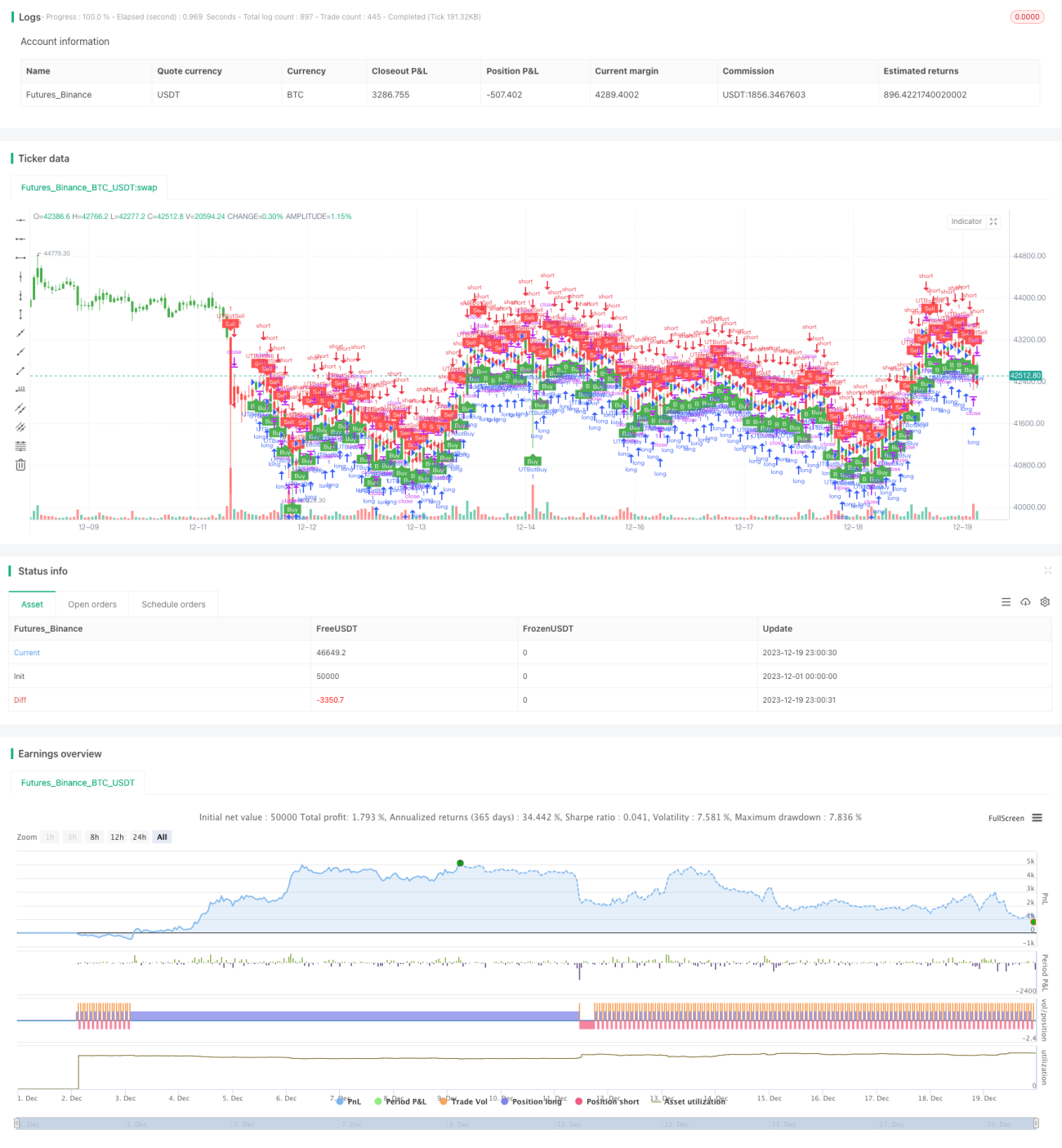

Stratégie de suivi de tendance avec stop suiveur adaptatif basé sur ATR et RSI

Aperçu

Cette stratégie combine l'Average True Range (ATR), le Relative Strength Index (RSI) et un stop suiveur pour réaliser un suivi de tendance adaptatif. L'ATR est utilisé pour calculer un niveau de stop dynamique, le RSI pour déterminer la direction du marché, et le stop suiveur pour suivre les fluctuations de prix afin de maximiser les profits. Il s'agit d'une stratégie de suivi de tendance très classique.

Principe de la stratégie

-

Calcul de l'ATR. L'ATR reflète la volatilité et le niveau de risque du marché. Cette stratégie utilise l'ATR pour calculer un stop dynamique, permettant un stop adaptatif.

-

Calcul du RSI. Le RSI permet d'identifier les conditions de surachat ou de survente. Lorsque le RSI est supérieur à 50, la tendance est haussière ; lorsqu'il est inférieur à 50, elle est baissière. Cette stratégie utilise le RSI pour déterminer la direction de la tendance des prix.

-

Suivi par stop suiveur. Sur la base du stop calculé par l'ATR et de la direction de tendance identifiée par le RSI, la stratégie met en œuvre un stop suiveur qui s'ajuste en continu aux fluctuations des prix, garantissant un stop tout en élargissant progressivement le niveau de take-profit pour maximiser les gains.

-

Plus précisément, un ordre long est ouvert lorsque le RSI est supérieur à 50, et un ordre court lorsque le RSI est inférieur à 50. Ensuite, le stop suiveur basé sur l'ATR est utilisé pour suivre les mouvements de prix.

Analyse des avantages

-

L'utilisation de l'ATR permet un stop adaptatif qui s'ajuste dynamiquement en fonction de la volatilité du marché, évitant les inconvénients d'un stop trop large ou trop serré.

-

Le RSI fournit une indication fiable de la direction de la tendance, évitant ainsi de se faire piéger dans des marchés sans tendance claire (range).

-

Le stop suiveur qui suit les fluctuations de prix permet d'élargir le take-profit et de profiter pleinement de la tendance.

Analyse des risques

-

Les paramètres de l'ATR et du RSI doivent être optimisés par backtesting, faute de quoi l'efficacité de la stratégie pourrait être compromise.

-

Bien qu'un stop soit en place, il est difficile d'éviter le risque de franchissement du stop en cas de gap important. Il est possible de réduire la taille des positions pour contrôler le risque.

-

La stratégie dépend fortement de l'optimisation des paramètres en fonction de l'instrument négocié ; il est nécessaire d'ajuster les paramètres pour chaque instrument.

Pistes d'optimisation

-

On peut envisager d'intégrer des algorithmes d'apprentissage automatique pour optimiser les paramètres de manière adaptative.

-

Ajouter un module de gestion de la taille des positions, permettant d'ajuster dynamiquement la taille en fonction des conditions du marché et de réduire la probabilité de franchissement du stop.

-

Ajouter des indicateurs de détection de tendance pour éviter les pertes dues à des retournements de tendance non anticipés.

Résumé

Cette stratégie intègre l'ATR, le RSI et le stop suiveur pour former une stratégie de suivi de tendance adaptative typique. Grâce à l'optimisation des paramètres, elle peut s'adapter de manière très flexible à différents instruments, ce qui en fait une stratégie de suivi de tendance universelle recommandable. Après l'ajout d'indicateurs supplémentaires et l'optimisation par apprentissage automatique, ses performances peuvent encore être améliorées.

- 1