マルチインジケーター・ボラティリティバンド取引戦略

概要

本戦略は、ボリンジャーバンド、RSI、MACDなどの複数のテクニカル指標を組み合わせて売買判断を行います。まずチャート上に通常のボリンジャーバンドを描画しますが、2つの異なる標準偏差レベルを2色のバンド領域で表示する点が特徴です。その後、バンドが突破されたかどうかに基づいてポジションを建てます。さらに、RSIとMACDをエントリーシグナルの追加確認として利用します。全体として、複数のテクニカル指標を用いて売買判断とポジション管理を行う総合的なトレーディング戦略です。

戦略の原理

-

まず、期間34のボリンジャーバンドをチャートに描画します。中央線、1標準偏差、2標準偏差の上限・下限バンドを含みます。

-

終値が上限バンドを上抜けた場合にロングエントリー、終値が下限バンドを下抜けた場合にショートエントリーを行います。

-

ロングポジション保有中に終値が中央線を下抜けた場合、ロングポジションを決済します。ショートポジション保有中に終値が中央線を上抜けた場合、ショートポジションを決済します。

-

さらにRSIを導入し、RSIが70超えをロングエントリーの追加確認、RSIが30未満をショートエントリーの追加確認とします。

-

RSIが50を上抜けた場合にショートポジションを決済、RSIが50を下抜けた場合にロングポジションを決済します。

-

またMACDを導入し、MACDのゴールデンクロスをロングエントリーの追加確認、デッドクロスをショートエントリーの追加確認とします。

-

MACDがデッドクロスした場合にロングポジションを決済、ゴールデンクロスした場合にショートポジションを決済します。

-

以上を統合し、本戦略ではボリンジャーバンド、RSI、MACDの3つの指標がすべて条件を満たした場合にのみエントリーします。決済条件も3つの指標を考慮することで、誤シグナルの確率を低減します。

優位性分析

複数の指標を組み合わせてシグナルをフィルタリングすることで、誤ったトレードを効果的に回避できます。ボリンジャーバンドは価格の突破シグナルを提供し、RSIは買われすぎ・売られすぎをフィルタリングし、MACDはトレンドの変化をフィルタリングします。これら3つが同時にシグナルを確定することで、収益確率を大幅に向上させることができます。

また、本戦略はエントリーと決済のロジックを異なるものに設定し、ポジションリスクを厳格に管理しています。中央線、RSIの中立線50、MACDのゴールデンクロス・デッドクロスを決済条件として導入することで、迅速に損切りでき、1回の損失を抑えることができます。

単一指標戦略と比較して、本戦略は複数の指標の利点を統合しているため、収益率と勝率を大幅に向上させ、最大ドローダウンを低減できます。複数指標の組み合わせフィルターにより誤トレードの確率が減り、厳格な損切りメカニズムにより各損失トレードの影響をコントロールできます。

総じて、本戦略は中長期のトレンドトレードに非常に適しており、市場の主要トレンドを捉えると同時に、指標の詳細を利用してポジションが逆方向に動くのを防ぐことができます。複数指標によるリスク管理メカニズムにより、高いレバレッジを安全に使用することも可能です。

リスク分析

本戦略には主に以下のリスクがあります:

-

指標による誤シグナルの発生確率。複数の指標を組み合わせることで誤シグナルを減らせますが、完全に排除することは不可能です。指標パラメータを最適化し、誤シグナル率をさらに低減する必要があります。

-

一方向の相場で利益を得られない可能性がある。トレンドがもみ合う場合、損切りが発生し、継続的に利益を上げることが難しい場合があります。損切り基準を緩和し、保有期間を延長することで対応できます。

-

一部の指標に遅延が生じ、最適なエントリータイミングを逃す可能性がある。より先進的な指標をテストし、転換点を早期に捉えることができます。

-

大幅なギャップオープンにより損切りが機能しない可能性がある。チャネル損切りや段階的なポジション追加により損失をコントロールできます。

-

パラメータが固定されすぎているため、異なる市場で調整が必要。機械学習を導入し、自動でパラメータを最適化できます。

-

テストデータが不足し、過学習の可能性がある。より長期間かつ多様な市場で戦略のロバスト性をテストする必要があります。

最適化の方向性

本戦略は以下の点からさらに最適化できます:

-

指標パラメータの最適化:ボリンジャーバンドの期間、RSIの期間、MACDのパラメータのより適切な組み合わせを見つけ、誤シグナルを低減します。ステップ法や総当たり法などで最適パラメータを探索できます。

