Strategi Indikator Mo Fei yang Melintasi Ruang dan Waktu

Ikhtisar

Ini adalah strategi kuantitatif sederhana yang menggunakan indikator Mofei untuk mengidentifikasi "hiu besar" di pasar. Strategi ini cocok untuk kerangka waktu 5 menit dan terutama digunakan dalam perdagangan mata uang kripto.

Prinsip Strategi

Strategi ini menggunakan indikator Mofei dengan panjang 3, menetapkan garis overbought pada 100 dan garis oversold pada 0. Strategi menunggu indikator Mofei mencapai level overbought, yang menunjukkan adanya "hiu besar" di pasar. Jika dua titik overbought indikator Mofei sebelumnya pada hari itu masih dapat mempertahankan tren naik harga, maka ini adalah sinyal masuk posisi beli (long).

Ketika indikator Mofei = 100 dan candle berikutnya adalah candle bullish besar, maka lakukan entry beli (long). Stop loss ditetapkan pada titik terendah hari perdagangan tersebut, dan take profit dalam 60 menit setelah entry.

Untuk posisi jual (short), dapat menggunakan logika cermin. Yaitu ketika indikator Mofei mencapai oversold dan candle berikutnya adalah candle bearish besar, maka lakukan entry jual (short).

Keunggulan Strategi

-

Menggunakan indikator Mofei dapat secara efektif mengidentifikasi perilaku "hiu besar" dalam mengakumulasi saham potensial di pasar, di mana saham tersebut memiliki kemungkinan untuk terus naik.

-

Menggunakan badan candle untuk mengidentifikasi titik breakout yang kuat dapat menyaring banyak breakout palsu.

-

Menggabungkan filter SMA untuk menghindari pembelian saham yang sedang dalam tren turun dapat secara efektif mengurangi risiko perdagangan.

-

Menggunakan metode operasi super jangka pendek intraday, take profit 60 menit dapat dengan cepat mengunci keuntungan dan mengurangi probabilitas penarikan (drawdown).

Risiko Strategi

-

Indikator Mofei dapat menghasilkan sinyal palsu, menyebabkan kerugian yang tidak perlu. Parameter dapat disesuaikan secara tepat atau ditambahkan indikator lain untuk penyaringan.

-

Metode operasi super jangka pendek 60 menit mungkin terlalu agresif, tidak cocok untuk saham dengan volatilitas tinggi. Waktu take profit dapat disesuaikan atau menggunakan trailing stop untuk optimalisasi.

-

Tidak mempertimbangkan risiko dampak pasar ketika peristiwa ekonomi makro besar terjadi. Pada saat itu, strategi harus dijeda dan perdagangan dilanjutkan setelah pasar kembali stabil.

Arah Optimasi Strategi

-

Dapat menguji kombinasi parameter yang berbeda, seperti menyesuaikan panjang indikator Mofei, mengoptimalkan parameter periode SMA, dll.

-

Coba tambahkan indikator lain untuk dikombinasikan, seperti Bollinger Bands, indikator KD, dll., untuk melihat apakah dapat meningkatkan akurasi sinyal.

-

Uji apakah melonggarkan lebar stop loss secara tepat dapat memperoleh keuntungan per perdagangan yang lebih besar.

-

Coba kembangkan versi yang berlaku untuk kerangka waktu lain berdasarkan kerangka strategi ini, seperti versi 15 menit atau 30 menit.

Kesimpulan

Secara keseluruhan, strategi ini sangat sederhana dan mudah dipahami, ide dasarnya konsisten dengan ide klasik mengikuti "hiu besar". Dengan mengidentifikasi titik-titik kunci overbought dan oversold dari indikator Mofei, dikombinasikan dengan penyaringan badan candle, banyak noise dapat disaring. Penambahan filter SMA juga semakin meningkatkan stabilitas strategi.

Cara operasi super jangka pendek 60 menit dapat menghasilkan keuntungan dengan cepat, tetapi juga membawa risiko operasional yang lebih tinggi. Secara keseluruhan, ini adalah template strategi kuantitatif yang sangat bernilai praktis, layak untuk diteliti dan dioptimalkan lebih lanjut, dan juga memberi kita ide pengembangan strategi yang berharga.

