StochRSIに基づくクオンツ取引戦略

概要

本戦略はStochRSI指標に基づいて開発されています。この戦略は主にStochRSI指標を使用して買われすぎ・売られすぎの状況を判断し、RSI指標と組み合わせて誤ったシグナルを除去します。StochRSI指標が売られすぎ領域を示したときに売り、買われすぎ領域を示したときに買いを行い、利益を得ることを目的としています。

戦略の原理

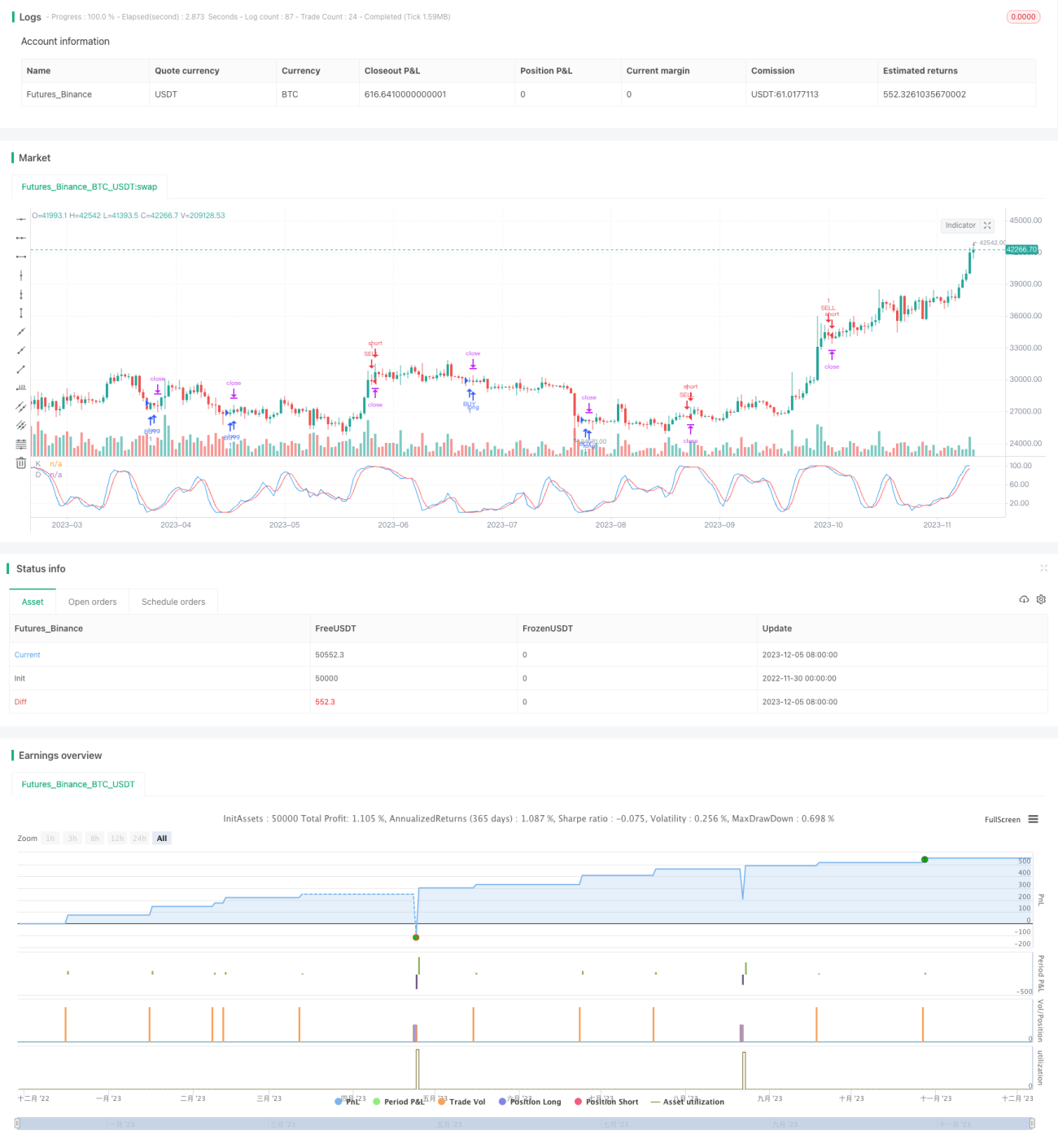

本戦略は主にStochRSI指標を適用して市場の買われすぎ・売られすぎ領域を判断します。StochRSI指標はK線とD線で構成され、K線は現在のRSIの値が直近期間のRSI価格範囲内でどの位置にあるかを反映し、D線はK線の移動平均線です。K線がD線を上抜けた場合が売られすぎ領域であり、このとき買いを行うことができます。K線がD線を下抜けた場合が買われすぎ領域であり、このとき売りを行うことができます。

具体的には、戦略はまず期間14のRSI指標の値を計算し、次にそのRSI指標にStochRSI指標を適用します。StochRSI指標のパラメータは期間14、平滑化周期K線3、D線3に設定されています。K線がユーザー設定の売られすぎ領域(デフォルト1)を上抜けたときに買い、K線がユーザー設定の買われすぎ領域(デフォルト99)を下抜けたときに売りを行います。

さらに、戦略には損切りと利確のパラメータも設定されています。損切りパラメータのデフォルトは10000です。利確はパラメータとして設定されたトレーリングストップ方式で、デフォルトのトレーリングポイント数は300、オフセットは0です。

優位性分析

- StochRSI指標を使用して買われすぎ・売られすぎ領域を判断することで、単一のRSI指標よりも信頼性が高い

- RSIと組み合わせてシグナルをフィルタリングし、誤ったブレイクアウトを回避

- 損切り・利確メカニズムを設定してリスクを管理

リスク分析

- StochRSI指標には誤ったシグナルが発生する可能性がある

- 買われすぎ・売られすぎのパラメータを適切に設定しないと誤操作につながる

- 損切りの値幅が小さすぎるとポジションが拘束されやすく、利確の値幅が大きすぎると得られる利益が限定的になる可能性がある

これらのリスクに対しては、より長いパラメータ周期を設定したり、他のインジケーターとの組み合わせを検討してシグナルをフィルタリングすること、買われすぎ・売られすぎのパラメータを市場に合わせて調整すること、そして異なる損切り・利確パラメータをテストすることなどが考えられます。

最適化の方向性

- MACDやボリンジャーバンドなど他のインジケーターとの組み合わせを検討し、誤ったシグナルをフィルタリングする

- さまざまな市場状況に対応できるよう、異なるパラメータ周期の設定をテストする

- バックテストで損切り・利確ポイントを複数回テストし、最適なパラメータを見つける

まとめ

本戦略はStochRSI指標に基づいて買われすぎ・売られすぎ領域を判断し、取引を行います。単一のRSI指標と比較して、StochRSIはKDJの考え方を取り入れており、転換点をより正確に判断できます。同時にRSIと組み合わせて誤ったシグナルをフィルタリングし、損切り・利確を設定してリスクを管理します。最適化の余地は大きく、他のインジケーターとの組み合わせやパラメータ設定の最適化が可能です。

- 1