Stratégie de suivi de tendance avec canal de prix à double moyenne mobile

Aperçu

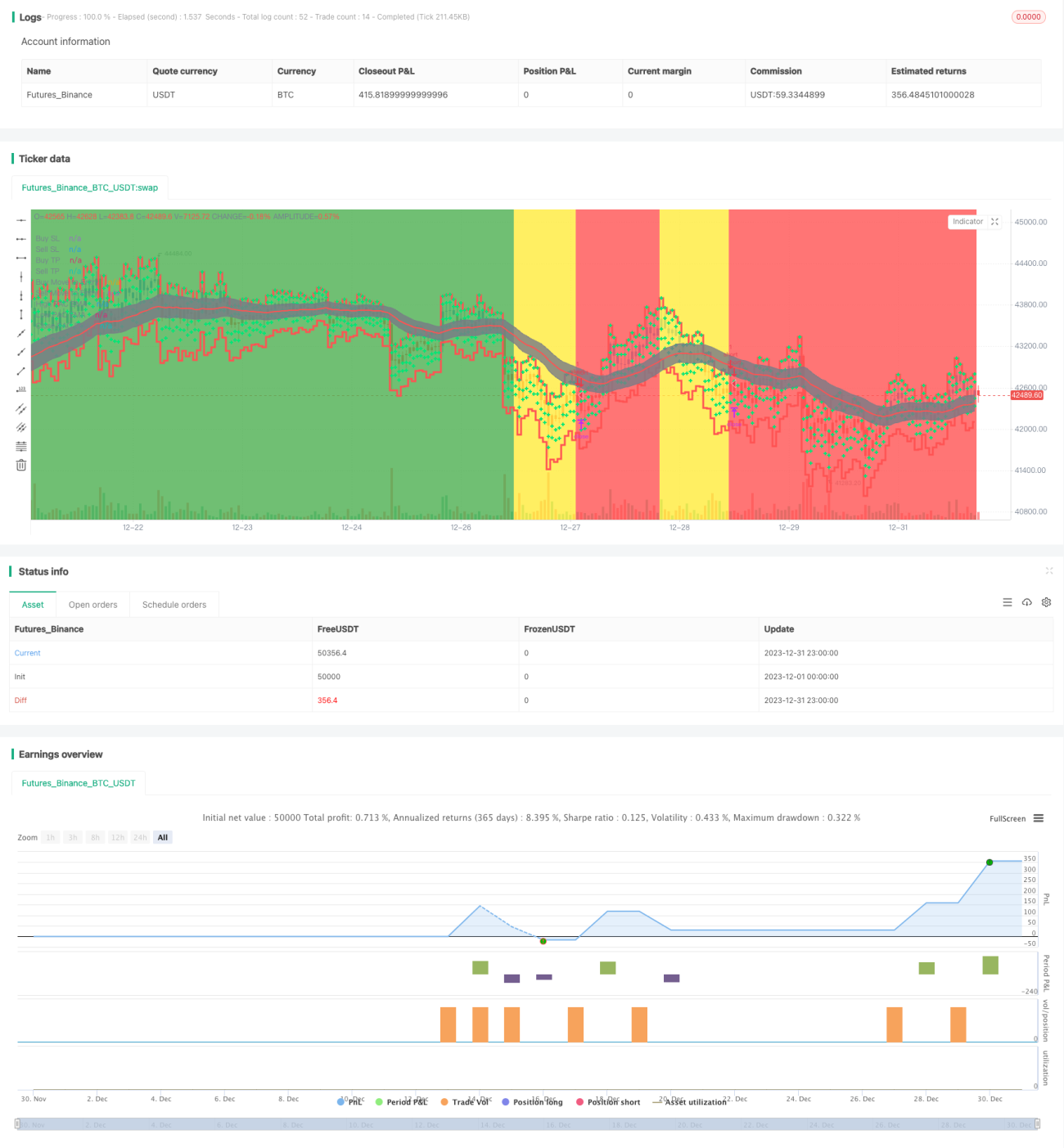

Cette stratégie est une stratégie de suivi de tendance qui utilise une double moyenne mobile pour construire un canal de prix, utilise la plage du canal pour déterminer la direction de la tendance des prix, et définit un stop suiveur pour verrouiller les bénéfices.

Principe de la stratégie

La stratégie de canal de prix à double moyenne mobile utilise une EMA rapide et une EMA lente pour construire le canal de prix. La période de l'EMA rapide est de 89, et celle de l'EMA lente est de 200. En parallèle, trois moyennes mobiles basées sur le prix haut, le prix bas et le prix de clôture sont utilisées pour construire la plage du canal de prix. Les bandes supérieure et inférieure du canal sont respectivement l'EMA du prix haut sur 34 périodes et l'EMA du prix bas sur 34 périodes.

Lorsque l'EMA rapide est au-dessus de l'EMA lente et que le prix est inférieur à la bande inférieure, la tendance est jugée haussière ; lorsque l'EMA rapide est en dessous de l'EMA lente et que le prix est supérieur à la bande supérieure, la tendance est jugée baissière.

En tendance haussière, la stratégie prend une position courte lorsque le retournement de tendance est confirmé ; en tendance baissière, elle prend une position longue lorsque le retournement est confirmé.

De plus, la stratégie intègre une fonction de stop suiveur. Après l'ouverture d'une position, le prix de stop suiveur est mis à jour en temps réel pour verrouiller les bénéfices.

Analyse des avantages

Le principal avantage de cette stratégie est d'utiliser la double moyenne mobile pour construire un canal de prix afin de déterminer la tendance des prix, puis d'agir sur les retournements, évitant ainsi d'acheter au sommet et de vendre au creux. La fonction de stop suiveur mobile permet de verrouiller les bénéfices et de réduire le risque de perte.

Autres avantages : grande flexibilité d'optimisation des paramètres, possibilité d'ajuster pour différentes paires et périodes ; mise à jour en temps réel du prix de stop, faible risque opérationnel.

Analyse des risques

Le principal risque de cette stratégie réside dans l'efficacité de la détection des signaux de retournement, qui peut entraîner de fausses indications. Il convient alors d'optimiser les paramètres pour garantir une bonne détection du retournement de tendance.

De plus, le réglage du stop est crucial. Un stop trop large peut entraîner un manque de réactivité ; un stop trop serré peut provoquer des sorties excessives. Cela doit être adapté en fonction du produit spécifique.

Enfin, des problèmes de données peuvent également rendre la stratégie inefficace. Il faut s'assurer d'utiliser des données historiques fiables, continues et suffisantes pour le backtest et la validation en conditions réelles.

Pistes d'optimisation

L'optimisation de cette stratégie porte principalement sur les points suivants :

-

Les périodes de l'EMA rapide et de l'EMA lente peuvent être optimisées en testant différentes combinaisons de paramètres.

-

Les paramètres des bandes supérieure et inférieure du canal de prix peuvent également être ajustés pour trouver une période plus appropriée.

-

Le réglage du stop est crucial : différents paramètres peuvent être testés pour optimiser la stratégie de stop.

-

Il est possible de tester l'ajout d'autres indicateurs pour confirmer le retournement de tendance et améliorer l'efficacité des prises de position.

Résumé

Cette stratégie présente un processus global cohérent et fluide : elle utilise le canal de prix à double moyenne mobile pour déterminer la direction de la tendance, agit en conséquence, et intègre un stop suiveur pour verrouiller les bénéfices. C'est une stratégie de suivi de tendance relativement stable. Grâce à l'optimisation des paramètres et à l'amélioration de la gestion des risques, elle peut devenir une stratégie de trading quantitatif efficace.

- 1