ダブルタートルブレイクアウト戦略

1

Follow

1802

Followers

概要

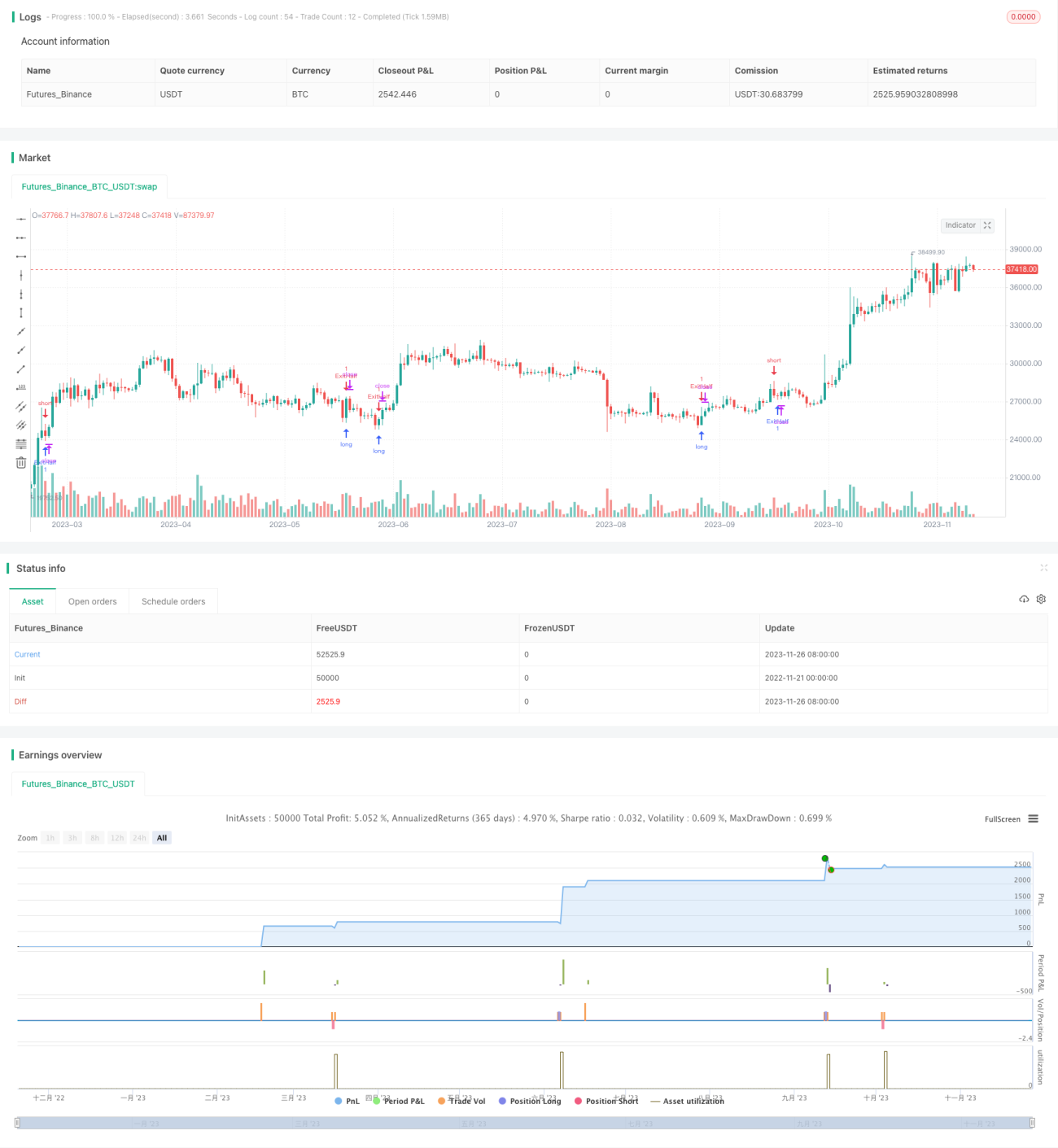

ダブルタートルブレイクアウト戦略は、タートルトレーディング法のブレイクアウト戦略とリンダ・ラシュクのトレーリングストップ原理を融合し、優れたブレイクアウト性能と厳格なリスク管理を実現しています。本戦略は同時に価格の上方・下方ブレイクアウトを監視し、ブレイクアウト発生時にロングまたはショートポジションを構築し、トレーリングストップとトレーリングプロフィットを利用してポジションを管理します。

