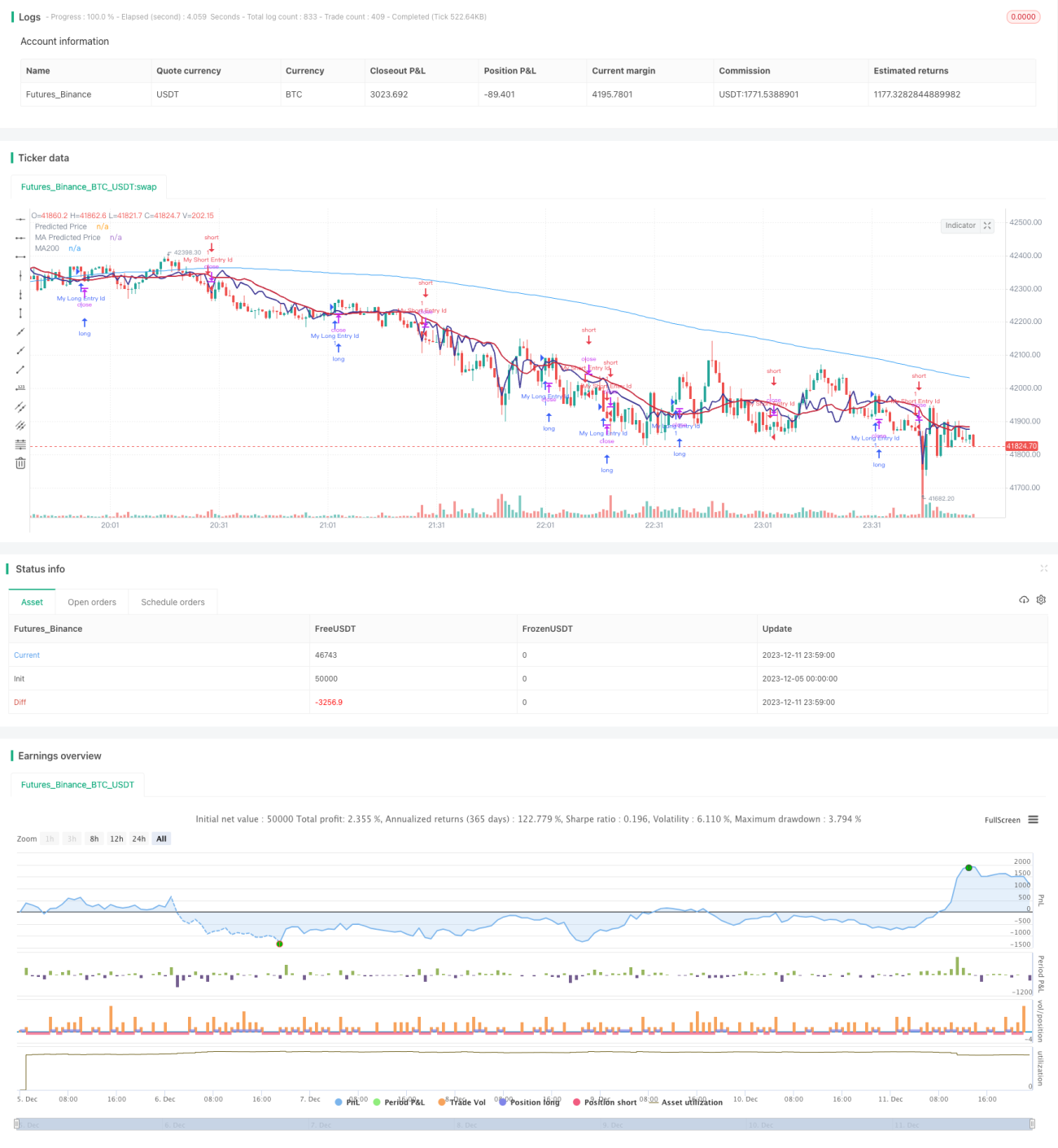

ダイナミック・イデオロギー・トレンド・リバーサル戦略

1

Follow

1802

Followers

概要

動的イデオロギー的トレンド反転戦略は、線形回帰を用いて価格を予測し、移動平均線が形成するイデオロギーを組み合わせて取引シグナルを生成します。予測価格が下から上へ移動平均線をクロスしたときに買いシグナル、上から下へクロスしたときに売りシグナルを発生させ、トレンド反転を捉えます。

戦略の原理

- 出来高に基づいて株価の線形回帰を計算し、価格の予測値を得る

- 異なる条件の移動平均線を計算する

- 予測価格が下から上へ移動平均線をクロスしたとき、買いシグナルを発生

- 予測価格が上から下へ移動平均線をクロスしたとき、売りシグナルを発生

- MACD指標と組み合わせてトレンド反転のタイミングを判断する

上記のシグナルは複数の確認要素を組み合わせることで、偽のブレイクアウトを回避し、シグナルの精度を高めます。

優位性分析

- 線形回帰を用いて価格トレンドを予測し、シグナル精度を向上

- 移動平均線が形成するイデオロギーと組み合わせ、トレンド反転を捉える

- 出来高に基づいて線形回帰を計算するため、経済的意義が高い

- MACDなどの指標で多重確認を行い、偽シグナルを低減

リスク分析

- 線形回帰のパラメータ設定が結果に大きな影響を与える

- 移動平均線の設定もシグナルの品質に影響する

- 確認メカニズムがあるものの、偽シグナルのリスクは依然存在する

- コードをさらに最適化し、取引回数を減らして収益率を高める余地がある

最適化の方向性

- 線形回帰と移動平均線のパラメータを最適化

- 確認条件を追加し、偽シグナル率を低下させる

- より多くの因子を組み合わせてトレンド反転の品質を判断

- ストップロス戦略を最適化し、1回の取引リスクを低減

まとめ

動的イデオロギー的トレンド反転戦略は、線形回帰予測と移動平均線が形成するイデオロギーを統合し、トレンド反転のタイミングを捉えます。単一の指標と比較して、より高い信頼性を持ちます。また、パラメータ調整や確認条件の最適化により、シグナル品質と収益性をさらに向上させることが可能です。

Source

Pine

/*backtest

start: 2023-12-05 00:00:00

end: 2023-12-12 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © stocktechbot

//@version=5

strategy("Linear Cross", overlay=true, margin_long=100, margin_short=0)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1