicateur de tendance EMA aide à éviter les positions à contre-courant et réduit les pertes systématiques.

Analyse des risques

- Un paramétrage inapproprié des bandes de Bollinger peut entraîner une fréquence de transactions trop élevée ou des signaux trop rares.

- Un stop-loss trop large peut aggraver les pertes.

- Un take-profit trop large peut faire manquer des profits plus importants.

Pour atténuer ces risques, il convient d'optimiser les paramètres des bandes de Bollinger, de tester différents niveaux de stop-loss et de take-profit, et de choisir les paramètres optimaux.

Axes d’optimisation

- Optimiser les paramètres des bandes de Bollinger pour trouver la meilleure combinaison.

- Tester différents niveaux de stop-loss afin de réduire la probabilité de se faire stopper.

- Tester différents multiples de take-profit pour maximiser les gains.

Conclusion

Cette stratégie, qui utilise la double moyenne exponentielle pour déterminer la tendance générale et les bandes de Bollinger pour les points d'entrée, a montré de bons résultats lors des backtests. Des améliorations supplémentaires sont possibles grâce à l'optimisation des paramètres et à la modification des règles. Son mécanisme de stop-loss et de take-profit peut également être transposé à d'autres stratégies, offrant ainsi une valeur de référence.

- 1