दोहरी मूविंग एवरेज गोल्डन क्रॉस और डेड क्रॉस क्वांटिटेटिव स्ट्रैटेजी

सारांश

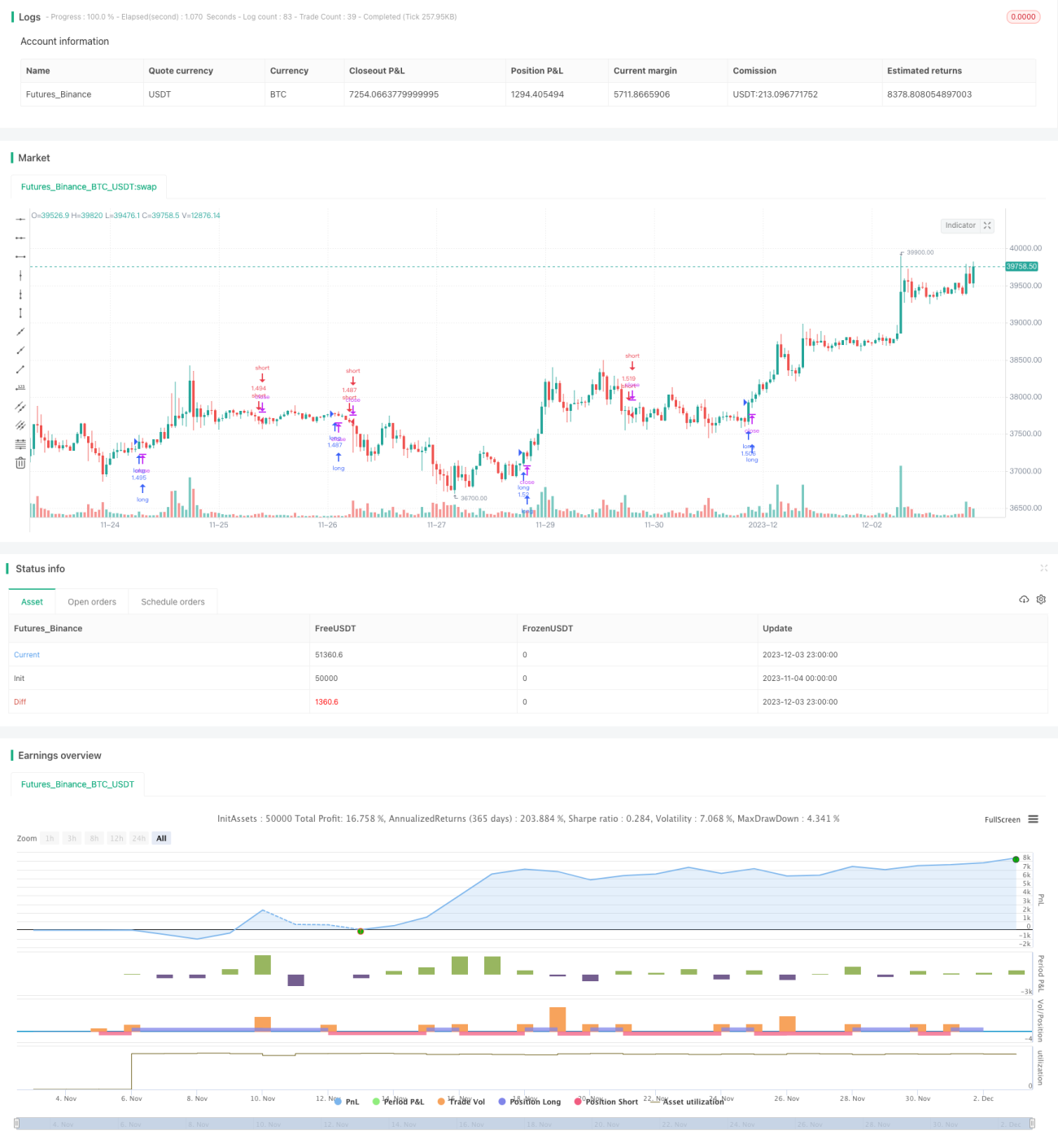

यह रणनीति दो ALMA मूविंग एवरेज के गोल्डन क्रॉस और डेड क्रॉस सिग्नल को MACD इंडिकेटर के बुलिश और बेयरिश सिग्नल के साथ मिलाकर स्वचालित रूप से लॉन्ग और शॉर्ट पोजीशन लेती है। रणनीति 4 घंटे और उससे ऊपर के टाइमफ्रेम के लिए उपयुक्त है। परीक्षण डेटा BNB/USDT है, समय अवधि 2017 से अब तक है, और शुल्क 0.03% निर्धारित किया गया है।

