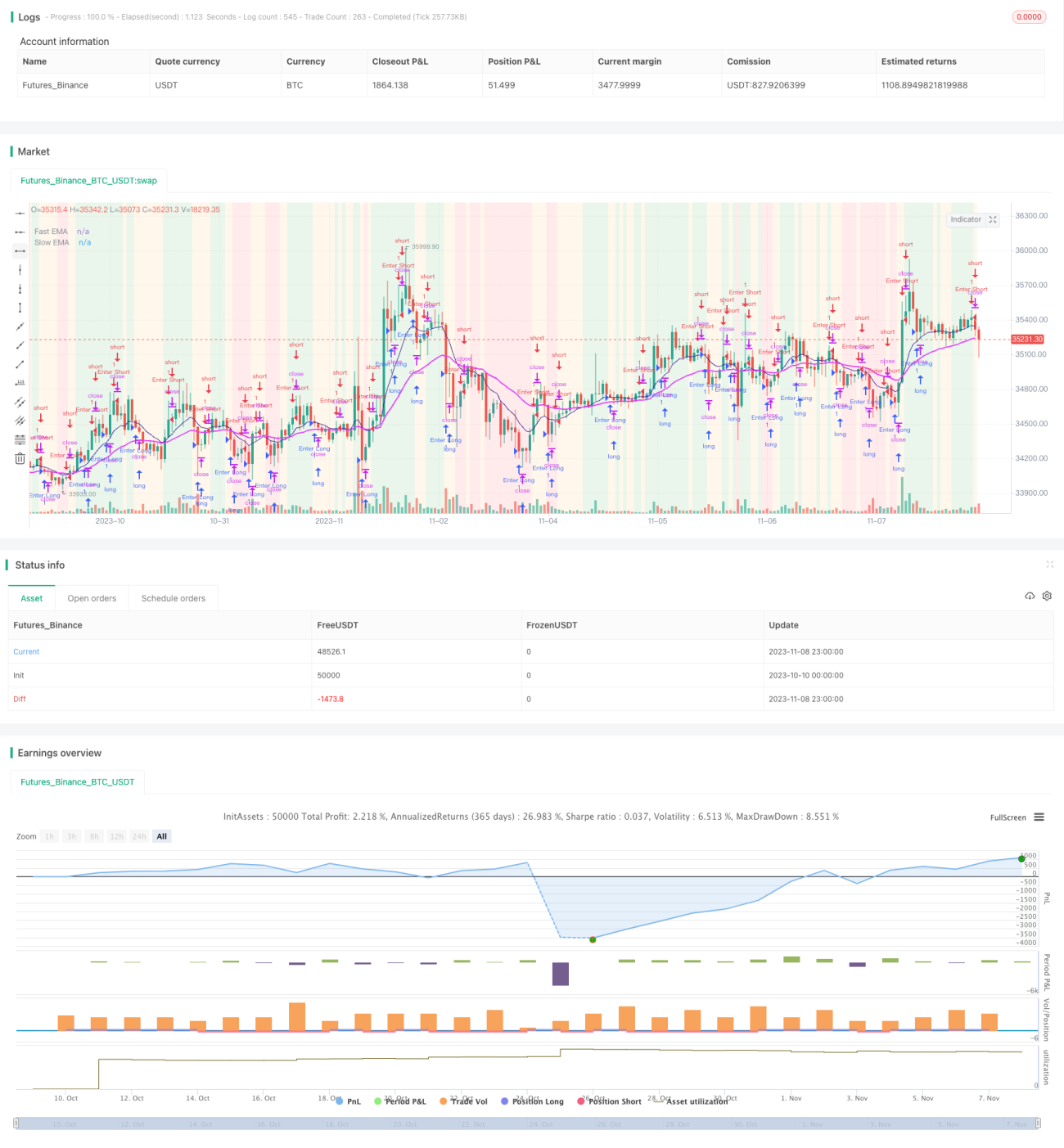

ダブル移動平均線リバーサル取引戦略

概要

本戦略は、短期移動平均線と長期移動平均線のゴールデンクロス・デッドクロスの原理に基づいて設計されています。短期線が下方から長期線を上抜けた時に買い、短期線が上方から長期線を下抜けた時に売りを行います。この戦略は中長期の取引に適しており、市場トレンドの反転を捉えることができます。

戦略の原理

本戦略では指数移動平均(EMA)を使用して短期線と長期線を計算します。短期EMAの期間は10、長期EMAの期間は30です。まず短期EMAと長期EMAを計算し、移動平均線を描画するとともに、トレンド方向を示すために異なる色の背景を表示します。

本日の終値が短期線より高く、かつ短期線が長期線より高い場合、上昇トレンドを示す緑色の背景を表示します。本日の終値が短期線より低く、かつ短期線が長期線より低い場合、下降トレンドを示す赤色の背景を表示します。

上昇トレンドにおいて、赤色のローソク足(終値が始値より低い)が出現し、前日も赤色のローソク足であった場合、買いエントリーを行います。ストップロスは300ポイント、利確は売り手仕舞いとします。

下降トレンドにおいて、緑色のローソク足(終値が始値より高い)が出現し、前日も緑色のローソク足であった場合、売りエントリーを行います。ストップロスは300ポイント、利確は買い手仕舞いとします。

各取引方向でポジションを保有した後、保有期間が1008000000ミリ秒(約2週間)を超えた場合、強制的にポジションをクローズし、保有の膠着を防止します。

優位性の分析

- ダブルEMAシステムを使用することで、市場のノイズを効果的に除去し、トレンドの反転点を特定できます。

- 短期線と長期線に加えてローソク足の実体の色を判断材料とすることで、エントリーシグナルが比較的信頼性の高いものになります。

- ストップロスと利確の戦略を設定することで、個別取引の損失を軽減します。

- 強制手仕舞いの仕組みにより、保有の膠着による巨額の損失を回避します。

リスク分析

- EMAシステムは急激な相場変動に鈍感なため、一部の取引機会を逃す可能性があります。

- 短期線と長期線のパラメータ設定が適切でない場合、偽のシグナルが発生する可能性があります。

- ストップロス幅が浅すぎるとロスカットリスクが高まり、深すぎると不必要な損失が発生する可能性があります。

- 強制手仕舞いの時間設定が適切でない場合、早期手仕舞いやポジション保有期間の長期化を招く可能性があります。

最適化の方向性

- 異なるパラメータでEMAシステムの収益率をテストし、短期線と長期線の期間を最適化できます。

- MACDなどの他の指標を追加して確認を行い、シグナルの正確性を高めることが考えられます。

- 当日の取引量の変化を考慮してストップロス水準を決定することも可能です。

- 市場のボラティリティ範囲に応じて、強制手仕舞いの時間を動的に調整できます。

まとめ

本戦略は全体的にバランスが取れており、ダブルEMAでトレンドを識別し、ローソク足の実体に付加的なルールを組み合わせて取引を行うことで、偽のシグナルを効果的に除去できます。ただし、EMAシステムとパラメータ設定はさらなる最適化が必要であり、ストップロスや利確の仕組みも市場に合わせて調整する必要があります。全体的には信頼性の高いトレンドフォロー戦略です。

- 1