Strategi Pelacakan Tren dengan Stop Loss Bergerak Adaptif Berdasarkan ATR dan RSI

Ikhtisar

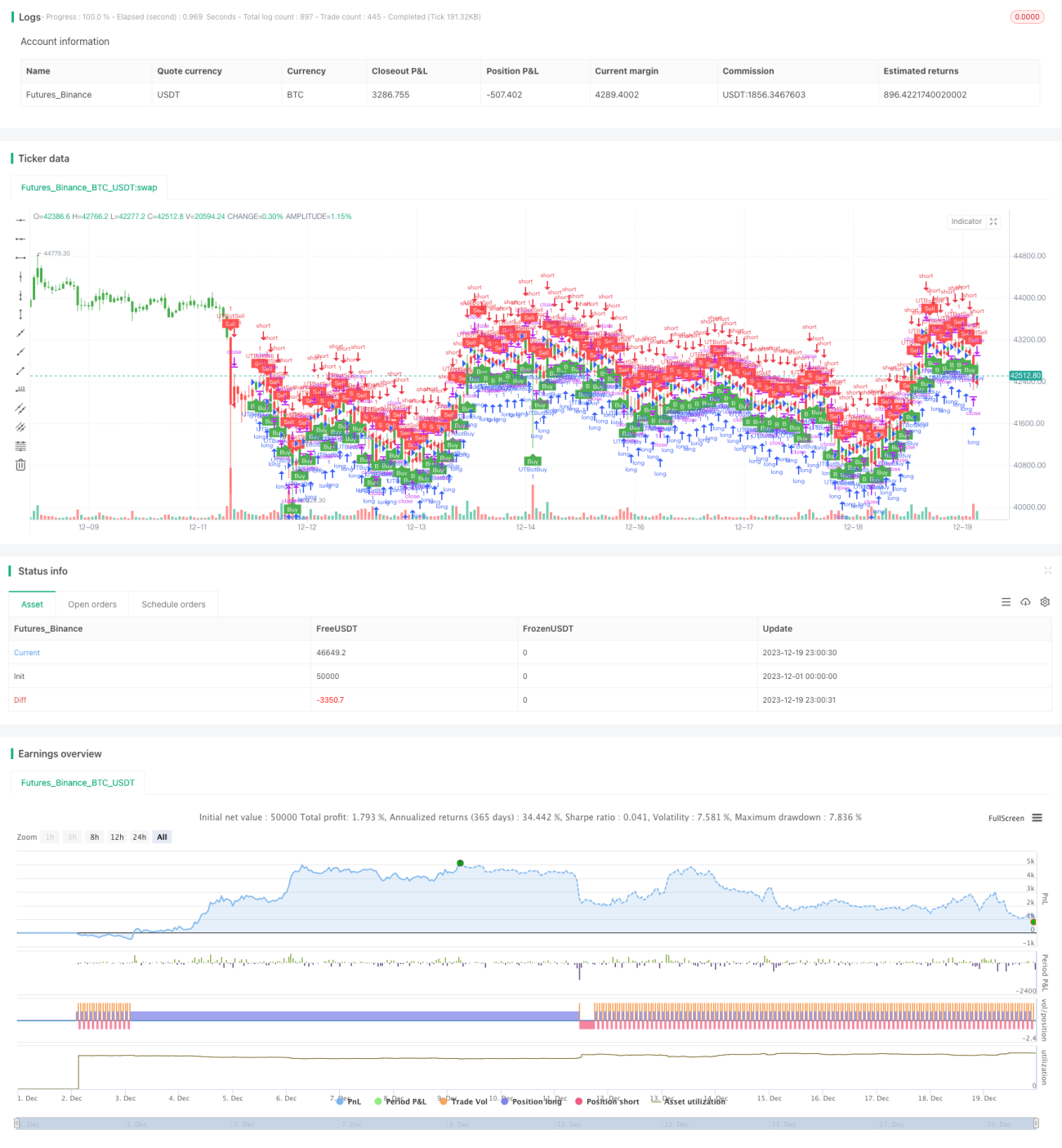

Strategi ini secara komprehensif menggunakan Average True Range (ATR), Relative Strength Index (RSI), dan trailing stop untuk mencapai trend following yang adaptif. Dengan ATR untuk menghitung level stop loss dinamis, RSI untuk menentukan arah tren pasar, dan trailing stop untuk mengikuti fluktuasi harga guna memaksimalkan keuntungan. Ini adalah strategi trend following yang sangat khas.

Prinsip Strategi

-

Menghitung ATR. ATR mencerminkan volatilitas pasar dan tingkat risiko. Strategi ini menggunakan ATR untuk menghitung level stop loss dinamis, sehingga menghasilkan stop loss yang adaptif.

-

Menghitung RSI. RSI dapat mengidentifikasi kondisi overbought dan oversold di pasar. Ketika RSI di atas 50, itu menandakan bullish; di bawah 50, menandakan bearish. Strategi ini menggunakan RSI untuk menentukan arah tren harga.

-

Trailing stop. Berdasarkan level stop loss yang dihitung dari ATR dan arah tren yang ditentukan oleh RSI, strategi ini menerapkan trailing stop yang terus mengikuti fluktuasi harga, memastikan proteksi stop loss sambil secara bertahap memperlebar target take profit, sehingga memaksimalkan keuntungan.

-

Secara spesifik, ketika RSI di atas 50, buka posisi long; ketika di bawah 50, buka posisi short. Setelah itu, gunakan level stop loss yang dihitung dari ATR untuk melakukan trailing stop, mengikuti pergerakan harga.

Analisis Keunggulan

-

Menggunakan ATR untuk menghasilkan stop loss adaptif, yang dapat menyesuaikan jarak stop loss secara dinamis berdasarkan volatilitas pasar, menghindari kelemahan stop loss yang terlalu ketat atau terlalu longgar.

-

RSI memberikan indikasi arah tren yang akurat dan andal, membantu menghindari terjebak dalam pasar yang sideways.

-

Trailing stop mengikuti fluktuasi harga, dapat memperlebar target take profit, sehingga memaksimalkan keuntungan dari tren.

Analisis Risiko

-

Pengaturan parameter ATR dan RSI perlu dioptimalkan melalui backtesting, jika tidak, dapat mempengaruhi efektivitas strategi.

-

Meskipun ada perlindungan stop loss, risiko stop loss tertembus akibat gap yang besar sulit dihindari sepenuhnya. Posisi dapat diperkecil untuk mengelola risiko.

-

Strategi ini sangat bergantung pada optimasi parameter untuk instrumen trading yang berbeda, sehingga perlu penyesuaian parameter untuk setiap instrumen.

Arah Optimasi

-

Dapat dipertimbangkan untuk menambahkan algoritma machine learning guna mencapai optimasi parameter yang adaptif.

-

Menambahkan modul manajemen posisi yang dapat menyesuaikan ukuran posisi secara dinamis berdasarkan kondisi pasar, mengurangi kemungkinan stop loss tertembus.

-

Menambahkan indikator penentu tren untuk menghindari kerugian akibat melewatkan titik pembalikan puncak dan dasar.

Kesimpulan

Strategi ini mengintegrasikan modul ATR, RSI, dan trailing stop untuk membentuk strategi trend following adaptif yang khas. Dengan optimasi parameter, strategi ini dapat beradaptasi secara fleksibel dengan berbagai instrumen trading, menjadikannya strategi trend following serbaguna yang direkomendasikan. Setelah menambahkan lebih banyak indikator dan optimasi algoritma machine learning, efektivitas strategi ini dapat ditingkatkan lebih lanjut.

- 1