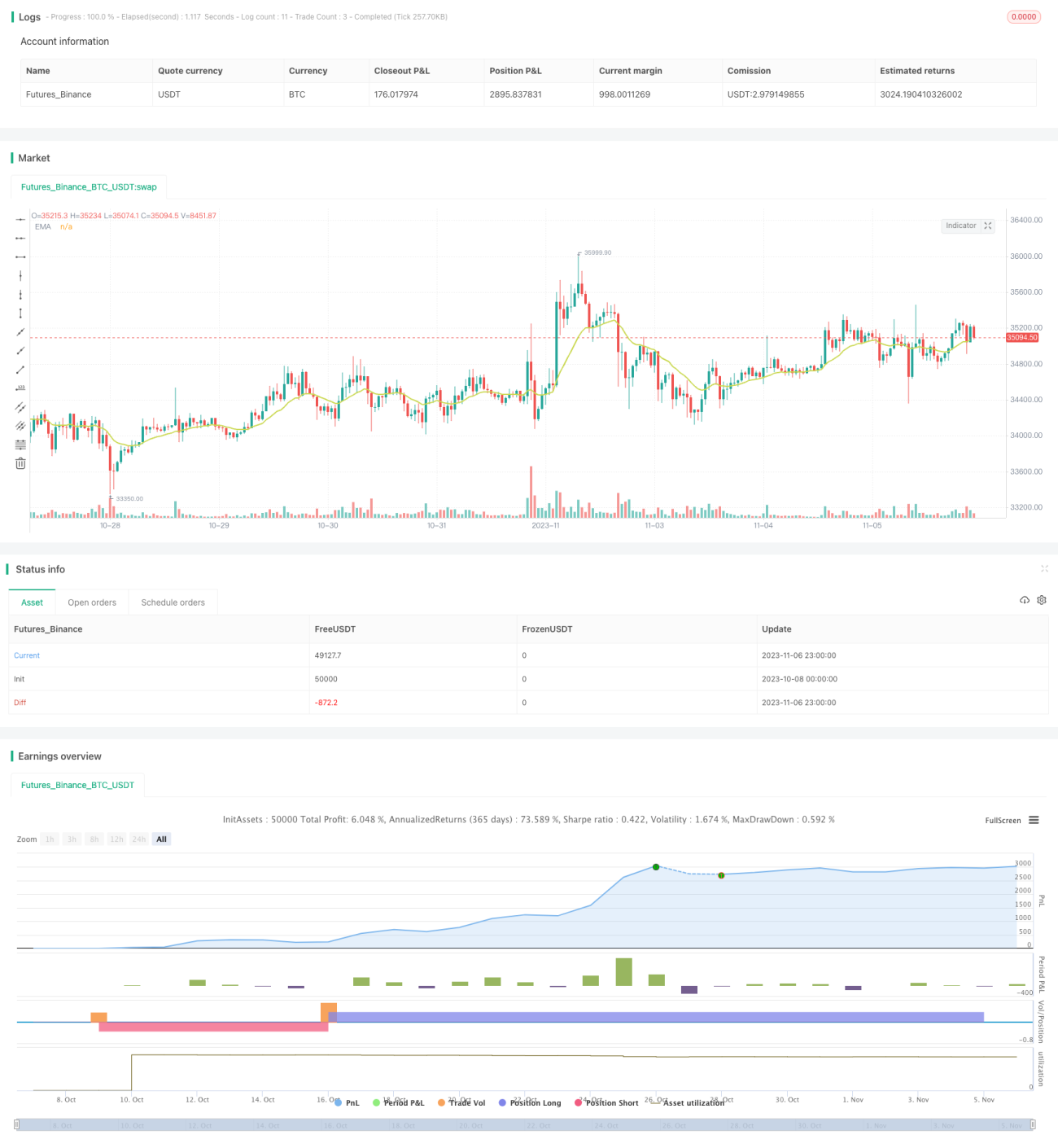

Strategi Breakout Dua Arah RSI

Ringkasan

Strategi ini dirancang berdasarkan indikator Relative Strength Index (RSI), memanfaatkan prinsip overbought dan oversold dari RSI untuk melakukan operasi breakout dua arah. Ketika RSI menembus ke atas garis overbought yang telah ditentukan, lakukan posisi long; ketika RSI menembus ke bawah garis oversold yang telah ditentukan, lakukan posisi short. Ini adalah strategi trading reversal yang khas.

Prinsip Strategi

-

Atur parameter untuk menghitung indikator RSI berdasarkan input pengguna, termasuk panjang periode RSI, ambang batas overbought, dan ambang batas oversold.