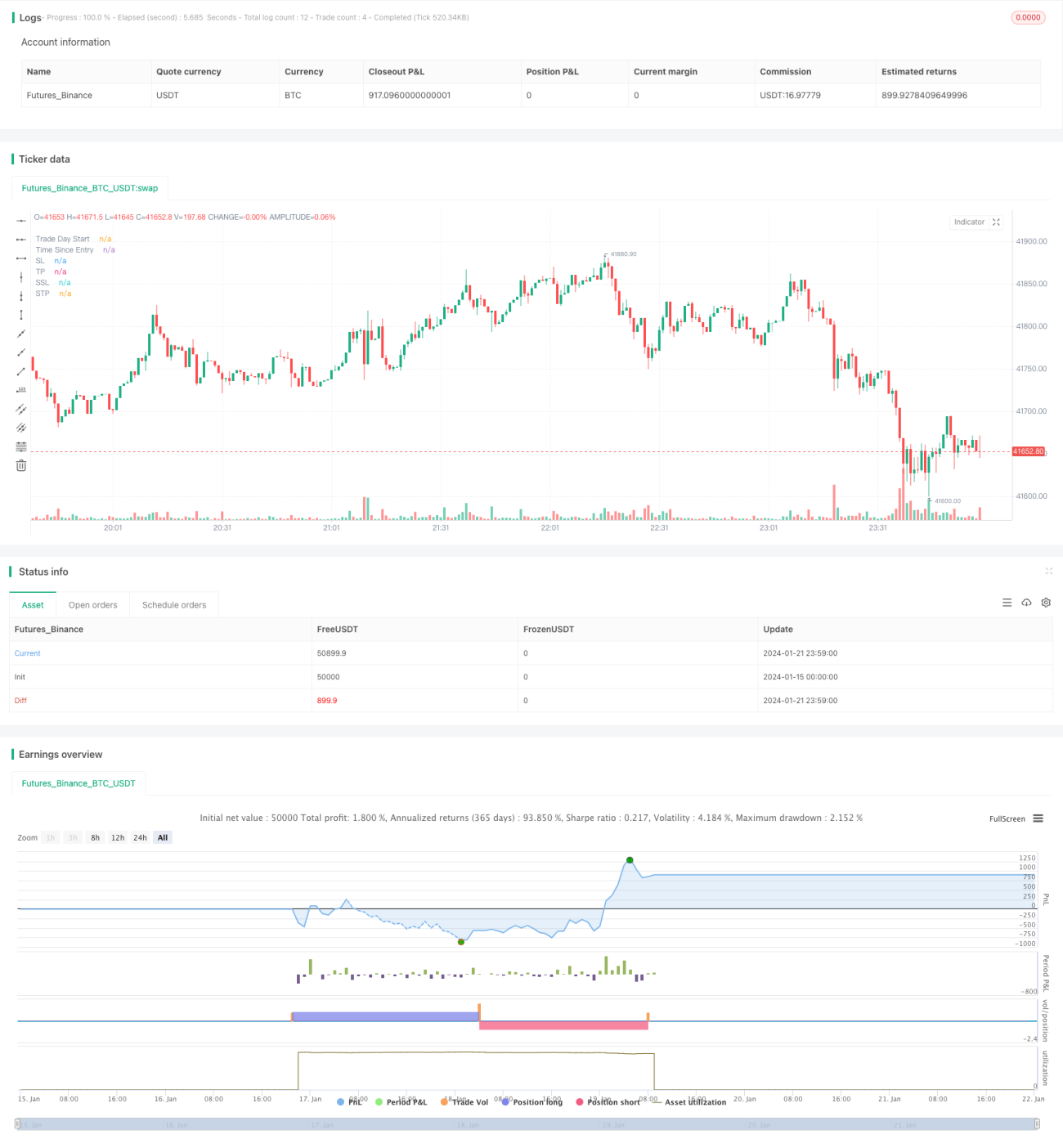

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1