概要

前日高値ブレイクアウト戦略は、前日の高値を突破した時点でロングポジションを建てるトレンドフォロー型戦略です。当日中に複数回ブレイクしてもエントリー可能です。トレンドフォローを主な特徴とし、市場が明確なトレンドを示し、かつボラティリティが高い状況に適しています。

原理

本戦略は、一連の指標を用いてエントリーとイグジットのタイミングを判断します。

-

ROC曲線フィルター:当日の終値が前日の終値に対して設定された閾値以上の変動率を示した場合に戦略を起動します。この指標により、戦略に適合しないレンジ相場をフィルタリングします。

-

ブレイクアウトポイント:当日の高値、安値、始値を記録します。価格が当日の高値を超えた時点がエントリーシグナルとなります。

-

エントリー・イグジット条件:エントリー後にストップロスとテイクプロフィットの比率を設定し、トレーリングストップを有効にして利益を確定することも可能です。また、特定のEMAに対して条件付きでストップロスをかけることもできます。

-

最適化設定:エントリー前のスプレッド比率を設定し、エントリータイミングを調整することで、偽のブレイクアウトを回避できます。ストップロス、テイクプロフィット、トレーリングストップの動的パラメータを設定できます。

具体的には、本戦略は当日の高値を記録し、エントリータイミングを判断します。価格が当日の高値を超えた時点でロングエントリーします。その後、ストップロスとテイクプロフィットでイグジットし、トレーリングストップも有効にできます。また、価格が特定のEMAを下回った場合にもストップロスをかけることができます。最適化方法としては、エントリー前のスプレッド比率を設定し、ストップロス・テイクプロフィット比率を調整してリスクをコントロールし、トレーリングストップで利益を確定します。

優位性分析

本戦略には以下の利点があります。

- トレンドフォローにより、トレンド相場で利益を獲得できる。

- ブレイクアウト戦略であり、エントリーシグナルが明確。

- 当日の高値を考慮することで、連続エントリーを防止。

- ストップロス・テイクプロフィットの設定によりリスク管理が容易。

- トレーリングストップで利益を確定可能。

- パラメータ最適化により、エントリータイミングを調整しリスクを制御可能。

- シンプルで直感的、理解・実装が容易。

- ロング・ショート両方向で利用可能。

リスク分析

本戦略には以下のリスクも存在します。

- ブレイクアウト戦略は、エントリー後にすぐ価格が反落するなど、嵌め込まれるリスクがある。

- トレンド相場でのみ有効であり、レンジ相場ではパフォーマンスが悪い。

- ストップロスの比率を適切に設定する必要があり、緩すぎると損失が拡大する可能性がある。

- エントリースプレッド比率を適切に設定する必要があり、過度に積極的だと損失が拡大する可能性がある。

- 偽のブレイクアウトにより不必要な損失が発生する可能性があるため、調整・最適化が必要。

- ブレイクアウト時の出来高がその後の値動きを支えられるか注意が必要。

- 異なる時間足のパラメータ設定間の整合性に注意する必要がある。

最適化の方向性

本戦略は以下の点から最適化が可能です。

- 出来高やオシレーター指標など、他のテクニカル指標を追加し、レンジ相場での嵌め込みを回避。

- 曲線適合指標を追加し、トレンドの質を判断し、偽のトレンドフォローを防止。

- エントリースプレッドを動的に最適化し、市場のボラティリティに応じてスプレッド要件を調整。

- ストップロス・テイクプロフィットを動的に最適化し、市場に合わせてパラメータを調整。

- 異なる銘柄・時間足に対して異なるパラメータを設定。

- 機械学習手法を用いて異なるパラメータが戦略に与える影響をテスト。

- オプション機能を追加して設定を最適化。

- レンジ相場での戦略適用方法を研究。

- 複数時間足や銘柄を組み合わせたポートフォリオ戦略に拡張。

まとめ

本戦略は前日高値ブレイクアウトのトレンドフォロー発想に基づき、トレンド相場で良好なパフォーマンスを示します。しかし、嵌め込みリスクやパラメータ最適化の課題も存在します。より多くの判断指標の導入、動的なパラメータ最適化、ポートフォリオ戦略への拡張などにより、さらなる改善が可能です。総じて、本戦略は短期トレンドフォローに適していますが、リスク管理とパラメータ最適化に注意を払う必要があります。