戦略の原理

中核ロジックは、大周期の高値が小周期の高値を突破した際にショートし、大周期の安値が小周期の安値を下抜けた際にロングすることです。ポジション構築後、トレーリングストップとトレーリングプロフィットを設定し、まずストップロスでリスクを確定します。ポジション保有数が設定された利確数量に達した場合、次の周期でストップロス注文をキャンセルし、半分明けしてトレーリングストップとトレーリングプロフィットを設定し、利益を確定して価格差を追跡します。

具体的な操作手順は次のとおりです。

- 大周期(20期間)の高値prevHighと小周期(4期間)の高値smallPeriodHighを計算します。

- 最新のローソク足の高値がprevHighより大きく、かつprevHighがsmallPeriodHighより大きい場合、大周期の高値が小周期の高値を突破したことを示し、この時ポジションがなければショートします。

- ポジション構築後、トレーリングストップを設定し、ポジションが反転したらストップロス注文をキャンセルし、ストップロスにかからないようにします。

- 保有数量が設定されたトレーリングプロフィット期間数(現在は0期間)に達した場合、次の周期で半分のポジションを決済し、トレーリングストップとトレーリングプロフィットを設定し、価格差を追跡して利益を確定します。

- 安値のブレイクアウトも同様に、大周期の安値と小周期の安値のブレイクアウト関係に基づいてロングポジションを構築します。

優位性の分析

本戦略は総合性の高いブレイクアウト戦略であり、以下の優位性があります。

- 二重周期のタートルトレーディング法を組み合わせ、ブレイクアウトシグナルを効果的に識別できます。

- トレーリングストップとトレーリングプロフィット技術を採用し、リスクを厳格に管理し、大きな損失を回避します。

- 2回に分けてエグジットし、1回目の利確で半分を決済、その後トレーリングプロフィットで全量を決済し、利益を確定します。

- ロングとショートの双方向取引に対応し、多空が入れ替わる市場特性に適合します。

- バックテストの結果が優れており、実戦でのパフォーマンスが高いです。

リスク分析

主なリスクと対策は以下のとおりです。

- 偽ブレイクアウトのリスク。周期パラメータを適切に調整し、ブレイクアウトの有効性を確保する必要があります。

- 高値追い・安値売りのリスク。トレンドや形状によるフィルタリングを組み合わせ、トレンド末期でのポジション構築を避ける必要があります。

- ストップロスが突破されるリスク。ストップロスの幅を適度に広げ、十分な余裕を確保することができます。

- トレーリングストップが過敏になるリスク。ストップロス後のスリッページ設定を調整し、無駄なストップロスを避ける必要があります。

最適化の方向性

本戦略は以下の点からさらに最適化できます。

- 出来高によるブレイクアウトのフィルタリングを追加し、ブレイクアウトの真実性を確保します。

- トレンド判断指標を追加し、トレンド末期でのポジション構築を回避します。

- より多くの時間周期を組み合わせてブレイクアウトのタイミングを判断します。

- 機械学習アルゴリズムを追加し、パラメータを動的に最適化します。

- 他の戦略と組み合わせ、統計的裁定を実施します。

まとめ

ダブルタートルブレイクアウト戦略は、二重周期のテクニカル分析、ブレイクアウト理論、厳格なリスク管理手段を総合的に活用し、高い勝率を維持しつつ、収益の安定性も確保しています。本戦略のモデルはシンプルで明確であり、理解と適用が容易な、非常に優れた定量戦略です。また、本戦略には大きな最適化の余地があり、投資家はこれを基に革新を加え、より優れた取引システムを構築することができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1