RSI両方向ブレイクアウト戦略

概要

本戦略は相対力指数(RSI)インジケーターに基づいて設計されており、RSIの買われ過ぎ・売られ過ぎの原理を利用して双方向ブレイクアウト取引を行います。RSIが設定した買われ過ぎラインを上抜けたらロング、売られ過ぎラインを下抜けたらショートする、典型的な逆張り戦略です。

戦略の原理

-

ユーザー入力に基づき、RSIインジケーターのパラメータ(RSI期間、買われ過ぎライン閾値、売られ過ぎライン閾値)を設定します。

-

RSI曲線と買われ過ぎライン・売られ過ぎラインとの位置関係から、買われ過ぎゾーンか売られ過ぎゾーンかを判断します。

-

RSIが売られ過ぎゾーンから対応する閾値ラインをブレイクした場合、反対方向にポジションをオープンします。例えば、買われ過ぎゾーンから買われ過ぎラインをブレイクした場合、相場が反転すると判断してロングエントリー。売られ過ぎゾーンから売られ過ぎラインをブレイクした場合、相場が反転すると判断してショートエントリーします。

-

エントリー後、ストップロスとテイクプロフィットラインを設定します。ストップロス・テイクプロフィットの状態を追跡し、条件を満たしたらポジションをクローズします。

-

本戦略はEMAをフィルターとして使用するオプション機能も備えています。RSIのロング・ショートシグナルが出た時点で、価格がEMAをブレイクしている場合のみエントリーします。

-

特定の取引時間帯のみ取引する機能も提供します。ユーザーは特定の時間帯のみ取引し、時間外はポジションをクローズして離脱するよう設定できます。

優位性分析

- RSIの古典的なブレイクアウト原理を利用しており、バックテスト結果が良好。

- 買われ過ぎ・売られ過ぎの閾値を柔軟に設定でき、異なる商品に調整可能。

- EMAフィルターを使用するか選択でき、小幅なレンジ相場での頻繁なエントリー・エグジットを回避。

- ストップロス・テイクプロフィット機能により、戦略の安定性を向上。

- 特定の取引時間帯を設定でき、不適切な時間帯の取引を回避。

- ロング・ショート双方向取引に対応し、相場の双方向の値動きを活用可能。

リスク分析

- RSIはダイバージェンスが発生しやすく、RSIだけで判断すると誤ったシグナルが出る可能性がある。トレンドや移動平均線などと組み合わせて判断する必要がある。

- 買われ過ぎ・売られ過ぎの閾値設定が不適切だと、取引が多すぎたりチャンスを逃したりする可能性。

- ストップロス・テイクプロフィットの設定が不適切だと、戦略がアグレッシブすぎたり保守的すぎたりする。

- EMAフィルターの設定が不適切だと、有効なシグナルを逃したりフィルターしすぎたりする可能性。

リスク対策:

- RSIパラメータを最適化し、異なる商品に適したパラメータに調整。

- トレンド指標などと組み合わせてダイバージェンスを判断し、誤ったシグナルを回避。

- ストップロス・テイクプロフィットパラメータをテスト・最適化し、最適なパラメータを発見。

- EMAパラメータをテスト・最適化し、最適なフィルターレベルを発見。

戦略の最適化方向

本戦略は以下の点から最適化できます:

-

RSIパラメータの最適化:異なる商品に最適なパラメータの組み合わせを探索。バックテストを網羅的に行い、最適な買われ過ぎ・売られ過ぎの閾値を見つける。

-

他のインジケーターをRSIの代わりや組み合わせとして試し、より強い判断シグナルを形成。例えばMACD、KD、ボリンジャーバンドなど。

-

ストップロス・テイクプロフィット戦略の最適化:戦略の安定性を向上。市場のボラティリティに応じたトレーリングストップや、トレーリングストップ機能を備えた戦略を検討。