-

適応型損切りの導入:固定の中央線損切りではなく、ATRやトレンドなどの要素を組み合わせて損切り位置を動的に調整します。

-

機械学習技術の導入:パラメータの適応的最適化を実現。強化学習を用いて異なる市場環境でパラメータを最適化できます。

-

トレンド判定ルールの追加:相場の段階に応じて異なる戦略を採用し、戦略の適応力を高めます。

-

テキスト分析やソーシャルデータなどの多要素予測を強化し、より先進的な指標で転換点を早期に判断します。

-

複利最適化:資金量に応じてポジションサイズを調整し、収益が指数関数的に成長するようにします。

-

ポートフォリオ最適化:補完的な戦略を探索し、無相関性を利用してポートフォリオの収益変動を低減します。

まとめ

本戦略は複数のテクニカル指標を組み合わせてエントリーとエグジットを判断し、厳格な損切りルールを設定しています。単一指標と比較して、複数指標の組み合わせは誤シグナルを大幅に削減し、収益確率を高めることができます。損切りルールは各損失の影響をコントロールします。この戦略はトレンド相場に適しており、比較的安定した収益を得ることができます。今後の課題は指標パラメータの最適化と戦略の適応力強化です。全体として、本戦略は信頼性が高く、安定した効率的な定量取引ソリューションです。

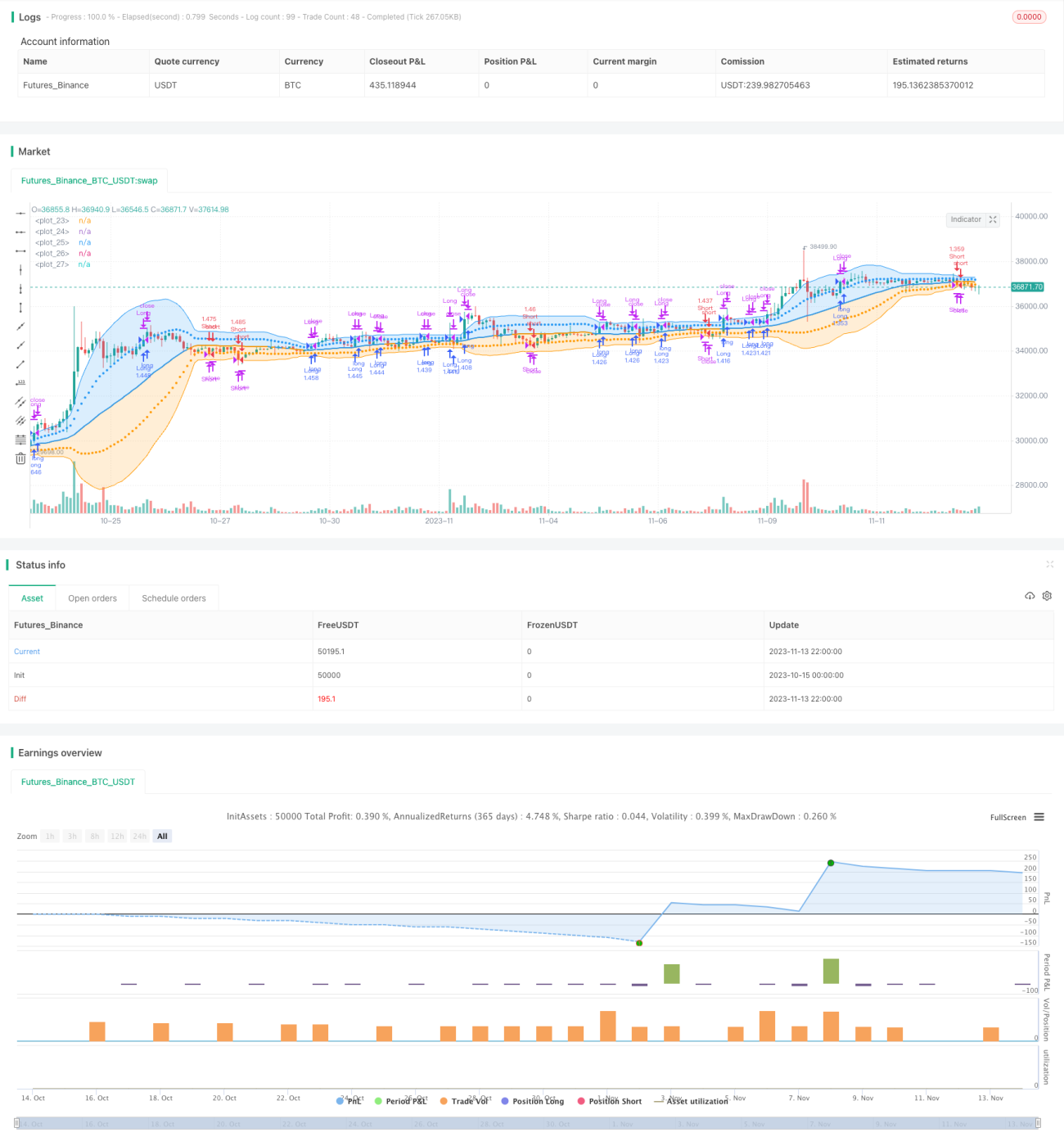

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// Bollinger Bands: Madrid : 14/SEP/2014 11:07 : 2.0

// This displays the traditional Bollinger Bands, the difference is

// that the 1st and 2nd StdDev are outlined with two colors and two- 1