Stratégie de retournement de tendance idéologique dynamique

Aperçu

La stratégie de retournement de tendance basée sur l'idéologie dynamique utilise la régression linéaire pour prédire le prix, et combine l'idéologie formée par les moyennes mobiles pour générer des signaux de trading. Un signal d'achat est généré lorsque le prix prédit traverse la moyenne mobile de bas en haut ; un signal de vente est généré lorsque le prix prédit traverse la moyenne mobile de haut en bas, permettant ainsi de capturer les retournements de tendance.

Principe de la stratégie

- Calculer la régression linéaire du prix de l'action basée sur le volume de transactions, afin d'obtenir la valeur prédite du prix

- Calculer les moyennes mobiles dans différentes conditions

- Lorsque le prix prédit traverse la moyenne mobile de bas en haut, un signal d'achat est généré

- Lorsque le prix prédit traverse la moyenne mobile de haut en bas, un signal de vente est généré

- Combiner l'indicateur MACD pour déterminer le moment du retournement de tendance

Ces signaux sont combinés avec plusieurs confirmations pour éviter les faux dépassements, améliorant ainsi la précision des signaux.

Analyse des avantages

- Utiliser la régression linéaire pour prédire la tendance des prix, améliorant la précision des signaux

- Combiner l'idéologie formée par les moyennes mobiles pour capturer les retournements de tendance

- Calculer la régression linéaire basée sur le volume, ce qui lui confère une signification économique plus forte

- Combiner des indicateurs tels que le MACD pour une confirmation multiple, réduisant les faux signaux

Analyse des risques

- Les paramètres de la régression linéaire peuvent avoir un impact significatif sur les résultats

- Les réglages des moyennes mobiles affectent également la qualité des signaux

- Malgré le mécanisme de confirmation, le risque de faux signaux persiste

- Le code peut être optimisé davantage pour réduire le nombre de transactions et améliorer le taux de profit

Directions d'optimisation

- Optimiser les paramètres de la régression linéaire et des moyennes mobiles

- Ajouter des conditions de confirmation pour réduire le taux de faux signaux

- Combiner davantage de facteurs pour évaluer la qualité du retournement de tendance

- Optimiser la stratégie de stop-loss pour réduire le risque par transaction

Résumé

La stratégie de retournement de tendance basée sur l'idéologie dynamique intègre la prédiction par régression linéaire et l'idéologie formée par les moyennes mobiles pour capturer les moments de retournement de tendance. Comparée à un indicateur unique, elle offre une fiabilité accrue. De plus, la stratégie peut être améliorée via l'ajustement des paramètres et l'optimisation des conditions de confirmation, renforçant ainsi la qualité des signaux et la rentabilité.

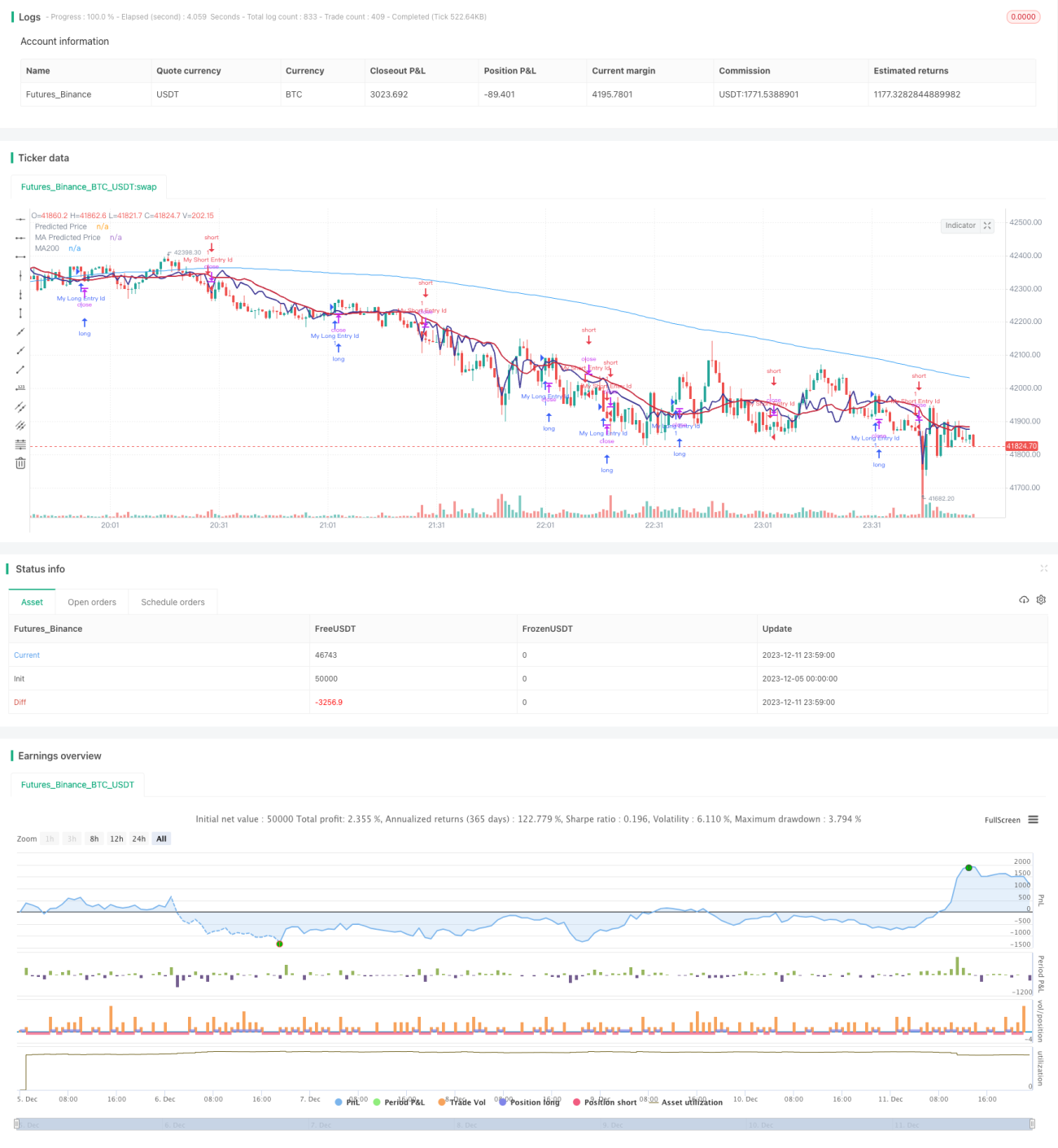

/*backtest

start: 2023-12-05 00:00:00

end: 2023-12-12 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © stocktechbot

//@version=5

strategy("Linear Cross", overlay=true, margin_long=100, margin_short=0)- 1