Strategi Mengikuti Tren Saluran Harga dengan Dua Rata-rata Bergerak

Ikhtisar

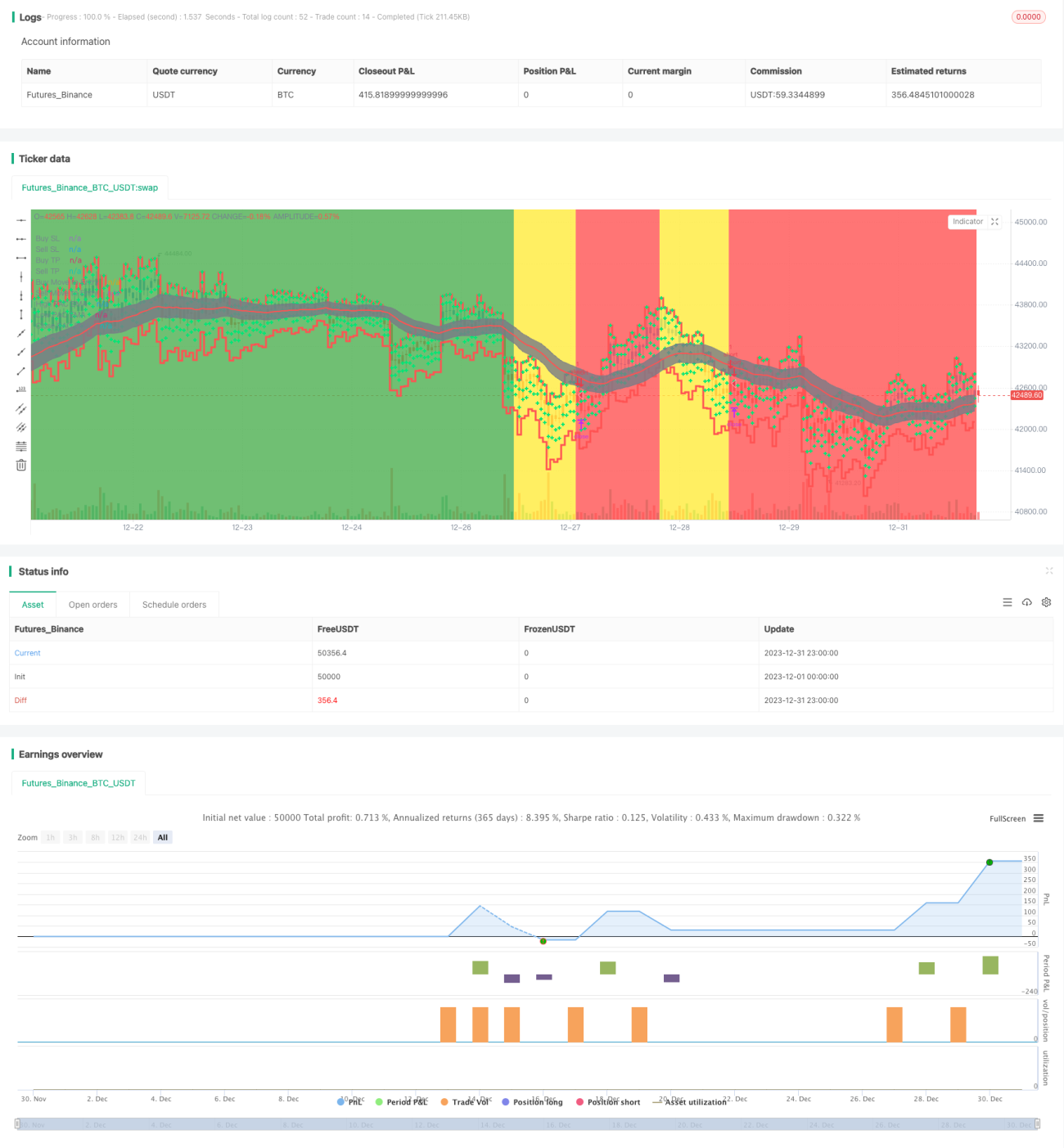

Strategi ini adalah strategi pelacakan tren yang membangun saluran harga berdasarkan dua rata-rata bergerak eksponensial (EMA), menggunakan rentang saluran untuk menentukan arah tren harga, dan menetapkan stop loss trailing untuk mengunci keuntungan.

