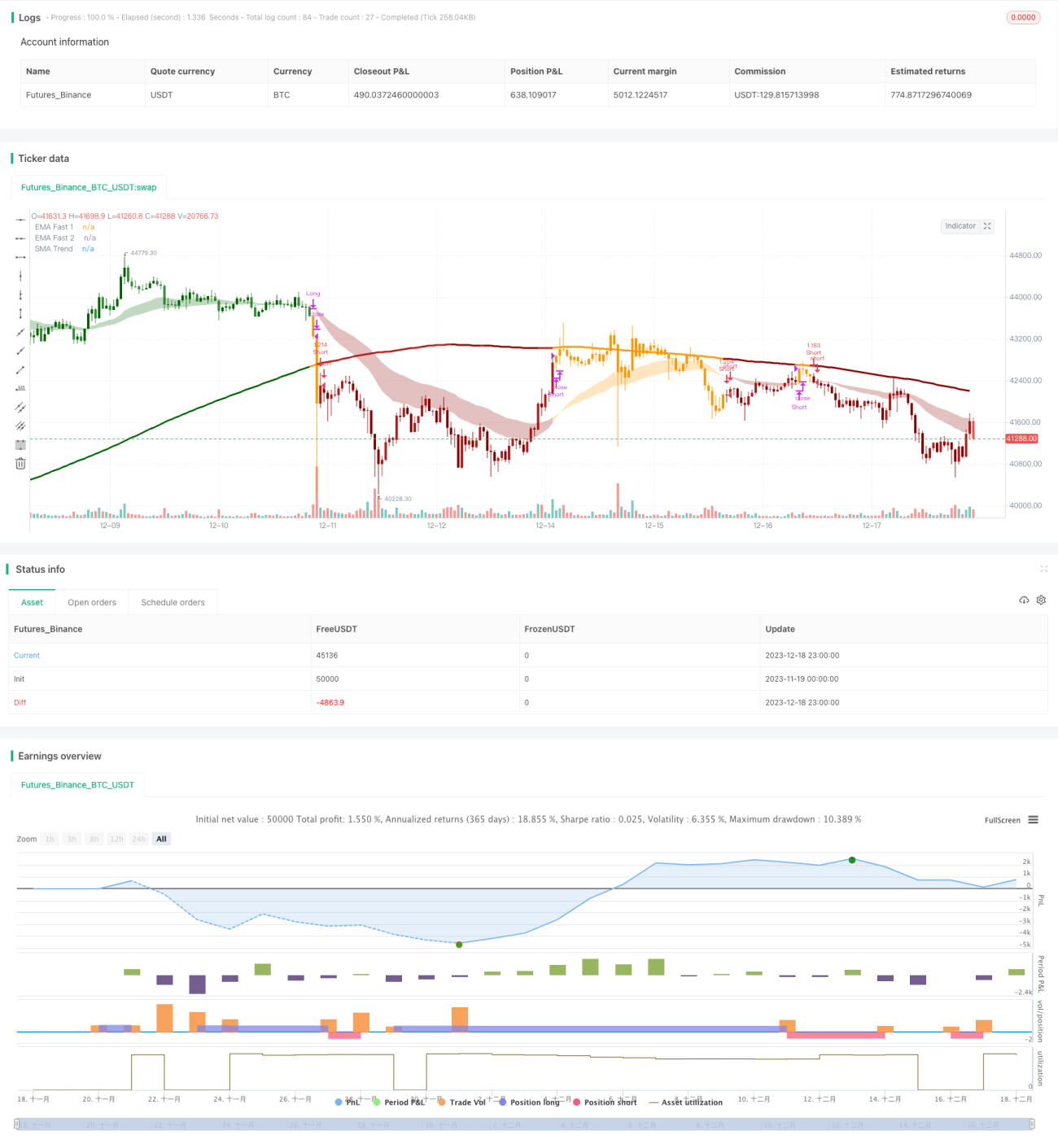

Stratégie de trading quantitatif hybride à double indicateur

Aperçu

Cette stratégie identifie la tendance et génère des transactions en combinant deux indicateurs. D'abord, elle utilise le croisement de deux moyennes mobiles (rapide et intermédiaire) pour déterminer la tendance à court terme. Ensuite, elle utilise une plage de canaux et une moyenne mobile à long terme pour déterminer la tendance principale. Un signal de transaction n'est émis que lorsque les deux jugements concordent. Cette utilisation combinée de multiples indicateurs permet de filtrer efficacement les faux signaux et d'améliorer la stabilité.