-

Tentukan apakah berada di zona overbought atau oversold berdasarkan posisi kurva RSI relatif terhadap garis overbought dan oversold.

-

Ketika indikator RSI menembus garis ambang yang sesuai dari zona oversold, lakukan operasi pembukaan posisi ke arah yang berlawanan. Misalnya, ketika menembus ke bawah dari zona overbought melewati garis overbought, dianggap terjadi pembalikan pasar, pada saat itu buka posisi long; ketika menembus ke atas dari zona oversold melewati garis oversold, dianggap terjadi pembalikan pasar, pada saat itu buka posisi short.

-

Setelah membuka posisi, tetapkan garis stop loss dan take profit. Pantau kondisi stop loss dan take profit, dan tutup posisi saat kondisi terpenuhi.

-

Strategi ini juga menyediakan fungsi opsional menggunakan EMA sebagai filter. Hanya ketika sinyal long atau short dari RSI terjadi bersamaan dengan harga yang menembus EMA, posisi dibuka.

-

Strategi juga menyediakan fungsi untuk hanya bertransaksi pada sesi perdagangan tertentu. Pengguna dapat mengatur untuk hanya bertransaksi dalam rentang waktu tertentu, dan menutup posisi setelah waktu tersebut.

Analisis Keunggulan

- Menggunakan prinsip breakout klasik RSI, hasil backtesting cukup baik.

- Ambang batas overbought/oversold dapat diatur secara fleksibel, disesuaikan dengan instrumen yang berbeda.

- Dapat memilih apakah akan menggunakan filter EMA untuk menghindari seringnya buka/tutup posisi akibat fluktuasi kecil.

- Mendukung fungsi stop loss dan take profit, yang dapat meningkatkan stabilitas strategi.

- Mendukung pengaturan sesi perdagangan tertentu, menghindari perdagangan di waktu yang tidak sesuai.

- Mendukung perdagangan dua arah long dan short, dapat memanfaatkan fluktuasi pasar secara maksimal.

Analisis Risiko

- Indikator RSI rentan mengalami divergensi, hanya mengandalkan RSI dapat menghasilkan sinyal trading yang tidak akurat. Perlu dikombinasikan dengan tren, moving average, dll.

- Pengaturan ambang batas overbought/oversold yang tidak tepat dapat menyebabkan frekuensi trading yang terlalu tinggi atau melewatkan peluang.

- Pengaturan stop loss/take profit yang tidak tepat dapat membuat strategi terlalu agresif atau konservatif.

- Pengaturan filter EMA yang tidak tepat juga dapat menyebabkan melewatkan peluang trading atau menyaring sinyal yang valid.

Solusi Risiko:

- Optimalkan parameter RSI, sesuaikan dengan parameter yang cocok untuk instrumen yang berbeda.

- Kombinasikan dengan indikator tren, dll., untuk mendeteksi divergensi dan menghindari sinyal yang salah.

- Uji dan optimalkan parameter stop loss/take profit untuk menemukan parameter terbaik.

- Uji dan optimalkan parameter EMA untuk menemukan level filter terbaik.

Arah Optimasi Strategi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

-

Optimalkan parameter RSI, cari kombinasi parameter terbaik untuk instrumen yang berbeda. Dapat dilakukan dengan backtesting menyeluruh untuk menemukan ambang overbought/overshot terbaik.

-

Coba ganti atau kombinasikan RSI dengan indikator lain untuk menghasilkan sinyal yang lebih kuat. Misalnya MACD, KD, Bollinger Bands, dll.

-

Optimalkan strategi stop loss/take profit untuk meningkatkan stabilitas strategi. Dapat menggunakan trailing stop berdasarkan volatilitas pasar, atau strategi dengan trailing stop.

-

Optimalkan parameter filter EMA atau uji filter indikator lain untuk lebih menghindari jebakan.

-

Tambahkan modul penentuan tren untuk menghindari posisi short di pasar bullish atau posisi long di pasar bearish.

-

Uji parameter sesi perdagangan yang berbeda untuk menentukan sesi mana yang cocok untuk strategi ini dan sesi mana yang harus dihindari.

Kesimpulan

Strategi breakout dua arah RSI ini memiliki ide yang jelas secara keseluruhan, memanfaatkan prinsip overbought/oversold klasik RSI untuk melakukan trading reversal. Strategi ini dapat menangkap peluang pembalikan di zona overbought/oversold, sekaligus mengendalikan risiko melalui filter EMA dan stop loss/take profit. Dengan ruang optimasi parameter dan modul yang cukup besar, strategi ini dapat dikembangkan menjadi strategi reversal yang cukup stabil dan andal. Layak untuk diuji lebih lanjut dan dioptimalkan sebelum diterapkan secara praktis.

- 1