Prinsip Strategi

Strategi saluran harga dengan dua EMA menggunakan EMA cepat dan EMA lambat untuk membangun saluran harga. Parameter EMA cepat adalah 89 periode, dan EMA lambat adalah 200 periode. Pada saat yang sama, digunakan tiga rata-rata bergerak berdasarkan harga tertinggi, harga terendah, dan harga penutupan untuk membangun rentang saluran harga. Garis atas dan garis bawah saluran masing-masing adalah EMA 34 periode dari harga tertinggi dan EMA 34 periode dari harga terendah.

Ketika EMA cepat berada di atas EMA lambat dan harga berada di bawah garis bawah, kondisi ini dianggap sebagai tren naik; ketika EMA cepat berada di bawah EMA lambat dan harga berada di atas garis atas, kondisi ini dianggap sebagai tren turun.

Dalam tren naik, strategi akan melakukan short ketika tren dipastikan berbalik; dalam tren turun, strategi akan melakukan long ketika tren dipastikan berbalik.

Selain itu, strategi dilengkapi dengan fungsi stop loss trailing. Setelah posisi terbuka, harga stop loss trailing akan diperbarui secara real-time untuk mengunci keuntungan.

Analisis Keunggulan

Keunggulan terbesar dari strategi ini adalah menggunakan dua EMA untuk membangun saluran harga guna menentukan arah tren, kemudian masuk posisi saat terjadi pembalikan, sehingga menghindari membeli di puncak atau menjual di lembah. Selain itu, dilengkapi dengan trailing stop loss yang dapat mengunci keuntungan dan mengurangi risiko kerugian.

Keunggulan lainnya meliputi: ruang optimasi parameter yang besar, dapat disesuaikan dengan instrumen dan periode yang berbeda; harga stop loss diperbarui secara real-time, risiko operasional rendah.

Analisis Risiko

Risiko utama strategi ini terletak pada efektivitas sinyal pembalikan yang mungkin kurang akurat, sehingga dapat terjadi kesalahan identifikasi. Dalam hal ini, perlu dilakukan optimasi parameter untuk memastikan efektivitas deteksi pembalikan tren.

Selain itu, pengaturan titik stop loss juga sangat krusial. Jika titik stop loss terlalu lebar, bisa terjadi eksekusi stop loss yang kurang tegas; jika terlalu sempit, bisa terjadi stop loss yang berlebihan. Hal ini perlu disesuaikan dengan instrumen spesifik.

Terakhir, masalah data juga dapat menyebabkan strategi tidak efektif. Pastikan menggunakan data historis yang terpercaya, kontinu, dan memadai untuk backtest dan validasi strategi secara real-time.

Arah Optimasi

Optimasi strategi ini terutama difokuskan pada beberapa aspek berikut:

-

Periode EMA cepat dan EMA lambat dapat dioptimalkan dengan mengatur berbagai kombinasi parameter untuk menguji efektivitasnya.

-

Parameter garis atas dan bawah saluran harga juga dapat disesuaikan untuk menemukan periode yang lebih sesuai.

-

Pengaturan titik stop loss sangat penting; parameter stop loss yang berbeda dapat diuji untuk mengoptimalkan strategi stop loss.

-

Dapat diuji apakah perlu menambahkan indikator lain untuk menentukan pembalikan tren guna meningkatkan efektivitas entry posisi.

Kesimpulan

Strategi ini memiliki alur kerja yang logis dan lancar secara keseluruhan. Dengan menggunakan saluran dua EMA untuk menentukan arah tren, dilengkapi dengan trailing stop loss untuk mengunci keuntungan, strategi ini merupakan strategi pelacakan tren yang relatif stabil. Melalui optimasi parameter dan pengaturan manajemen risiko, strategi ini dapat menjadi salah satu strategi trading kuantitatif yang efisien.

- 1