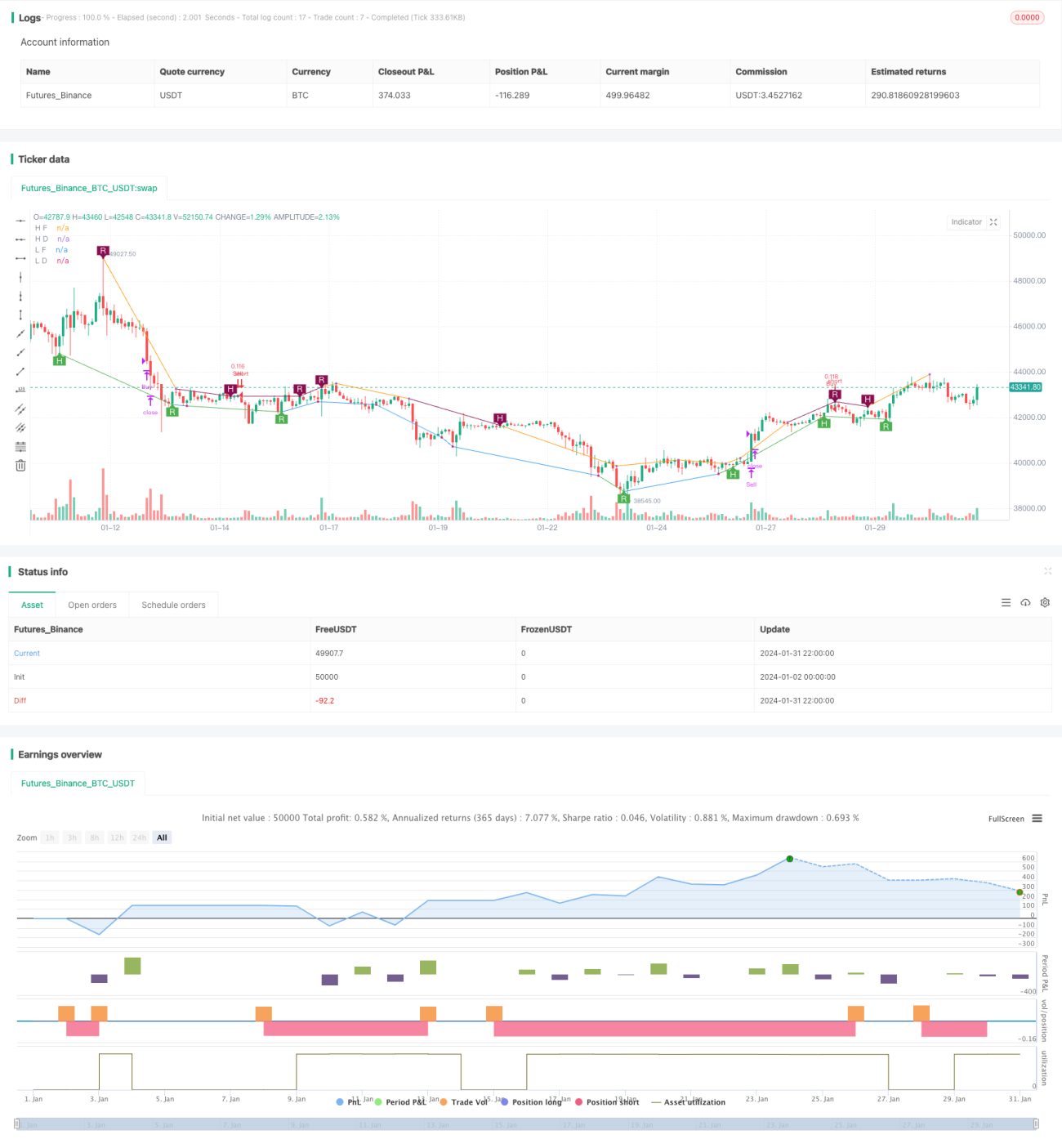

Stratégie de trading de tendance basée sur la divergence des prix

Aperçu

Cette stratégie est une stratégie de trading de tendance basée sur les signaux de divergence de prix. Elle utilise plusieurs indicateurs pour détecter les signaux de divergence de prix, tels que le RSI, le MACD, le Stochastique, etc., et les confirme via l'oscillateur de Murrey Math. Lorsqu'un signal de divergence de prix apparaît et que l'oscillateur confirme également la direction actuelle de la tendance, une entrée en position est effectuée.

Principe de la stratégie

Le cœur de cette stratégie repose sur la théorie de la divergence de prix. Lorsque le prix atteint un nouveau sommet mais que l'indicateur n'atteint pas un nouveau sommet, on parle de divergence baissière ; lorsque le prix atteint un nouveau creux mais que l'indicateur n'atteint pas un nouveau creux, on parle de divergence haussière. Cela indique un possible renversement de tendance. La stratégie combine les points hauts et bas d'un motif de fraction avec l'oscillateur pour confirmer les signaux de trading.

Plus précisément, les conditions d'entrée de la stratégie sont les suivantes :

- Détection d'un signal de divergence de prix, y compris la divergence régulière et la divergence cachée.

- L'oscillateur de Murrey Math se trouve dans la zone de tendance correspondante.

La condition de sortie est la fermeture de la position lorsque l'oscillateur repasse en dessous de la ligne médiane.

Analyse des avantages

Cette stratégie combine la théorie de la divergence de prix avec la confirmation de tendance, offrant les avantages suivants :

- Utilisation des signaux de divergence de prix pour détecter les points de renversement potentiels de tendance.

- Application d'un oscillateur pour confirmer la tendance actuelle, évitant les faux cassages.

- Combinaison de multiples indicateurs et paramètres, permettant un ajustement flexible.

- Équilibre entre le suivi de tendance et la prévention des pertes.

- Logique claire et large marge d'optimisation du code.

Analyse des risques

Les principaux risques proviennent des aspects suivants :

- Les signaux de divergence de prix peuvent être de faux signaux, ne confirmant pas totalement le renversement de tendance.

- Un réglage inapproprié des paramètres de l'oscillateur peut entraîner des entrées manquées et des opportunités de trading perdues.

- Une prépondérance excessive des positions longues ou courtes peut entraîner un risque de perte important.

- Pendant les périodes de forte volatilité, le nombre de transactions et les coûts de slippage peuvent augmenter fortement.

Il est recommandé de définir des stop-loss, d'ajuster les positions et d'optimiser la combinaison des paramètres pour réduire les risques.

Directions d'optimisation

Cette stratégie offre encore des possibilités d'optimisation :

- Ajout d'algorithmes d'apprentissage automatique pour optimiser en temps réel la combinaison des paramètres.

- Intégration de techniques de stop-loss adaptatives, telles que le trailing stop, le stop moyen, etc.

- Combinaison avec davantage d'indicateurs et de conditions de filtrage pour améliorer le rapport signal/bruit.

- Ajustement dynamique des paramètres de l'oscillateur pour optimiser le jugement de tendance.

- Optimisation de la gestion des risques, avec l'établissement de limites comme le drawdown maximal.

Résumé

Cette stratégie intègre la théorie de la divergence de prix et les indicateurs d'analyse de tendance, permettant de détecter efficacement les points de retournement de tendance potentiels. Associée à des mesures de gestion des risques optimisées, elle peut offrir un bon rendement de la stratégie. À l'avenir, elle pourra être optimisée à l'aide de méthodes avancées telles que l'apprentissage automatique pour obtenir des rendements excédentaires plus stables.

- 1