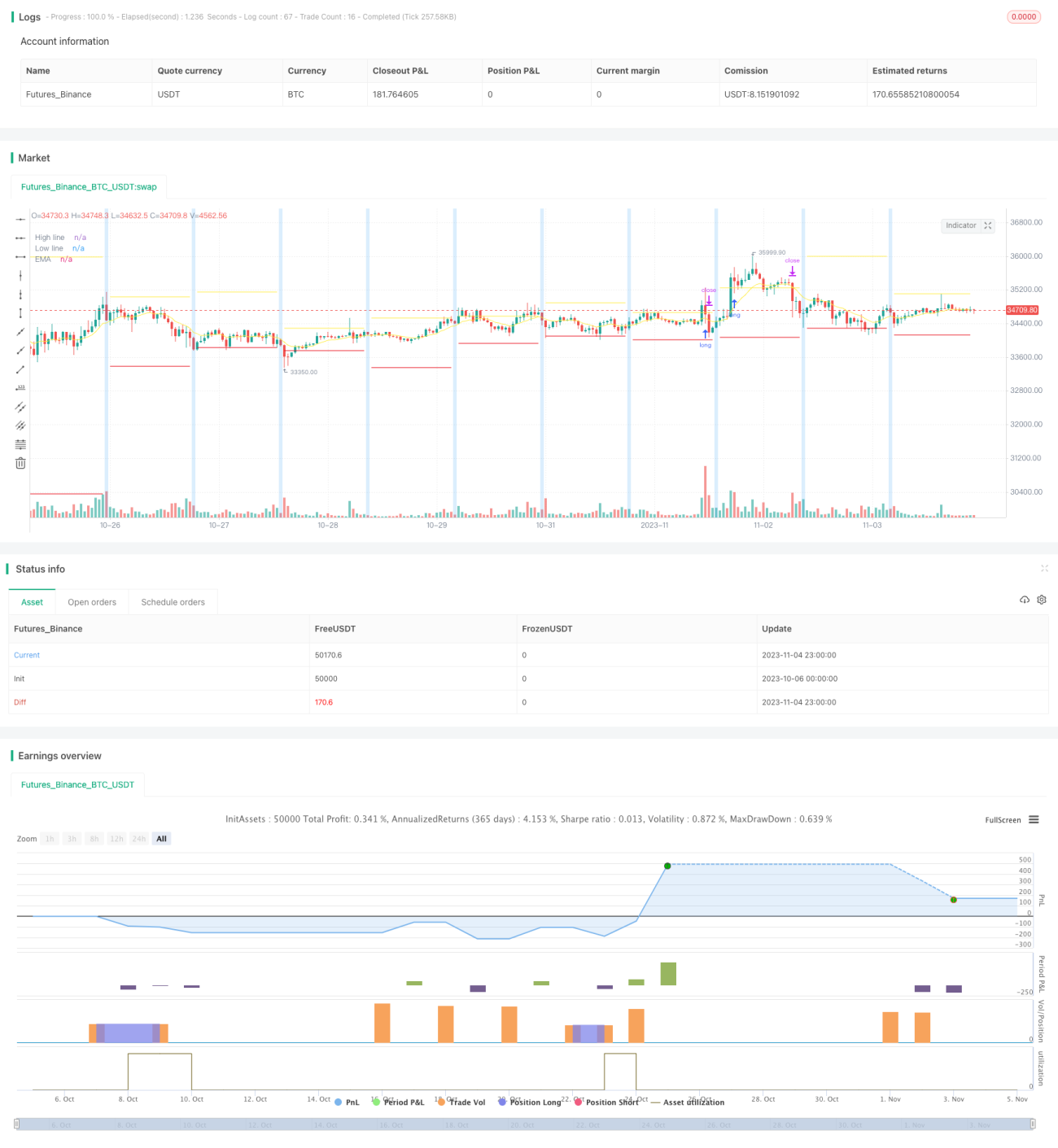

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Author: © tumiza 999

// © TheSocialCryptoClub

- 1