二重移動平均線のゴールデンクロス・デッドクロス定量戦略

概要

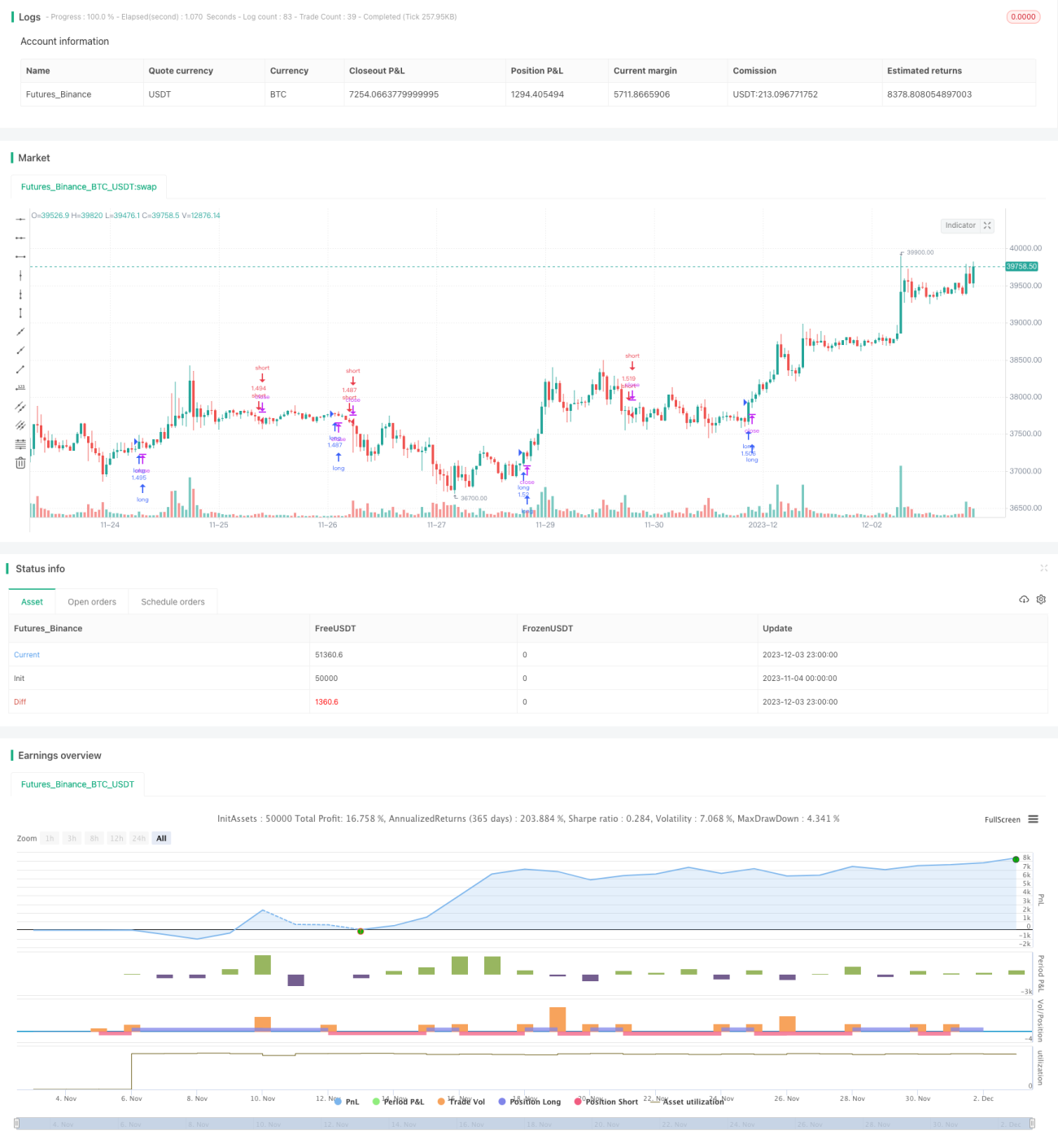

本戦略は、二重ALMA移動平均線のゴールデンクロス・デッドクロスシグナルと、MACDインジケーターの強弱シグナルを組み合わせ、自動でロング・ショートを行うものです。戦略は4時間足以上の時間軸に適しており、テストデータはBNB/USDT、期間は2017年から現在まで、手数料は0.03%に設定しています。

戦略の原理

戦略では、ALMAの短期線と長期線で二重移動平均線を構築します。短期線の長さは20、長期線は40で、いずれもオフセット0.9、標準偏差5を使用します。短期線が長期線を上抜けた場合にロングシグナル、下抜けた場合にショートシグナルを生成します。

同時に、MACDインジケーターのヒストグラムシグナルも組み合わせます。MACDヒストグラムが正(上昇)の場合のみロングシグナルが有効となり、負(下降)の場合のみショートシグナルが有効となります。

また、本戦略は利確・損切条件も設定しています。ロングの利確は2倍、損切は0.2倍、ショートの利確は0.05倍、損切は1倍です。

優位性分析

本戦略は、二重移動平均線によるトレンド判断とMACDによるエネルギー判断を組み合わせることで、偽シグナルを効果的にフィルタリングし、エントリー精度を高めています。利確・損切の設定も合理的で、利益を最大限確保し、大きな損失を回避できます。

バックテストデータは2017年以降、複数回の強気相場と弱気相場の転換を含んでおり、戦略は異なるサイクル条件下でも良好なパフォーマンスを示しています。これは市場の線形・非線形特性に適応していることを証明しています。

リスク分析

本戦略には以下のリスクがあります:

- 二重移動平均線自体にラグが存在するため、短期的なチャンスを逃す可能性がある

- MACDヒストグラムがゼロの場合、シグナルが発生しない

- 利確・損切比率は事前設定であり、実際の相場と乖離する可能性がある

解決方法:

- 移動平均線の期間を適切に短縮し、短期感度を高める

- MACDパラメータを最適化し、ヒストグラムの変動をより頻繁にする

- 利確・損切設定を動的に調整する

最適化の方向性

本戦略は以下の点からさらに最適化が可能です:

- 異なるタイプの移動平均線を試し、より優れた平滑化効果を探す

- 移動平均線とMACDのパラメータを最適化し、異なる銘柄や時間軸に適合させる

- 出来高の変化などの追加条件を組み込み、シグナルをフィルタリングする

- 利確・損切の比率をリアルタイムで調整し、戦略の適応性を高める

まとめ

本戦略は、移動平均線によるトレンド判断とMACDによる補助判断を成功裏に組み合わせ、合理的な利確・損切を設定することで、様々な相場状況において安定した収益を得ることができます。パラメータ設定の継続的な最適化や追加フィルタ条件の導入により、戦略の安定性と収益性はさらに向上する可能性があります。

- 1