-

EMAフィルターパラメータの最適化、または他の指標フィルターのテストにより、さらにエントリーの質を向上。

-

トレンド判断モジュールの追加:逆張りでロングすべきでない上昇トレンドや、ショートすべきでない下降トレンドを回避。

-

異なる取引時間帯のパラメータをテストし、本戦略に適した時間帯と避けるべき時間帯を判断。

まとめ

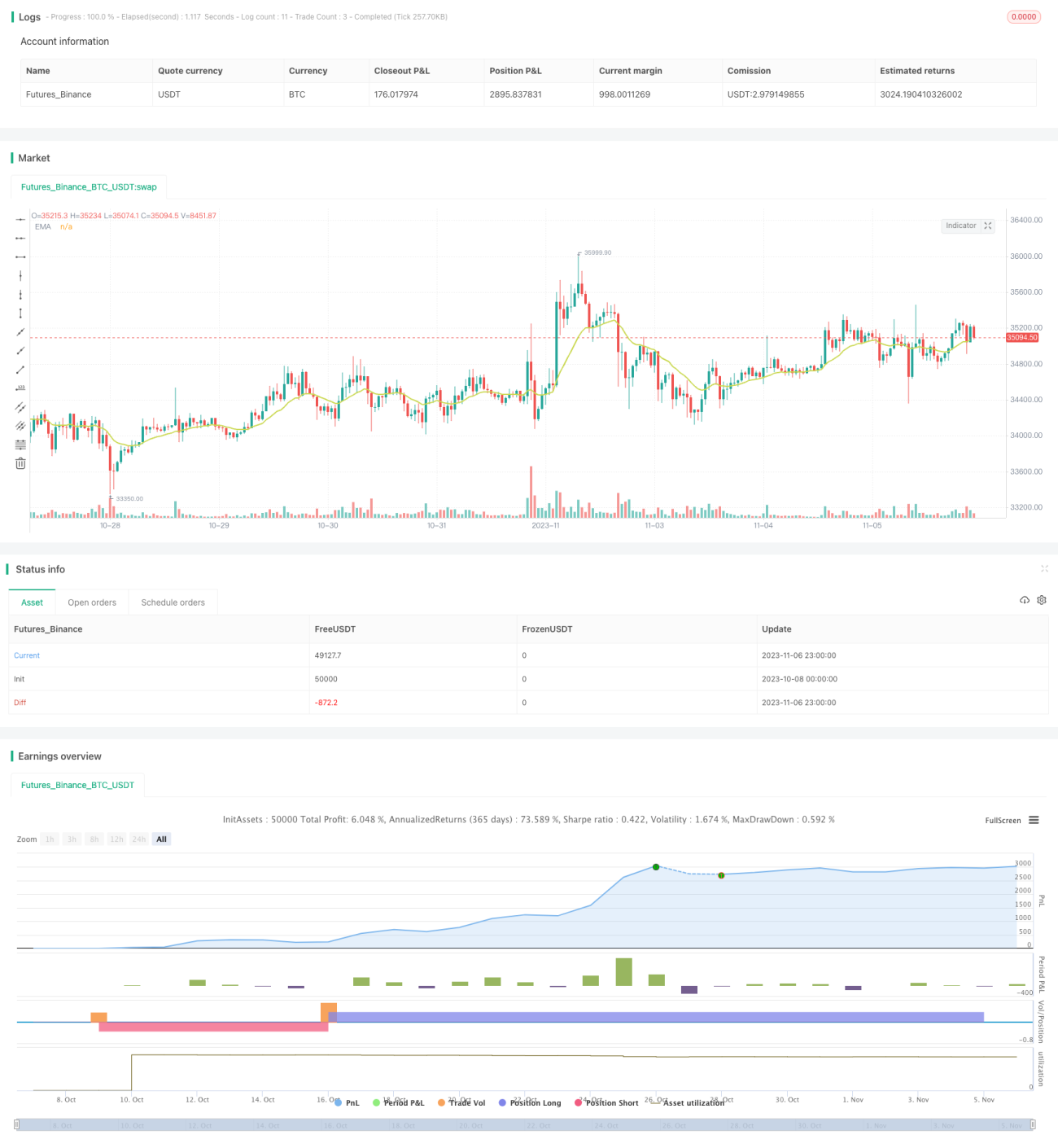

本RSI双方向ブレイクアウト戦略は全体として明確なロジックを持ち、古典的なRSIの買われ過ぎ・売られ過ぎの原理を利用した逆張り取引です。買われ過ぎ・売られ過ぎゾーンでの反転の機会を捉えつつ、EMAフィルターとストップロス・テイクプロフィットでリスクを制御できます。パラメータ最適化やモジュール最適化の余地が大きく、より安定した信頼性の高い逆張り戦略に仕上げることが可能です。さらなるテスト・最適化を経て実運用に値する戦略です。

- 1