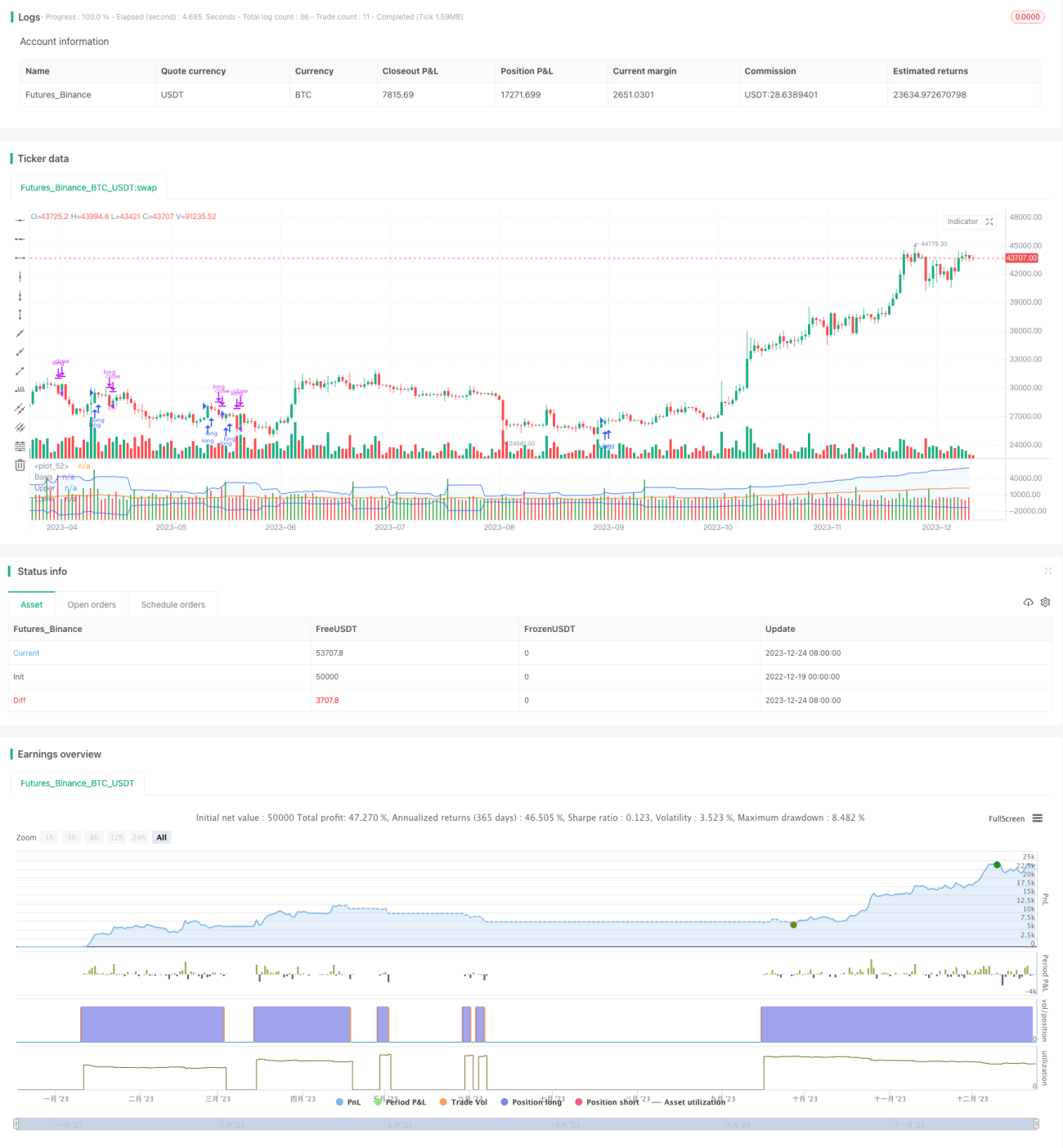

Stratégie de percée dynamique basée sur la volatilité des volumes d'achat et de vente

Aperçu

Cette stratégie utilise les volumes d'achat et de vente sur une période personnalisée pour déterminer les positions longues ou courtes, en les filtrant avec la VWAP hebdomadaire et les bandes de Bollinger, afin de réaliser un suivi de tendance à haute probabilité. Parallèlement, un mécanisme dynamique de prise de profit et de stop-loss est introduit pour contrôler efficacement le risque unilatéral.

Principe de la stratégie

- Calculer les indicateurs de volume d'achat et de vente sur une période personnalisée

- BV : volume d'achat, volume généré par les achats aux plus bas

- SV : volume de vente, volume généré par les ventes aux plus hauts

- Traiter les volumes d'achat et de vente

- Lisser à l'aide d'une EMA sur 20 périodes

- Séparer les signes positifs et négatifs des volumes traités

- Déterminer la direction de l'indicateur

- Indicateur supérieur à 0 : haussier, inférieur à 0 : baissier

- Combiner la VWAP hebdomadaire et les bandes de Bollinger pour détecter les divergences

- Prix au-dessus de la VWAP et indicateur haussier : signal d'achat

- Prix en dessous de la VWAP et indicateur baissier : signal de vente

- Stop-loss et take-profit dynamiques

- Définir les pourcentages de stop-loss et take-profit en fonction de l'ATR journalier

Avantages de la stratégie

- Les volumes d'achat et de vente reflètent la véritable dynamique du marché et captent l'énergie potentielle de la tendance.

- La VWAP hebdomadaire détermine la direction de la tendance à long terme, les bandes de Bollinger identifient les signaux de rupture.

- Le réglage dynamique du stop-loss et take-profit basé sur l'ATR permet de verrouiller au maximum les profits et d'éviter les dépassements.

Risques de la stratégie

- Les données de volume d'achat et de vente comportent une certaine marge d'erreur, ce qui peut entraîner des erreurs de jugement.

- La combinaison d'un seul indicateur peut générer des faux signaux.

- Un paramétrage inapproprié des bandes de Bollinger peut réduire les ruptures valides.

Directions d'optimisation de la stratégie

- Optimiser les indicateurs de volume d'achat et de vente sur plusieurs périodes.

- Ajouter des indicateurs auxiliaires tels que le volume des transactions pour filtrer.

- Ajuster dynamiquement le paramètre des bandes de Bollinger pour améliorer l'efficacité des ruptures.

Conclusion

Cette stratégie exploite pleinement la capacité prédictive des volumes d'achat et de vente, soutenue par la VWAP et les bandes de Bollinger pour générer des signaux à haute probabilité. Grâce à un stop-loss et take-profit dynamiques, elle contrôle efficacement les risques, ce qui en fait une stratégie de trading quantitatif efficace et stable. Avec l'optimisation continue des paramètres et des règles, les résultats devraient devenir encore plus significatifs.

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

- 1