Stratégie de stop suivi SuperTrend

Aperçu

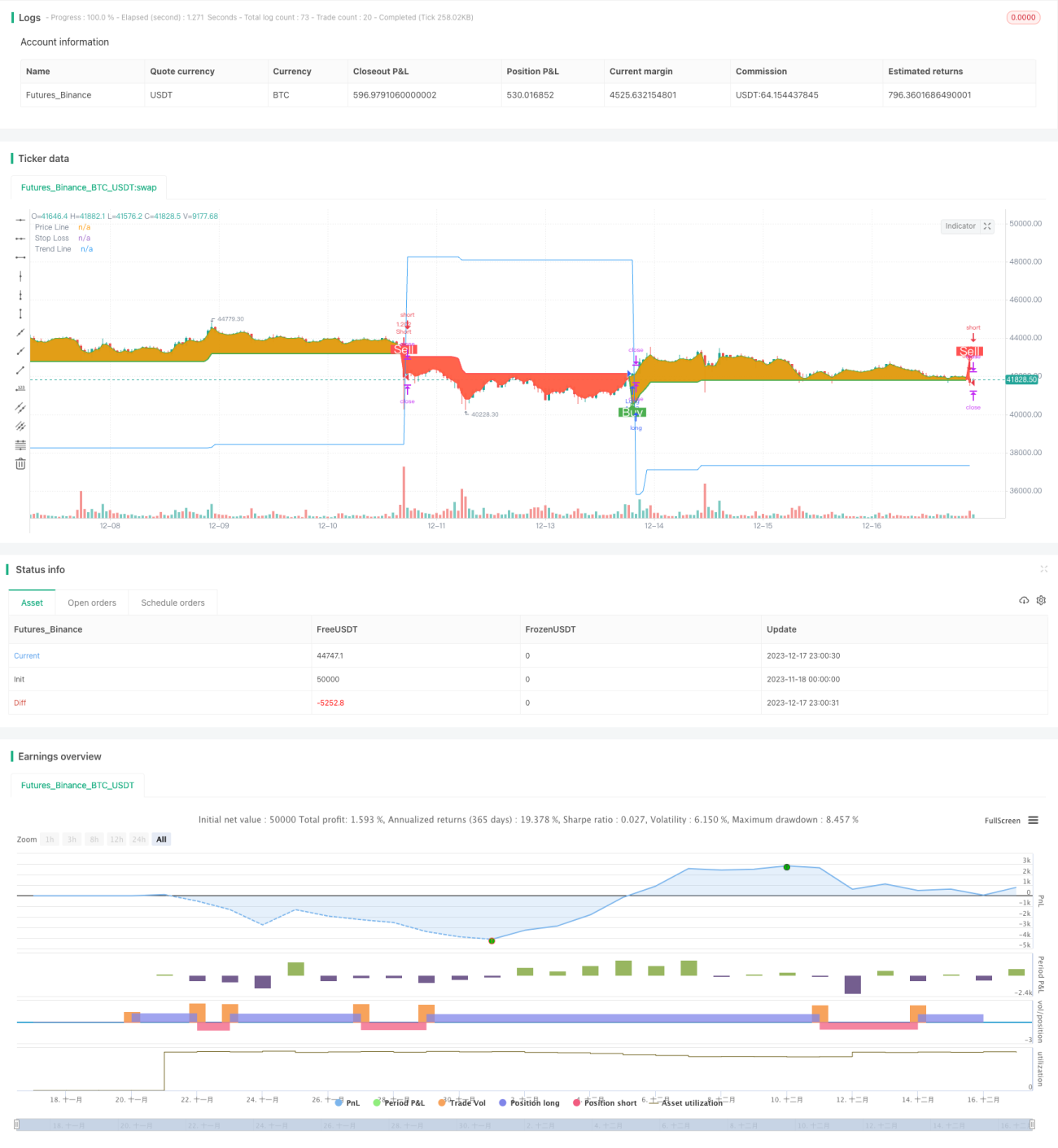

Cette stratégie utilise l'indicateur SuperTrend et un stop suiveur pour ouvrir et fermer des positions. Elle emploie 4 alertes pour ouvrir et fermer les positions, et repose sur une approche basée sur le SuperTrend. La stratégie est spécialement conçue pour les robots de trading et intègre une fonction de stop suiveur.

Principe de la stratégie

La stratégie calcule les bandes haute et basse à l'aide de l'indicateur ATR. Un signal d'achat est généré lorsque le cours de clôture franchit la bande haute, et un signal de vente lorsqu'il franchit la bande basse. La stratégie utilise également la ligne de SuperTrend pour déterminer la direction de la tendance. Lorsque la ligne de SuperTrend passe au-dessus, cela indique le début d'un marché haussier ; lorsqu'elle passe en dessous, cela indique le début d'un marché baissier. La stratégie ouvre une position lors de l'apparition d'un signal, tout en fixant un prix de stop initial. Ensuite, elle ajuste le prix de stop de manière dynamique en fonction des mouvements de prix, afin de verrouiller les profits et d'obtenir un effet de stop suiveur.

Analyse des avantages

Cette stratégie combine les avantages de l'indicateur SuperTrend pour identifier la direction de la tendance et de l'ATR pour définir les stops, ce qui permet de filtrer efficacement les faux dépassements. Le stop suiveur permet de verrouiller les profits et de réduire le drawdown. De plus, la stratégie étant spécialement conçue pour les robots, elle peut être exécutée de manière automatisée.

Analyse des risques

L'indicateur SuperTrend peut générer un nombre important de faux signaux. Si l'amplitude d'ajustement du prix de stop est trop grande, la probabilité que le stop soit touché augmente. Par ailleurs, le trading robotisé est exposé à des risques techniques tels que les pannes de serveur ou les interruptions réseau.

Pour réduire la probabilité de faux signaux, il est possible d'ajuster les paramètres de l'ATR ou d'ajouter d'autres indicateurs comme filtre. Lors du réglage de l'amplitude du stop suiveur, il faut trouver un équilibre entre profit et risque. Il convient également de préparer des serveurs de secours et un réseau pour parer aux risques techniques.

Pistes d'optimisation

La stratégie peut être optimisée dans les domaines suivants :

- Ajouter des indicateurs ou des conditions pour filtrer les signaux d'entrée et éviter les faux signaux. Par exemple, on peut ajouter l'indicateur MACD.

- Tester différentes combinaisons de paramètres ATR pour trouver les meilleurs paramètres.

- Optimiser l'amplitude du stop suiveur pour trouver le point d'équilibre optimal.

- Ajouter plusieurs niveaux de stop pour réaliser un stop progressif.

- Mettre en place une architecture à deux serveurs (principal et de secours) pour basculer rapidement en cas de panne du serveur principal.

Résumé

Cette stratégie intègre les avantages de l'indicateur SuperTrend et du stop suiveur, permettant d'ouvrir et de fermer des positions de manière automatisée. En y appliquant les améliorations proposées dans les pistes d'optimisation, elle peut devenir une stratégie de trading quantitatif très pratique en conditions réelles.

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © arminomid1375

//@version=5

strategy('Mizar_BOT_super trend', overlay=true, default_qty_value=100, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=100, max_bars_back=4000)- 1