Principe de la stratégie

La stratégie s'appuie sur trois groupes d'indicateurs. D'abord, le croisement haussier (golden cross) ou baissier (death cross) entre l'EMA rapide (période 26) et l'EMA intermédiaire (période 50) détermine la tendance à court terme. Ensuite, on calcule une plage de canaux et on vérifie si le prix dépasse cette plage pour déterminer la tendance à moyen terme (haussière ou baissière). Enfin, on compare le prix avec la moyenne mobile simple à long terme (SMA 200) pour déterminer la direction de la tendance principale. Un signal de transaction n'est émis que lorsque les trois jugements sont tous cohérents.

Plus précisément, la logique de jugement est la suivante :

- Le croisement des lignes rapide et intermédiaire (golden cross = haussier, death cross = baissier) détermine la direction de la tendance à court terme.

- La rupture du prix par rapport à la plage de canaux détermine la direction de la tendance à moyen terme. La plage de canaux est basée sur la moyenne mobile à long terme, à laquelle on ajoute ou retranche l'ATR multiplié par un coefficient. Si le prix dépasse la limite supérieure, c'est haussier ; s'il casse la limite inférieure, c'est baissier.

- La comparaison entre le prix et la moyenne mobile à long terme détermine la direction de la tendance principale.

Enfin, un signal de transaction n'est émis que si les trois jugements (court, moyen, long terme) sont tous cohérents. Ce jugement combiné permet de filtrer efficacement les faux signaux et d'améliorer la stabilité.

Avantages de la stratégie

Cette stratégie combinant deux indicateurs présente plusieurs avantages :

- Elle filtre efficacement les faux signaux et améliore la stabilité, car les signaux de transaction nécessitent la validation de multiples indicateurs (court, moyen, long terme), évitant ainsi les erreurs dues à un seul indicateur.

- Elle offre une grande flexibilité, les paramètres des moyennes mobiles rapides et lentes ainsi que ceux de la plage de canaux pouvant être ajustés pour s'adapter à différents environnements de marché.

- Elle combine les avantages du trading de tendance et du trading de range. Les indicateurs à court et moyen termes capturent la tendance, tandis que l'indicateur à long terme détermine la zone, offrant ainsi une approche équilibrée entre suivi de tendance et retournement.

- L'utilisation du capital est efficace. Les ordres ne sont passés que lorsque les résultats des multiples indicateurs sont cohérents, ce qui permet d'utiliser les fonds de manière optimale et d'éviter les transactions inutiles.

Risques de la stratégie

Cette stratégie comporte également certains risques :

- Risque lié au réglage des paramètres. Les périodes des moyennes mobiles et les paramètres de la plage de canaux doivent être définis correctement ; sinon, ils pourraient ne pas détecter efficacement la tendance ou générer trop de faux signaux.

- La combinaison de deux indicateurs augmente le coût d'opportunité des transactions. Par rapport à une stratégie à indicateur unique, elle peut manquer certaines opportunités de trading et ne pas entrer ou sortir aux points optimaux.

- La stratégie de stop-loss doit être utilisée avec prudence. Le mécanisme de stop-loss par cassure de cette stratégie peut entraîner des pertes inutiles ; le pourcentage de stop-loss doit donc être soigneusement défini.

- L'efficacité peut être réduite dans des marchés fortement agités. Cette stratégie est plus adaptée aux environnements de marché où la tendance est claire.

Pistes d'optimisation

La stratégie peut être optimisée dans les directions suivantes :

- Tester différentes combinaisons de paramètres pour trouver les paramètres optimaux. Des tests sur des données historiques plus étendues peuvent permettre de déterminer le réglage le plus performant.

- Ajouter un mécanisme de stop-loss adaptatif. Il est possible d'ajuster dynamiquement l'amplitude du stop-loss en utilisant un indicateur de volatilité.

- Intégrer un indicateur de volume pour aider au jugement. Aux points clés, il peut aider à déterminer la taille des positions, améliorant ainsi l'efficacité de l'utilisation du capital.

- Optimiser la logique d'entrée. Envisager des stratégies de coût moyen par entrées progressives pour réduire le risque lié à une entrée unique.

- Combiner avec des modèles d'apprentissage automatique pour le jugement. Introduire des modèles comme les réseaux de neurones pour évaluer la robustesse et la qualité d'ajustement du modèle.

Résumé

Cette stratégie, grâce à l'évaluation triple (court, moyen, long terme) et à un mécanisme de double validation, permet de supprimer efficacement les faux signaux et d'améliorer la stabilité. Elle combine également les avantages du trading de tendance et du trading de range, avec une utilisation efficace du capital. Elle peut être améliorée par l'optimisation des paramètres, l'optimisation du stop-loss, l'intégration d'indicateurs de volume, etc. C'est une stratégie quantitative hybride recommandable.

- 1