रणनीति का सिद्धांत

रणनीति ALMA फास्ट लाइन और स्लो लाइन का उपयोग करके दोहरी मूविंग एवरेज बनाती है। फास्ट लाइन की लंबाई 20 है, स्लो लाइन की लंबाई 40 है, दोनों में 0.9 का ऑफसेट और 5 का मानक विचलन (स्टैंडर्ड डेविएशन) है। जब फास्ट लाइन स्लो लाइन को ऊपर से क्रॉस करती है, तो लॉन्ग सिग्नल उत्पन्न होता है; जब फास्ट लाइन स्लो लाइन को नीचे से क्रॉस करती है, तो शॉर्ट सिग्नल उत्पन्न होता है।

साथ ही, रणनीति MACD इंडिकेटर के हिस्टोग्राम सिग्नल को भी शामिल करती है। लॉन्ग सिग्नल तभी मान्य होता है जब MACD हिस्टोग्राम पॉजिटिव (बढ़ रहा हो) हो; शॉर्ट सिग्नल तभी मान्य होता है जब MACD हिस्टोग्राम नेगेटिव (गिर रहा हो) हो।

रणनीति में टेक प्रॉफिट और स्टॉप लॉस की शर्तें भी निर्धारित की गई हैं। लॉन्ग के लिए टेक प्रॉफिट 2 गुना और स्टॉप लॉस 0.2 गुना है; शॉर्ट के लिए टेक प्रॉफिट 0.05 गुना और स्टॉप लॉस 1 गुना है।

लाभ विश्लेषण

यह रणनीति दोहरी मूविंग एवरेज के ट्रेंड निर्णय और MACD इंडिकेटर के ऊर्जा निर्णय को जोड़ती है, जो झूठे सिग्नल को प्रभावी ढंग से फ़िल्टर कर सकती है और प्रवेश की सटीकता में सुधार कर सकती है। टेक प्रॉफिट और स्टॉप लॉस का उचित निर्धारण लाभ को अधिकतम करने और बड़े नुकसान से बचने में मदद करता है।

बैकटेस्ट डेटा 2017 से अपनाया गया है, जिसमें कई बुल और बेयर मार्केट चक्र शामिल हैं। रणनीति क्रॉस-साइकिल परिस्थितियों में भी अच्छा प्रदर्शन करती है। यह साबित करता है कि रणनीति बाजार की रैखिक और गैर-रैखिक विशेषताओं के अनुकूल है।

जोखिम विश्लेषण

इस रणनीति में निम्नलिखित जोखिम हैं:

- दोहरी मूविंग एवरेज स्वयं में अंतर्निहित लैग (विलंब) होता है, जिससे अल्पकालिक अवसर छूट सकते हैं।

- जब MACD हिस्टोग्राम शून्य होता है, तो रणनीति कोई सिग्नल उत्पन्न नहीं करेगी।

- टेक प्रॉफिट और स्टॉप लॉस का अनुपात पूर्व-निर्धारित है, जो वास्तविक बाजार स्थितियों से भिन्न हो सकता है।

समाधान:

- मूविंग एवरेज की अवधि को उचित रूप से छोटा करके अल्पकालिक संवेदनशीलता बढ़ाएं।

- MACD मापदंडों को अनुकूलित करें ताकि हिस्टोग्राम अधिक बार उतार-चढ़ाव करे।

- टेक प्रॉफिट और स्टॉप लॉस की सेटिंग को गतिशील रूप से समायोजित करें।

अनुकूलन दिशाएँ

इस रणनीति को निम्नलिखित पहलुओं से और अनुकूलित किया जा सकता है:

- विभिन्न प्रकार के मूविंग एवरेज आज़माएं ताकि बेहतर स्मूथिंग प्रभाव प्राप्त हो सके।

- विभिन्न उपकरणों और समय-सीमाओं के अनुरूप मूविंग एवरेज और MACD के मापदंडों को अनुकूलित करें।

- अतिरिक्त शर्तें जोड़ें, जैसे कि ट्रेडिंग वॉल्यूम में बदलाव, सिग्नल को फ़िल्टर करने के लिए।

- टेक प्रॉफिट और स्टॉप लॉस के अनुपात को वास्तविक समय में समायोजित करें ताकि रणनीति अधिक अनुकूल हो।

निष्कर्ष

यह रणनीति मूविंग एवरेज के ट्रेंड निर्णय और MACD के सहायक निर्णय को सफलतापूर्वक जोड़ती है, और उचित टेक प्रॉफिट और स्टॉप लॉस निर्धारित करती है, जो विभिन्न बाजार स्थितियों में स्थिर लाभ प्राप्त कर सकती है। मापदंडों के निरंतर अनुकूलन और अतिरिक्त फ़िल्टरिंग शर्तों को जोड़ने जैसे उपायों के माध्यम से रणनीति की स्थिरता और लाभ क्षमता को और बढ़ाया जा सकता है।

- 1