概要

スーパーモメンタム戦略は、複数のモメンタム指標を総合的に活用し、複数のモメンタム指標が同時に強気または弱気を示した場合に、買いまたは売りの注文を実行します。本戦略は、複数のモメンタム指標を組み合わせることで、価格トレンドをより正確に捉え、単一指標による誤ったシグナルを回避します。

戦略の原理

本戦略は、4つのEvergetのRMI指標と1つのChandeモメンタム・オシレーターを同時に使用します。RMI指標は価格のモメンタムに基づいて計算され、価格の上昇と下落の強さを判断します。Chande MOは価格変動を計算することで、市場の買われすぎ・売られすぎの状況を判断します。

RMI5がその買い線を上抜け、RMI4がその買い線を下抜け、RMI3がその買い線を下抜け、RMI2がその買い線を下抜け、RMI1がその買い線を下抜け、かつChande MOがその買い線を上抜けた場合、買い注文を実行します。

RMI5がその売り線を下抜け、RMI4がその売り線を上抜け、RMI3がその売り線を上抜け、RMI2がその売り線を上抜け、RMI1がその売り線を上抜け、かつChande MOがその売り線を下抜けた場合、売り注文を実行します。

RMI5は他のRMI指標とは逆方向に設定されており、これによりトレンドをより適切に識別し、ピラミッディング操作を行うことができます。

優位性の分析

- 複数の指標を総合することで、トレンドをより正確に判断し、単一指標による誤ったシグナルを回避できます。

- 複数の時間枠の指標を含むため、より大きなレベルのトレンドを識別できます。

- 逆方向のRMI指標は、トレンド識別とピラミッディング操作に役立ちます。

- Chande MOは、買われすぎ・売られすぎの状況での誤った取引を回避するのに役立ちます。

リスク分析

- 指標の組み合わせが多く、パラメータ設定が複雑であるため、慎重なテストと最適化が必要です。

- 複数の指標が同時に変化する場合、誤ったシグナルが発生する可能性があります。

- 複数の指標を総合するため、取引頻度が低くなる可能性があります。

- 指標パラメータが異なる銘柄や市場環境に適合するかどうかに注意する必要があります。

最適化の方向性

- 指標パラメータの設定をテストし、戦略の安定性を高めるためにパラメータを最適化します。

- 指標の追加または削減を試み、シグナルの品質への影響を評価します。

- 特定の市場状況での誤ったシグナルを回避するために、フィルター条件を導入することもできます。

- 指標の買い線・売り線の位置を調整し、最適なパラメータの組み合わせを見つけます。

- リスクをコントロールするために、ストップロスメカニズムの導入を検討します。

まとめ

本戦略は、複数のモメンタム指標を総合的に活用することで、市場トレンドの判断能力を向上させています。しかし、パラメータ設定が複雑であるため、慎重なテストと最適化、継続的な改良と調整が必要です。適切に使用すれば、優れた取引シグナルを得ることができ、市場トレンドを追跡する上で一定の優位性を持つ可能性があります。しかし、トレーダーはリスクに注意を払い、最適なパラメータの組み合わせを模索し、安定した取引を行うためにリスク管理メカニズムを追加する必要があります。

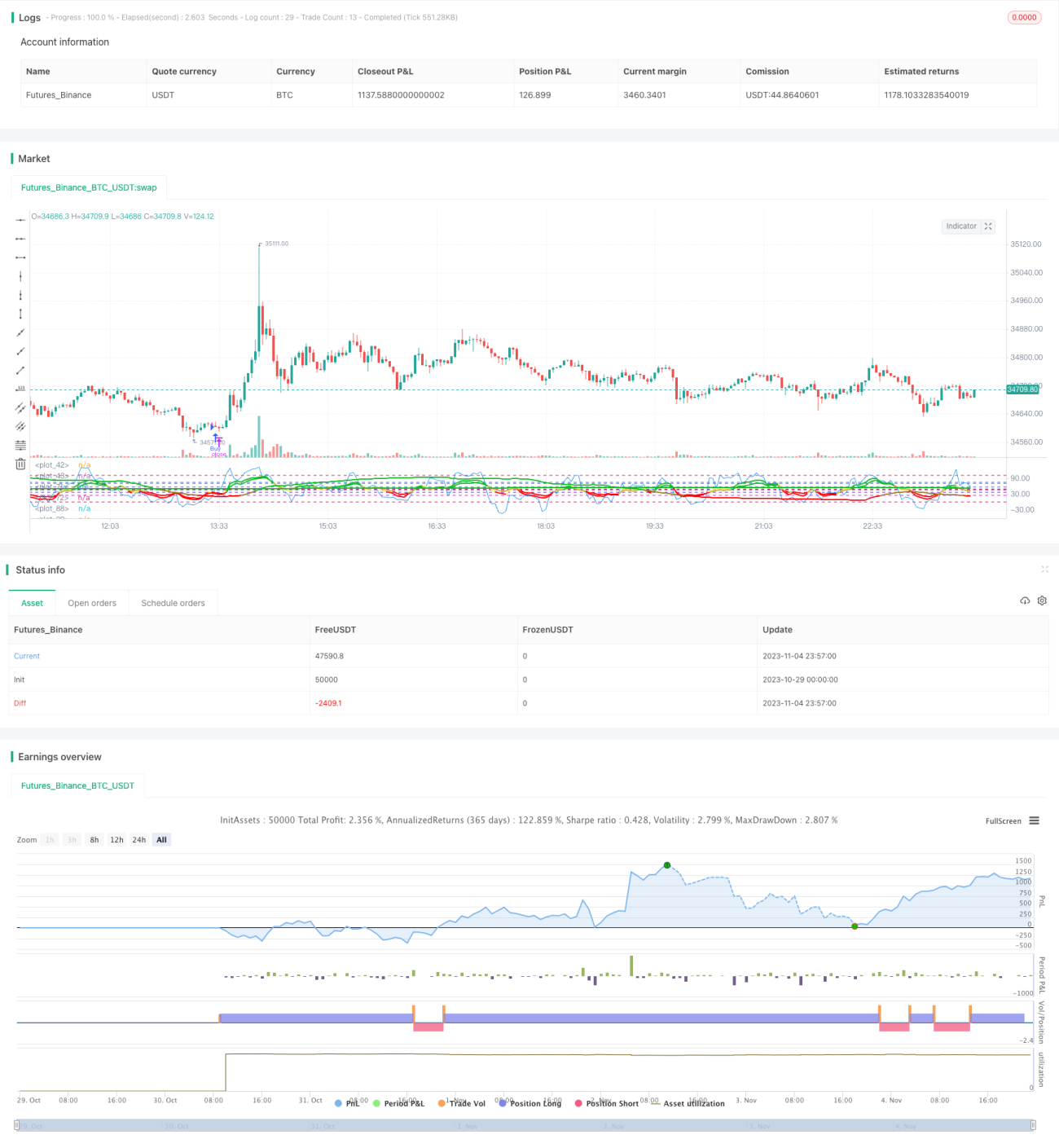

/*backtest

start: 2023-10-29 00:00:00

end: 2023-11-05 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Super Momentum Strat", shorttitle="SMS", format=format.price, precision=2)

//* Backtesting Period Selector | Component *//- 1